Share this link via:

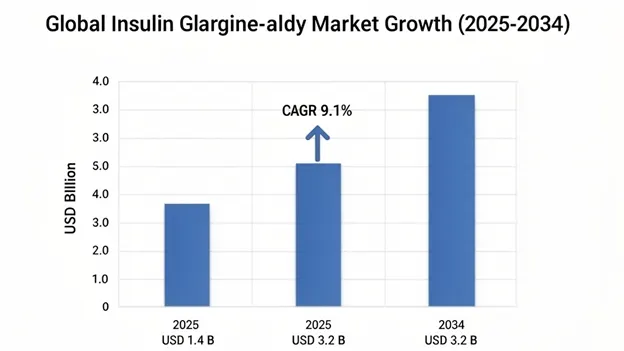

Insulin glargine-aldy injection market size was valued at USD 1.4 billion in 2025 and is projected to reach USD 1.6 billion in 2026, expanding to USD 3.2 billion by 2034, growing at a CAGR of 9.1% during the forecast period (2026-2034).

Insulin glargine-aldy represents a transformative advancement in diabetes therapeutics, because it’s an FDA-approved interchangeable biosimilar to the reference insulin glargine (Lantus). It uses sophisticated recombinant DNA technology, and is designed to provide consistent, peakless basal insulin coverage for roughly 24 hours, following subcutaneous administration. The molecular structure incorporates two key modifications compared with human insulin, including the substitution of asparagine with glycine at position A21 of the A-chain, and the addition of two arginine residues at the C-terminus of the B-chain, and together these changes shift the isoelectric point toward physiological pH. This helps form stable micro precipitates at injection sites, thereby supporting sustained drug release and a more predictable insulin flow.

Clinically, insulin glargine-aldy offers value beyond pharmacological equivalence. It’s also tied to improving healthcare access, while also supporting the economic sustainability of diabetes management systems globally. Because it’s an interchangeable biosimilar, pharmacists can substitute it at the point of dispensing, without prescriber intervention, in places that recognize the interchangeability designation. That reduces adoption barriers, while keeping therapeutic equivalence, which is shown across analytical, preclinical, and clinical comparability work. In a regulatory sense, this designation also directly addresses the global insulin affordability crisis that affects millions. Biosimilar pricing is often 30–70% lower than originator products, while still delivering outcomes.

The global diabetes epidemic keeps expanding, and at unprecedented rates. The International Diabetes Federation reports that 537 million adults living with diabetes in 2021, and they project it to grow to 783 million by 2045. Within that group, about 30-40% of Type 2 diabetes patients eventually require insulin therapy as pancreatic beta-cell function keeps declining. And virtually all Type 1 diabetes patients, from diagnosis onward, rely on lifelong exogenous insulin, continuously growing addressable demand for cost-effective basal insulin solutions, and insulin glargine-aldy is increasingly being adopted as a preferred formulary option. Healthcare systems, insurance providers, and government procurement agencies are evaluating its potential to optimize therapeutic value while also keeping pharmaceutical spending under control.

On the commercial side, the insulin glargine-aldy ecosystem is more than just the molecule. It includes delivery device platforms, patient education programs, and digital health integration, which makes the product feel less like a bare commodity and more aligned with an integrated diabetes management platform. Modern prefilled pen systems improve dosing accuracy, day-to-day convenience, and patient satisfaction versus the traditional vial-and-syringe administration methods, especially for elderly patients or people with limited dexterity or visual acuity. There are also advanced formulations being developed, including higher-concentration U-300 variants that aim for improved pharmacokinetic consistency, less injection volume, and potentially reduced hypoglycemia rates.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 1.4 Billion |

| Forecast Value | USD 3.2 Billion |

| CAGR | 9.1% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Indication, Concentration, Distribution Channel, End-User, Patient Demographics |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Eli Lilly and Company, Viatris Inc., Biocon Biologics, Samsung Bioepis, Sandoz Group AG, Gan & Lee Pharmaceuticals, Sanofi S.A. |

Get more details on this report - Request Free Sample

The growth of the insulin glargine-aldy market is primarily driven by the rising global prevalence of diabetes, like the ongoing worldwide jump in diabetes cases, especially Type 2 diabetes, which makes up 90-95% of all diabetes, and its incidence rates keep climbing across basically every age bracket driven by increasing obesity rates, sedentary lifestyles, and diet patterns get more westernized. Since Type 2 diabetes tends to worsen over time, a lot of people who start off on oral antidiabetic agents will eventually need insulin, as pancreatic beta-cell function slowly declines. This continuously expands the basal insulin patient population. Type 1 diabetes is smaller in raw numbers, roughly 8-9 million globally but it is an insulin-dependent population from diagnosis onward, meaning they need lifelong basal-bolus insulin setups.

