Share this link via:

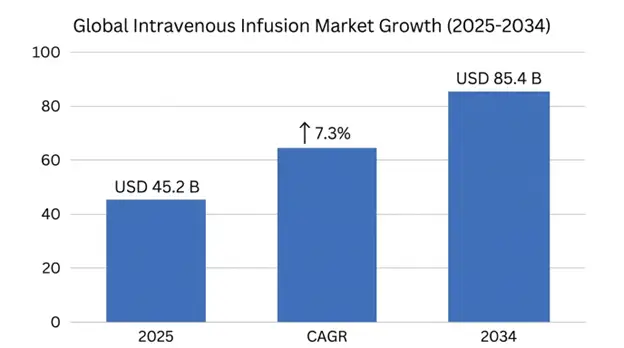

The global intravenous infusion market size was valued at USD 45.2 billion in 2025 and is projected to reach USD 48.5 billion in 2026, expanding to USD 85.4 billion by 2034, growing at a CAGR of 7.3% during the forecast period.

Intravenous infusion therapy is one of the simplest and most widely used treatment methods in contemporary clinical medicine that allows for rapid, accurate, and controlled delivery of fluids, electrolytes, blood products, drugs, and nutritional products into the systemic circulation with immediate bioavailability, predictable pharmacokinetics, and flexibility of treatment that cannot be accomplished through other means of delivery, such as orally. Technology includes anything from the simple gravity delivery system to sophisticated microprocessor-controlled electronic pumps with dose error reduction systems, smart drug libraries, wireless connectivity and integrated safety monitoring technology that work together to enhance the accuracy of medication delivery and reduce the risk of infusion errors that could lead to a life-threatening situation.

The reason for intravenous administration of a drug is primarily to ensure that the drug is not absorbed by the gastrointestinal tract, does not undergo first-pass metabolism in the liver, and has a consistent bioavailability that can be relied upon when oral drugs are not as effective, especially for large molecule biologics, chemotherapeutic agents, and emergency medications that need rapid, systemic exposure. It is an essential part of treatment in a variety of clinical settings, such as the emergency room, intensive care, operating room, oncology infusion center and more recently the home care setting where patients with chronic diseases receive complex care over the long-term.

Today's intravenous infusion systems have come a long way from simple drip-rate controllers to intelligent platforms with the ability to connect to electronic health records, verify medication administration with a barcode, calculate doses in real time, include full alarm functions, and support remote monitoring to help healthcare providers provide complex multi-drug regimens with previously unattainable accuracy and security. Smart infusion pumps with extensive drug libraries and preprogrammed concentration ranges and dose limits, along with clinical decision support alerts, have been shown to reduce potentially harmful programming mistakes by 50-70% compared to traditional infusion pumps, proving that these technologies are a crucial piece of infrastructure for safe medication administration.

The commercial environment for intravenous infusion runs far beyond the device manufacturers to cover pharmaceutical product development, specialized compounding pharmacy services, complete consumable supply chains from administration sets and vascular access devices to clinical training and certification services, and sophisticated service networks for equipment maintenance, software updates and regulatory compliance. It provides the valuable therapeutic infrastructure needed for virtually any medical specialty and care setting, ranging from a neonatal intensive care unit where micro-infusions must be precisely controlled to home infusion programs where patients can receive complex biologic therapies and maintain normal daily activities and family responsibilities.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 45.2 Billion |

| Forecast Value | USD 85.4 Billion |

| CAGR | 7.3% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Technology, Application, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Becton Dickinson, Baxter International, B. Braun Melsungen, ICU Medical, Fresenius Kabi, Medtronic, Smiths Medical |

Get more details on this report - Request Free Sample

The major factor that is going to drive the expansion in the intravenous infusion market is the increasing prevalence of chronic diseases that mandate long-term intravenous therapeutic management, such as oncological conditions, autoimmune diseases, and chronic infectious diseases in which the therapeutic agents used, such as biologic drugs, are required to be administered intravenously for effective therapeutic action. In 2025, cancer incidence was projected to hit 19.3 million new cases per year globally, and an estimated 65% of cancer patients are expected to receive treatment using any type of IV chemotherapy, targeted or immunotherapy therapy, during their cancer treatment journey, creating a sustained demand for specialized infusion infrastructure, consumables, and clinical services.

