Share this link via:

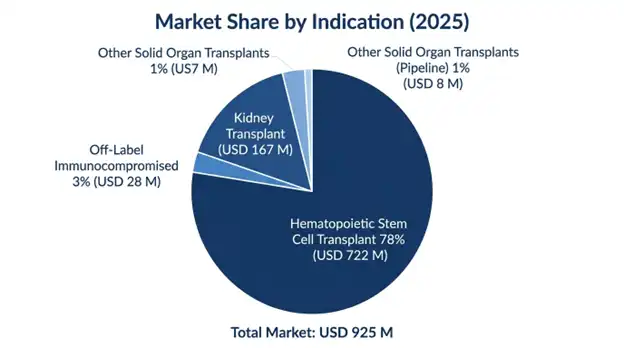

The global letermovir market size was valued at USD 925 million in 2025 and is projected to reach USD 1.02 billion in 2026, expanding to USD 2.18 billion by 2034, growing at a CAGR of 9.9% during the forecast period (2026-2034).

Letermovir is a groundbreaking first-of-its-kind antiviral compound that has revolutionized CMV prophylaxis in high-risk immunocompromised patients owing to its unique mode of action through inhibition of the viral DNA terminase complex rather than the classical viral DNA polymerase pathway. The drug has been developed and marketed by Merck & Co. as Prevymis and acts selectively on the viral terminase complex of UL51, UL56, and UL89 gene products, which are responsible for viral DNA cleavage, processing, and encapsidation in CMV infection. This pharmacological distinction has eliminated cross-resistance to other anti-CMV agents such as ganciclovir, valganciclovir, foscarnet, and cidofovir, along with the crucial absence of myelosuppression, the dose-limiting factor for other anti-CMV regimens.

The clinical importance of letermovir extends beyond its antiviral action by overcoming major drawbacks in the field of transplantation wherein CMV reactivation is the most significant infectious complication post-allogeneic hematopoietic stem cell transplantation or solid organ transplantation. In patients who are seropositive for CMV infections and are left untreated, the frequency of developing end-organ manifestations such as pneumonitis, colitis, retinitis, and encephalitis is about 60 to 80%, while indirect immunomodulatory effects also lead to greater susceptibility to bacterial/fungal co-infections, acute and chronic graft rejection, graft versus host disease, and mortality rates secondary to the transplantation procedure. Conventional approaches of ganciclovir or valganciclovir for prophylaxis had been limited by the hematologic toxicities of neutropenia and thrombocytopenia which hinder post-transplant hematologic reconstitution and engraftment.

FDA approval of Letermovir in November 2017, followed by approvals across the globe, has created a benchmark treatment modality for CMV prophylaxis among adult CMV-seropositive recipients of allogeneic hematopoietic stem cell transplantations, along with the more recent indication in kidney transplantation for patients at higher risk based on donor-positive/receiver-negative serostatus. Market dynamics have been further impacted by various clinical development programs under way, seeking applications of the compound in other solid organ transplant patient groups and pediatric patients, among others with severe immunosuppression conditions.

The increasing demand for the product is driven not only by rising global transplant patient numbers but also by the shift from a more reactive strategy of using preemptive therapy to a proactive strategy of universal prophylaxis, facilitated by the safety of letermovir. The shift in practice has far-reaching implications not only clinically, but also financially, making the product a vital part of modern transplant treatment protocols.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 925 Million |

| Forecast Value | USD 2.18 Billion |

| CAGR | 9.9% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

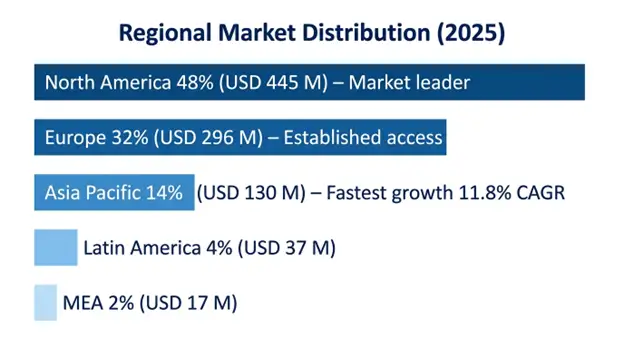

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Route of Administration, Indication, Patient Demographics, End-User, Distribution Channel |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Merck & Co. Inc., AiCuris Anti-infective Cures GmbH |

Get more details on this report - Request Free Sample

The main factor behind the continued growth of the letermovir market lies in the consistent growth in the number of allogeneic hematopoietic stem cell transplantation as well as solid organ transplantation worldwide, thereby increasing the number of patients requiring CMV prophylaxis or preemptive treatment. The global numbers of allogeneic HSCT have been consistently growing at an average of more than 5.5% per year to reach nearly 58,000 procedures performed annually by 2025, attributed not only to new indications, such as non-malignant hematological conditions, primary immune deficiencies, and metabolic diseases, but also to technical improvements in donor matching, conditioning, and support techniques, which enable transplantation in older and multi-comorbidity patients.