Demographic aging also contributes significantly across developed and emerging markets, which adds fuel to the rise of diabetes. As people get older, insulin resistance and beta-cell problems become more pronounced, so Type 2 diabetes incidence climbs sharply after age 65. On top of that, gestational diabetes mellitus, which affects around 14% of pregnancies globally, is another growing use case for insulin therapy, especially when diet and lifestyle changes are insufficient to achieve glycemic targets. Many clinical guidelines now more often recommend long-acting insulin analogs for basal coverage during pregnancy, usually under specialist supervision.

Key performance metrics further illustrate the scale of market expansion. In 2021, global diabetes prevalence hit 537 million adults, and forecasts suggest it could reach 783 million by 2045, representing 46% growth during the forecast period. About 30-40% of Type 2 patients will need insulin intensification within 10 years after diagnosis since oral therapy becomes inadequate. Type 1 diabetes incidence is also moving upward around 3-4% each year globally, with more visible increases in pediatric groups. By 2025, insulin treated diabetes patients passed 100 million globally, and basal insulin formulations are still the category most frequently prescribed.

The commercial trajectory of insulin glargine-aldy is primarily driven by the accelerating adoption of biosimilar insulin products to speed up biosimilar insulin uptake across the big healthcare markets. That’s being driven by payer led formulary control, through structured formulary management strategies, plus government buying habits that lean toward cost effectiveness. At the same time there’s this increasing prescriber and patient trust in biosimilar therapeutic equivalence, which is backed by broad real-world evidence. Health technology assessment groups tend to land on the same message, namely approved biosimilar insulins deliver equivalent clinical value versus reference products. So, in practice this often supports formulary exclusivity deals where payers label biosimilars as preferred, then they add step therapy rules. Those rules basically require a biosimilar trial before they let the originator insulin be covered.

Regulatory progress around interchangeability designation. This represents a significant regulatory advancement, because it allows pharmacist level substitution of the interchangeable biosimilar for the reference product, without requiring prescriber authorization. As a result, administrative friction drops a lot and volume conversion speeds up in retail pharmacy settings. Instead of relying on traditional prescriber adoption, the payer preference gets baked right into the dispensing workflow. That creates structural market share benefits for interchangeable biosimilars. And importantly it can be less tied to individual physician prescribing patterns.

Pharmacy benefit managers and commercial health plans are using even more forceful formulary management approaches. This includes prior authorization for originator insulins, higher patient cost sharing levels on the reference products compared to biosimilars, and sometimes total exclusion of originator products from the covered formulary, replaced by biosimilar alternatives. As a result, payer-driven incentives become increasingly influential. Prescribers may want to avoid extra paperwork, and patients generally seek to minimize out-of-pocket healthcare expenses.

The performance indicators are pointing to fast adoption. Biosimilar insulin penetration in the United States reached about 28% of all insulin glargine prescriptions in 2025, up from under 5% in 2021. Medicare Part D formulary coverage for biosimilars climbed to 87% of plans by 2025, and most of those plans placed biosimilars on preferred tiers. On top of that, average wholesale price discounts for biosimilar insulin glargine versus originator Lantus hit roughly 65-78% in 2025.

The economic burden of diabetes management is one of the biggest fiscal challenges facing healthcare systems worldwide, with total direct medical costs going over USD 760 billion each year globally, and insulin plus other diabetes medicines accounting for a disproportionate share of healthcare expenditure. Lately the historically elevated pricing of the originator insulin line has attracted significant public and regulatory attention, and that has led to various legislative steps, so insulin affordability emerged as a major healthcare accessibility challenge. In response regulators have rolled out measures like price transparency rules, out-of-pocket cost ceilings, and biosimilar promotion directives.