The rapid introduction of many new cost-effective, high value specialty infusions in oncology, rheumatology, gastroenterology and neurology, driven by monoclonal antibody, checkpoint inhibitor and other biologic products, has completely changed the intravenous infusion world with its need for controlled infusion protocols, extended infusion durations, specialized monitoring for infusion-related reactions and specific infusion center equipment. The number of biologic therapy approvals increased at about 22% annually from 2020 through 2025, and most of these new therapies were indicated intravenously, keeping the clinical indications and patient populations that are being infused steadily increasing.

The number of elderly aged 60 and over exceeded 1.1 billion in 2025 and is expected to reach 2.1 billion by 2050 with the number of age-related diseases requiring intravenous therapy growing exponentially. Elderly patients are more likely to have complicated comorbidities, which result in complex intravenous infusion regimens and the use of advanced pumps and consumables; chronic conditions must be managed with ongoing intravenous fluids, and severe infections will require extended use of IV antibiotics.

Key Performance Metrics:

The market for intravenous infusion is gaining significant momentum from continuous advancement in smart infusion pump platforms, which are expected to transform the medication management landscape, leading to improved medication safety, enhanced clinical workflows and better data connectivity across healthcare settings. In hospital settings, infusion-related errors account for around 54% of all potential patient-harmful medication errors, thus offering significant regulatory and institutional opportunities for implementation of dose error reduction technologies.

Smart pump systems featuring extensive drug libraries, preprogrammed concentration ranges, dose limits, and clinically triggered warnings have been shown to reduce the occurrence of potentially harmful infusion programming errors by 50-70% over traditional pumps. Smart infusion pumps with electronic health record (EHR) integration, pharmacy information systems (PIS), and clinical decision support (CDS) systems are a game-changer that allows closed-loop medication management workflows to be implemented, whereby pharmacist-verified orders are sent electronically to bedside pumps, eliminating the need for manual order transcription and offering real-time medication verification.

Thanks to the evolution of wireless connectivity, remote monitoring and predictive analytics, healthcare systems can optimize pump fleet use, forecast maintenance needs and track medication administration throughout hospital networks. Together, these connected infusion ecosystems provide comprehensive medication administration data that can help guide clinical quality improvement initiatives, regulatory compliance documentation, and pharmacovigilance programs to monitor real-world drug safety signals.

Innovation Impact Metrics:

The growing trend toward delivering complex infusion therapy outside of the hospital inpatient setting such as ambulatory infusion centers and home healthcare is a major strength of the intravenous infusion business, as pressures on healthcare systems, patient preference for outpatient care, and portable infusion technology that allows for safe outpatient use have spurred this growth and signaled the end of the era of inpatient-only delivery. The home infusion market is outpacing the overall infusion market growth rate by 6.8% per year, from 2020-2025, as payer policies increasingly favor site-of-care transitions with equivalent clinical outcomes at the same time at cost savings of 40-65% compared to hospital outpatient infusion.

Since the introduction of more portable pump technology, the standardization of compounding pharmacy practices and the development of specialized nursing services, the indications for home infusion have grown greatly to include intravenous antibiotic therapy for severe infections, parenteral nutrition for patients with intestinal failure, intravenous immunoglobulin therapy for immune disorders, biologic therapies for autoimmune diseases, and palliative care infusions for symptom management. The COVID-19 pandemic reinforced the development of site-of-care transitions by providing proof of concept for the safe management of patients in a COVID-19 world and building institutional confidence in the ambulatory infusion model.

Common characteristics of modern ambulatory infusion devices are that they are light in weight, have long battery life, are easy to use by the patient or caregiver, and are wireless and can be monitored remotely by a health care provider. Elastomeric pumps that are powered by mechanical pressure, but not electronic pumps, have been widely adopted because they are simple, inexpensive, and reliable and don't require technical support, which is often unavailable in the outpatient setting.

Patient Care Transition Metrics:

The most important challenge to the growth of the intravenous infusion market is exceptionally rigorous product regulation and high-profile product recalls that generate significant development costs, market entry barriers and compliance costs for manufacturers. The FDA and EMA have put in place demanding pre-market clearance and extensive post-market surveillance requirements for infusion pumps because of the potential for patient harm or death when the pumps malfunction, due to over-infusion, under-infusion, or failure of the pump alarm.