Insulin glargine-aldy and other biosimilar insulin products provide healthcare systems with a workable route to meaningfully lower drug spending on basal insulin therapy, while keeping equivalent clinical results. That creates persuasive economic value claims for national health services, pharmacy benefit managers, hospital formulary committees, and individual patients, especially in places where insurance coverage is thin and people are paying more directly. If biosimilar insulin is adopted widely, the system-level savings could be huge, with economic analyses estimating annual savings of approximately USD 3–4 billion in annual healthcare savings in the United States by itself.

In developing markets, where diabetes prevalence is climbing the fastest, but healthcare budgets are still constrained, the lower purchase price of biosimilar insulin is a direct deciding factor for whether insulin-dependent patients get adequate therapy. So biosimilar availability becomes a question not only of economic efficiency, but also of public health fairness. Nations like India, Brazil, China, and parts of Southeast Asia have put biosimilar insulin procurement into their national diabetes care programs, which in turn creates big-volume tender windows that tend to reward cost-competitive manufacturers.

Economic impact metrics, for 2025 total global insulin expenditure hit USD 48.7 billion, and basal insulin analogs made up 38% of that spend. When healthcare systems lean toward biosimilar insulin formulary preference, they’ve reported reductions around 22-35% in per patient yearly basal insulin costs. On top of that, patients switching to biosimilar options, especially when those are under preferred formulary arrangements saw their out-of-pocket insulin expenses fall by an average of 47%.

Despite robust regulatory frameworks and a growing pile of real-world safety evidence that backs insulin biosimilar equivalence, prescriber hesitancy, and clinical inertia continues to represent a significant barrier as real obstacles. They end up slowing voluntary uptake rates, especially once we move past payer-mandated formulary changes which are of course more forceful. Some endocrinologists, diabetologists, and primary care physicians still voice worries. The issues are usually about possible immunogenicity differences, some glycemic response unpredictability after product switching, and the lack of long-term comparative safety information, like with limited long-term comparative safety data extending beyond standard clinical trial durations, which is the same timeframe regulators tend to rely on for biosimilar approval.

These concerns are particularly pronounced in Type 1 diabetes care, where very tight glycemic control is clinically essential. In that setting, any disruption in insulin pharmacokinetics could mean a nontrivial risk of hypoglycemia or hyperglycemia. So, specialist physicians who manage complicated patients, with carefully optimized regimens, may hold back from switching products, even when regulatory bodies confirm biosimilar interchangeability. They worry that the switch could disrupt previously stabilized glycemic control that took months, and sometimes longer, to get right. Meanwhile patient advocacy organizations have sometimes opposed mandatory biosimilar switching policies, they highlight continuity of treatment and patient autonomy, especially around product choice.

Prescriber survey results point to 34% of endocrinologists reporting moderate to significant hesitancy about biosimilar switching in stable Type 1 diabetes patients. Patient surveys are even more blunt: 41% say they have concerns about the transition, and immunogenicity plus glycemic stability are the main worries. Physician-initiated biosimilar prescribing stays well below payer-mandated conversion rates.

Biosimilar insulin production is significantly more complex than manufacturing conventional small-molecule generic pharmaceuticals, it needs sophisticated recombinant DNA expression systems, plus complex downstream purification steps, and a very strict analytical characterization to show structural plus functional equivalence to reference biologics. Also, keeping the same product quality from one manufacturing batch to the next is hard, while long-term product stability remains an additional challenge, especially with different storage conditions.

Cold chain logistics are essential for insulin distribution, insulin products must be kept at 2-8°C during storage, and transport too, to preserve biological activity. That means the whole distribution infrastructure must be built out, and that can restrict market access, particularly in regions where the pharmaceutical cold chain capability is limited or inconsistent. If the supply chain has disruptions, or if temperature control is even slightly missed, the product can degrade, which brings patient safety risks, plus regulatory compliance problems. And all of that has real commercial impact for biosimilar manufacturers.

Operational challenge metrics, the constraints show up clearly. Biosimilar insulin manufacturing costs tend to sit 35-50% higher than small-molecule generics, largely because the biological production complexity doesn’t go away. Cold chain failures are implicated in about 15-25% of insulin potency loss across distribution networks where temperature control is inadequate. And regulatory batch release testing takes on average 45-90 days, which makes inventory planning tricky and reduces how quickly supply can respond.

A transformative commercial opportunity to speed up market penetration across high-growth emerging markets in Asia Pacific, Latin America, Middle East, and Africa, where diabetes is rising fast, but basal insulin therapy is still not used nearly enough compared with the number of people who are clinically eligible. In a lot of those settings the gap is stark between patients who need insulin therapy and the ones who end up receiving it, and it shows up even more strongly in low- and middle-income countries. These markets face multiple barriers like medication cost, not enough specialist access, and some cultural resistance to injectable therapy, so large groups end up managing their diabetes with poorly controlled outcomes using suboptimal oral regimens.

The lower acquisition cost of biosimilar insulin glargine directly addresses affordability challenges in price sensitive markets. Also, manufacturers that can produce locally can often reach cost structures that let them offer more competitive pricing during government tenders, which is what usually decides formulary access for publicly insured patients. Several biosimilar manufacturers have set up regional manufacturing operations, with export capabilities that reach several emerging markets at once, positioning biosimilar insulin as a scalable solution for national diabetes programs. for national diabetes care programs.

Market expansion numbers support that direction clearly. The insulin treatment gap in low- and middle-income countries impacts about 40-60% of clinically eligible patients, meaning tens of millions who require basal insulin therapy are not getting it. Meanwhile, government diabetes programs in India, China, Brazil, and South Africa have already added biosimilar insulin procurement into national formularies. In Asia Pacific, basal insulin market growth is projected to be 11.2% CAGR, and that’s the fastest expansion globally, fueled by the epidemic scale and by improvements in healthcare coverage.

Significant chances for product development in advanced insulin glargine-aldy variants, especially stuff like higher strength U-300 formulations that seem to give more consistent pharmacokinetics and smaller injection volumes. Also, there’s the idea of fixed-dose combinations, for instance pairing with a GLP-1 receptor agonist for kind of synergistic glucose control, plus some integration with digital health platforms think connected delivery devices and adherence monitoring systems.

U-300 concentration insulin glargine, it tends to show better pharmacokinetic stability, with less peak-to-trough swing and fewer nocturnal hypoglycemia episodes versus standard U-100 formulations. That creates clinically meaningful upsides for people who need very tight glycemic management, and not just “better” in a generic sense. For biosimilar U-300 versions, it’s not a simple plug-and-play situation separate regulatory approval is required as a distinct reference product, however it can still open a premium kind of positioning inside the biosimilar market.

Innovation opportunity, the numbers look strong. U-300 insulin glargine reportedly generated USD 1.4 billion globally in 2025. That’s about 18% of the total insulin glargine market value, and it’s growing around 12.3% year over year. In clinical studies, U-300 reduces nocturnal hypoglycemia by about 23-31% compared to U-100. Meanwhile, biosimilar U-300 development programs had 4 active regulatory submissions in 2025, with approvals expected during 2026-2027.

North America: Market Leadership Through Advanced Biosimilar Infrastructure and Payer Innovation

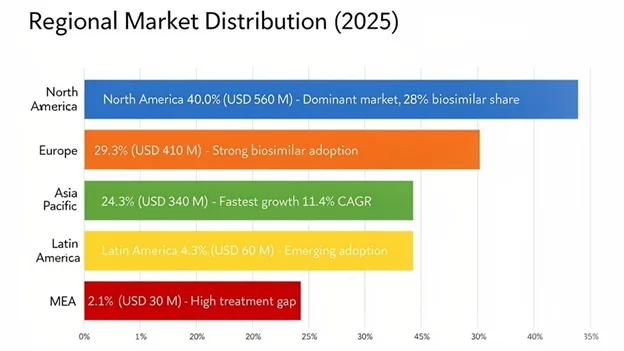

North America accounted for the largest market share at USD 560 million in 2025, and keeps a projected 8.9% CAGR through 2034, mainly because the world’s most sophisticated biosimilar regulatory framework allows interchangeability designations, plus aggressive payer driven formulary management that quietly gives structural adoption advantages, and also high diabetes prevalence, hitting 37.3 million Americans with fairly comprehensive insurance coverage that helps sustain premium therapeutic access. In fact, the United States makes up 91% of the regional market value, benefiting from Medicare plus commercial insurance frameworks, which are essentially structured to reward formulary compliance via tiered cost-sharing mechanisms. This makes biosimilar options financially attractive for patients, while also helping generate substantial savings for health plans.