High-profile product recalls have been made public in the market, especially in the case of software issues with smart pumps, mechanical problems with administration sets and cyber security issues with networked devices. Classes I recall can be costly and expensive to manufacturers in terms of remediation, logistics and lost revenues, as well as the damage to brand reputation. Constant software updates, cybersecurity patch management and smooth interoperability with the hospital IT infrastructure create additional costs associated with software development and maintenance.

More than 15 large-scale Class I recalls of infusion pump systems occurred worldwide between 2023-2025, mostly due to software faults, alarm failures and security issues. In addition, compliance and remediation expenses for top-tier manufacturers with the largest number of recalled infusion systems averaged USD 45-60 million per major incident, while the time to regulatory review for novel smart infusion systems increased to 18-24 months as cybersecurity scrutiny has been strengthened.

Chronic, recurring shortages of essential intravenous medicines are a big limit on the market, and they hurt quality of care, raise costs because hospitals choose expensive alternative therapies and they create patient safety risks when the substitute treatments use different dosing, or unfamiliar steps. The FDA in 2025 reported around 300 active drug shortages at any one time with IV products often making up roughly 40-55% of those reports due to complex manufacturing, sterility rules and a small circle of suppliers.

The fact that only a few makers produce many key IV solutions and small volume parenteral items makes the system fragile to manufacturing quality problems, natural disasters or shortages of raw materials. Health systems said average annual costs were about USD 216 million tied to managing shortages, like therapeutic substitutions additional pharmacist time and emergency buying premiums.

A top market opportunity is the development of fully automated closed-loop infusion systems that combine continuous physiological monitoring with algorithmic dose adjustment to provide specific dosing targets [either drug concentrations or physiological parameters] within defined therapeutic ranges without manual clinician intervention. Randomized clinical trials have confirmed the clinical feasibility of closed-loop anesthesia delivery systems with impressive hemodynamic stability, lower drug consumption than traditional manual control, and quicker postoperative recovery; clear commercial proof-of-concept is now established in adults to support future expansion into complementary therapeutic applications.

The use of artificial intelligence and machine learning algorithms for optimization of infusion therapy present significant opportunities to improve clinical outcomes through prediction of patient-specific pharmacokinetic variability, personalized initial dosing based on patient characteristics including age, biochemical and physiological markers and dynamic adjustment of maintenance infusion rates based on serial assessment of real-time clinical response data. Population pharmacokinetic modeling using electronic health record data allows for precision dosing strategies for therapeutic drug monitoring applications.

Our worldwide data shows that by 2025, only 35% of hospitals are using full bi-directional EHR integration to their infusion pump fleets, meaning there is a massive untapped upgrade cycle market. Infusion Pump Interoperability Software & Integration Services Market Analysis Infusion Pump Interoperability Software & Integration Services Market to Grow at 14.5% CAGR Through 2034

The chance to build small, on-body infusion units that give continuous drug delivery during normal daily life is a big market opening, it removes the limits on movement you get with the old pole mounted pumps. Wearable bolus injectors and devices stuck to the body went beyond just insulin, now they are used for continuous pain meds, blood thinners, and some specialty biologic therapies, and more things in that area.

The market for wearable infusion gadgets hit USD 4.2 billion in 2025 and has been growing about 14.8% each year, pushed by diabetes care and niche drug delivery uses. Patients, when they switch from inpatient to ambulatory infusion routines reported quality of life scores up, by roughly 23 points on average, which suggests real benefit, although some details vary by study.

Since infusion pumps increasingly depend on hospital wireless networks for drug list updates and to tie into EHR systems, they have become prime targets for cyber-attacks. A big new trend is to put military level cyber security straight into the device firmware, including a zero-trust style architecture, end to end encryption and secure boot mechanisms that prevent, unauthorized code from running.

IT teams in hospitals now treat cyber security posture as equally important to clinical features when they choose new equipment, and sometimes they even put it first. Requests for proposals that mention security for infusion systems jumped about 300 % from 2022 to 2025. More than 60 % of the smart pumps introduced in 2025 came with integrated secure boot tech and real time network anomaly detection.