The implementation of legislative insulin affordability measures, including the Inflation Reduction Act cost-sharing caps, has tweaked the pricing dynamics in a way that keeps the biosimilar economic edge for payers, while narrowing the patient level cost differences. It’s kind of reinforcing system-level incentives for formulary preference, with preference leaning on acquisition cost savings more than on what patients pay out of pocket. Canada adds 9% of regional value through provincial formulary programs that require biosimilar transitions for new patients across multiple jurisdictions, which then creates those institutional demand channels that support market growth.

Regional performance indicators too. For example, United States biosimilar insulin prescription volume reached 31.4 million units in 2025, which equals 28% of all insulin glargine prescriptions, and it’s growing at about 22% each year. Medicare Part D spending on biosimilar insulins rose from USD 180 million in 2022 to USD 640 million in 2025. On the Canadian side, provincial formulary biosimilar inclusion reached 8 of 10 provinces, creating a near-national biosimilar coverage framework.

Asia Pacific: Fastest Growth Through Epidemic Scale and Manufacturing Localization

Asia Pacific emerged as the fastest-growing region, with a projected 11.4% CAGR through 2034, and it should reach USD 340 million by 2025, mostly because the world has the largest diabetes population within the region China and India alone contribute about 200 million and 101 million cases, respectively, and creating substantial addressable market opportunities for lower-cost basal insulin therapy. At the same time, rapid economic development continues to improve healthcare accessibility, then healthcare infrastructure keeps expanding, and insurance coverage is improving across the region, so more people can reach advanced diabetes treatments that were, which were previously concentrated in developed healthcare markets.

China is leading, holding around 41% market share. This is being driven by national healthcare reforms that expand insulin reimbursement via the National Reimbursement Drug List, plus government procurement preferences for products that are made domestically or sold through local partnerships for biosimilars. India shows strong momentum, The growth is tied to wider health insurance coverage through government programs, and to the presence of globally strong biosimilar players, including Biocon Biologics.

The Asia Pacific diabetes population reached 226 million adult people in 2025, that’s 42% of the global burden, and it is still rising about 4.1% each year. Insulin use is still way under Western levels: only about 18-24% of eligible Type 2 diabetes patients are using insulin, which suggests there’s a lot of untapped capacity. The regional biosimilar insulin market increased at 19.3% annually from 2020-2025, and that’s notably faster than overall insulin market growth of 8.7%.

Product Type Insights

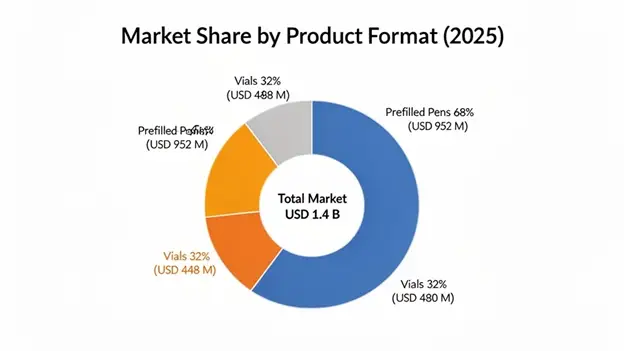

Prefilled Pens dominate the product type space at 68% market share, and were valued at approximately USD 952 million in 2025, with 9.4% CAGR expected all the way to 2034. Inside this segment there are advanced delivery device platforms that end up improving dosing accuracy, making administration more convenient, and generally lifting patient satisfaction compared with traditional vial-and-syringe administration methods. This matters a lot for elderly patients, or for people who have limited dexterity, or lower visual acuity. Also, the segment can carry premium pricing because the user experience is more refined. On top of that, there are integrated safety measures like dose memory and injection confirmation, and the whole thing matches up with digital health platforms, so it can support connected diabetes management too.

Vials & Cartridges are holding about 32% market share at USD 448 million in 2025, and they’re primarily targeted toward cost-sensitive patient segments, plus institutional procurement programs, and patients who still lean toward traditional administration methods or who are using insulin pump systems, where cartridge-based delivery is needed. Even with a lot of competitive push from pen-based systems, vials stay important in emerging markets where affordability considerations outweigh convenience factors. Also, in specialized clinical applications, they help with more precise dose customization.

Indication Insights

Type 2 Diabetes Mellitus represents the main indication segment at USD 980 million in 2025, and it’s expected to grow at a 9.6% CAGR through 2034, mirroring the biggest and quickest expanding patient group that still needs basal insulin therapy. This indication really leans on the progressive disease nature, which keeps pushing new patient initiation, plus established clinical guidelines that treat basal insulin as the preferred first injectable option. Also, there are simply large absolute patient counts, so prescription volumes stay high, and that generates strong formulary management incentives for choosing more cost-effective biosimilar products.

Type 1 Diabetes Mellitus comes in at USD 364 million in 2025 with an 8.3% CAGR through 2034, representing an absolutely insulin dependent population, with lifelong treatment needs that keep demand stable, and predictable. Biosimilar uptake has moved slower here, mostly because of prescriber and patient hesitation around product switching, given how critical this group is. growing, more real-world evidence, along with pay pressure, is pushing a gradual but consistent shift toward biosimilar alternatives.

Distribution Channel Insights

Retail Pharmacies are still the biggest distribution channel, sitting at 46% market share, with an estimated USD 644 million in 2025, which kind of shows how outpatient diabetes care is mostly handled using self-administered subcutaneous therapy. This channel has been especially helpful for biosimilar uptake, because pharmacists can step in via substitution pathways tied to interchangeability designations. As a result, conversion to biosimilar products can happen automatically at dispensing skipping the prescriber level adoption hurdles and it plugs in payer formulary preferences right away.

Hospital Pharmacies hold about 28% of the market, reaching USD 392 million in 2025. They focus on inpatient diabetes management, plus discharge prescriptions and the institutional formulary choices that may push big scale conversions across full health systems, often due to one formulary committee decision. Specialty Pharmacies are around 15% market share, and they cater to more complicated patients who need added support services, prior authorization oversight, and dedicated diabetes education programs.

The global insulin glargine-aldy injection market shows a moderately consolidated competitive structure with the top manufacturers basically covering around 70-75% of the biosimilar insulin glargine market value, thanks to established regulatory approvals in the big markets, plus competitive pricing tactics that help them land formulary preference positions, and those patient support efforts that make adoption and adherence smoother, or at least easier to sustain. So, competitive differentiation is primarily based on pricing and contract discussions with payers, the wider regulatory approval reach that opens international access, manufacturing reliability keeping supply steady and predictable, and also added services like patient education along with digital health integration.

The competitive setup keeps shifting as manufacturers pump resources into next generation product development, like higher concentration formulations, combination products, and connected delivery systems. These things create differentiation that goes past “commodity” pricing, even though people talk about it like it’s just cost. Meanwhile, the originator companies counter through authorized generic approaches, patient assistance programs, and device innovation, which helps them keep their reference product relevance in the premium segments.

March 2026: Viatris Inc. announced successfully completed a full real-world evidence study, involving approximately 15,000 patients showing equivalent glycemic results plus safety profiles for insulin glargine-aldy versus reference insulin glargine, over 18 months of ongoing treatment. This is being framed as support for wider formulary inclusion across major health systems.

February 2026: Biocon Biologics received approval from the European Medicines Agency for an expanded pediatric use of its insulin glargine biosimilar. Now it can be used in children 6 years and up who have Type 1 diabetes, which should broaden the available patient pool, and help it compete more effectively with originator products.

January 2026: Samsung Bioepis announced a partnership plan with a prominent United States pharmacy benefit manager, where its insulin glargine biosimilar is named exclusive preferred basal insulin across commercial formularies touching 12 million beneficiaries. This represents one of the largest biosimilar insulin formulary agreements to date. biosimilar insulin formulary commitments to date.

December 2025: Eli Lilly and Company rolled out an upgraded insulin glargine-aldy formulation, with better temperature stability. It allows storage at room temperature for as long as 56 days addressing cold chain logistics challenges and improves day to day convenience for patients in a range of climate settings.

List of Key Players in Global Insulin Glargine-aldy Injection Market

Global Insulin Glargine-aldy Injection Market Segments

By Product Type:

By Indication:

By Concentration:

By Distribution Channel:

By End-User:

By Patient Demographics:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

14 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.