The intravenous infusion market is being kind of reshaped by faster entry of biosimilar versions for the leading original biologics, including biosimilars for bevacizumab, trastuzumab, rituximab and infliximab, and this competition has cut buying costs somewhere between 15–45% in markets where rivals are active, enabling health systems to treat larger groups of patients within tight budgets expanding overall infusion therapy use volumes a bit more than before.

Biosimilar infliximab took up about 62% of fresh prescription starts in European markets and 38% in the United States by 2025, causing average price cuts of around 28% off the pricing of the original product. Total infusion procedure volumes grew 12.4% per year between 2020 - 2025 despite average biologic medicines price falls of 18%.

North America: Market Leadership Through Advanced Infrastructure and Safety Mandates

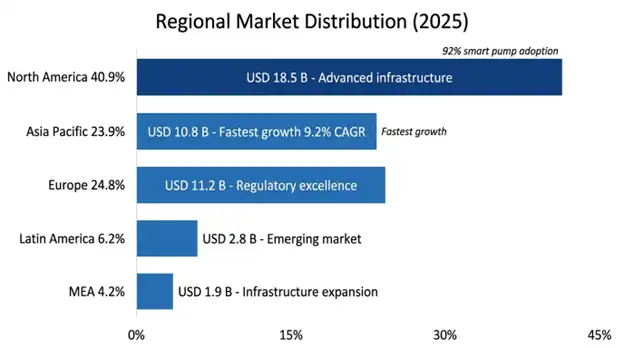

North America was holding the biggest slice of the market at USD 18.5 billion in 2025, and it keeps a projected CAGR of 6.8% through 2034. Regional dominance reflects very advanced healthcare frameworks, that often require smart infusion pumps with dose error reduction systems and broad insurance for new therapies through Medicare and commercial payers, high rates of chronic illness pushing ongoing infusion therapy needs and an early pick up of new tech like EHR integrated pumps and outpatient infusion programs.

The United States makes up about 85% of the regional market value supported by huge healthcare spending and a well-built specialty pharmacy setup. Medicare policies covering home infusion have set up reimbursement bases enabling the market to grow, with Medicare home infusion benefit spending reaching USD 1.8 billion in 2025. Use of smart pumps with dose error reduction systems hit 92% of US acute care hospitals which fuels a profitable replacement and upgrade market.

Key Performance Indicators:

Asia Pacific: Exponential Growth Through Healthcare Modernization and Disease Burden

Asia Pacific turned into the fastest expanding regional market with a compound annual growth rate of 9.2% through 2034, reaching USD 10.8 billion in 2025. Regional growth is pushed by a huge chronic disease load with China and India together accounting for 38% of global diabetes cases expanding healthcare infrastructure investment, a growing middle class seeking better medical care and health reform moves that widen insurance cover for specialty procedures.

China leads the region with about 41% portion of the market, driven by government health reforms that broaden access to biologic therapies, heavy spending on hospital infrastructure, and a fast rise in oncology treatment capacity. India is showing faster uptake through expanding private hospital chains, increasing health insurance penetration, and the creation of high-volume, cost-efficient delivery approaches.

Regional Growth Drivers:

Product Type Insights

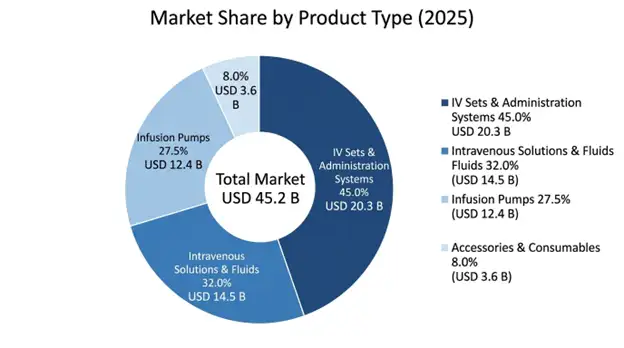

Intravenous sets and administration systems take the lead in the market with about 45% share, valued at USD 20.3 billion in 2025 and growing at 7.8% CAGR through 2034. This group covers primary and secondary administration sets, extension lines and needleless connectors plus the special tubing you need for each infusion procedure. Their dominance comes from being consumable, they must be replaced for every patient encounter to avoid healthcare associated infections, which makes a steady recurring revenue stream that resists economic ups and downs.

Infusion pumps are the highest value part of the market at USD 12.4 billion in 2025 and expand to 8.2% CAGR through 2034. Even though they are capital equipment with longer lifecycles, ongoing tech upgrades, conversions to smart pumps and wider clinical uses keep driving high value growth. Volumetric pumps make up 48% of pump revenues, syringe pumps 28% and ambulatory pumps 24% with the fastest growth, about 11.3% CAGR.

Intravenous solutions and fluids hold roughly 32% market share at USD 14.5 billion in 2025, including large-volume parenteral, small-volume parenteral and total parenteral nutrition formulations. This segment keeps essential demand characteristics since these products are needed for nearly every intravenous therapy application, so demand stays relatively stable.

Application Insights

Oncology and Chemotherapy are the largest application segment, about 32% market share and valued near USD 14.5 billion in 2025 with a 9.6% CAGR through 2034. The exact delivery needs for very toxic chemotherapeutic agents and targeted biologic therapies need advanced infusion pumps with full safety features, this drives premium pricing and growth that keeps going as cancer rates increase around the world.

Clinical Nutrition and Parenteral Feeding make up roughly 21% of the market, about USD 9.5 billion in 2025, serving patients with intestinal failure, critical illness and malnutrition who need complete nutritional support given intravenously. The segment gains from more awareness of how malnutrition affects outcomes and the steady expansion of critical care capacity.

Pain Management and Anesthesia represent close to 18% market share at about USD 8.1 billion in 2025, they rely heavily on patient-controlled analgesia pumps that let patients give themselves doses within the safety limits set by physicians.

End-User Insights

Hospitals and acute care Facilities are the biggest end user segment with 65% of the market, valued at USD 29.4 billion in 2025, covering inpatient wards, intensive care units, emergency departments and hospital-based outpatient infusion centers. The segment keeps dominance because complex cases tend to concentrate there requiring intensive monitoring and there is established reimbursement for procedures at the facility, plus a broad infrastructure that supports therapies that are high risk.

Home healthcare settings take about 16% of the market, worth USD 7.2 billion in 2025 and they show a 10.5% CAGR through 2034, growing the fastest among end user segments. Expansion is pushed by cost containment pressures patient preferences, and tech advances that let complex therapies be administered safely in the home.

The global market for intravenous infusion is moderately too highly concentrated, with around seven main firms holding roughly 58-65% of the market value through a variety of different product lines that include infusion pumps, sets for administration, IV solutions, and service packages combined, they offer. Competitive edges come from tech innovation, notably pump features that are smart and the way they link electronic health records, broad safety functions and big distribution networks and long-term service deals with major health systems

There are more strategic partnerships now between device makers, drug companies and health IT firms, making combined platforms that try to cover full therapy delivery needs, M&A activity is aimed at buying specific technologies, getting into new regions and integrating vertically along the infusion therapy value chain.

March 2026: Becton Dickinson rolled out a next generation Alaris smart infusion system, that has built in two-way Epic EHR linking, letting a kind of closed loop auto programming and making clinical notes more automatic, the unit also brings stronger cybersecurity measures and a larger drug library with about 2,400 clinical support routines.

February 2026: Baxter International got FDA ok for an ultra-compact pump for ambulatory use, made for home-based cancer therapy, it has cloud remote monitoring so clinicians can watch therapy delivery and patient condition in near real time.

January 2026: ICU Medical said it made a strategic tie up with a top healthcare cybersecurity firm, to fold zero trust network design into the Plum 360 pump family addressing rising worries around network weak spots on medical devices.

December 2025: B. Braun finished a 150-million-dollar expansion of its IV solutions plant in Southeast Asia, doubling output to catch up with the fast-growing local need for sterile fluids and special parenteral nutrition mixtures.

November 2025: Fresenius Kabi launched administration sets with RFID that auto fill lot numbers and expiry dates into hospital inventory systems, this helps streamline supply chain work and paperwork for regulators.

List of Top Companies Intravenous Infusion Market

Global Intravenous Infusion Market Segments

By Product Type:

By Technology:

By Application:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

13 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.