The epidemiological basis of the market lies in the high rate of CMV positivity among adults worldwide, where seropositivity rates range from 45-70% in developed nations and exceed 90% in numerous developing nations, implying that most transplant patients carry latent CMV infection that is prone to reactivation during immunosuppression. The group at the highest risk of developing clinical CMV disease is the group of CMV-seropositive recipients regardless of the serostatus of their donors, accounting for 65-75% of allogeneic HSCT recipients in North America and Europe, even higher proportions in Asia, Latin America, and Africa.

The opportunity for incremental growth through solid organ transplantation is tremendous in relation to development plans, with over 95,000 kidney transplants, over 32,000 liver transplants, over 8,500 heart transplants, and nearly 6,800 lung transplants carried out globally each year. All solid organ transplants pose significant potential for CMV complications, specifically at high-risk donor positive and recipient-negative serostatuses in 20% - 25% of all kidney and liver transplants, which present a 60% - 80% risk for developing CMV disease without prophylaxis. The FDA's approval of letermovir for kidney transplantation prophylaxis demonstrates that there is an acceptable regulatory process for achieving more such solid organ transplant indications during the forecast period.

Key Performance Metrics:

The rapid clinical uptake of letermovir is a direct result of its ability to overcome the critical safety drawbacks inherent to previous CMV prophylactic drugs, which were the limiting factor in optimizing patient care. The standard-of-care drugs ganciclovir and valganciclovir have been shown to induce neutropenia in 15-35% and thrombocytopenia in 8-20% of their recipients, a serious issue when considering that transplant recipients are simultaneously working on their hematological recovery, administering immunosuppressive medications, and at risk of potentially deadly bacterial and fungal infections due to treatment-related cytopenias.

The Phase III SOLSTICE study established letermovir's superior clinical effectiveness via a statistically significant decrease in the primary composite endpoint of clinically significant CMV infection through week 24 following transplant, where 21.2% of letermovir recipients reached the primary endpoint as opposed to 37.5% of the placebo group. This translated into a 16.3 percentage point and 43.5% absolute and relative risk reduction, respectively. Importantly, this effect occurred with no accompanying myelotoxicity typical of previous drugs, as letermovir induced adverse event rates like placebo, without neutropenia, thrombocytopenia, or nephrotoxicity.

Real-world evidence trials performed at prominent transplant centers have been successful in validating the results of the pivotal trial, proving that letermovir is effective in high-risk groups such as haploidentical recipients, cord blood grafts, and patients with active graft-versus-host disease on intense immunosuppressive treatment. The real-world evidence trials have also been successful in proving some secondary advantages, such as lower costs for healthcare resources due to fewer CMV-related admissions, less frequent commencement of antiviral therapy for prevention purposes, and better survival outcomes.

Clinical Impact Metrics:

The most significant commercial constraint that limits letermovir market penetration involves its relatively high acquisition cost versus generic CMV prophylaxis options, which creates reimbursement obstacles especially in price sensitive markets and in healthcare systems that have tight, restrictive pharmaceutical budgets. A typical 100-day letermovir prophylaxis course costs around USD 42,000 to 48,000 using US list pricing, whereas generic valganciclovir comes in at roughly USD 3,500 to 5,000 for the same duration. That gap is about 10 to 12 times higher, which then means payers usually need strong pharmacoeconomic reasons for approval and eventual formulary placement.

Whereas detailed Pharmacoeconomics studies have consistently supported the cost-effectiveness of letermovir due to cost savings from fewer treatments for CMV diseases, lower rates of hospitalization, lower secondary infection rates, and better outcomes in transplants, payer uptake varies widely according to varying levels of cost-effectiveness thresholds and budget impact assessments in respective healthcare systems. A few countries within Europe have adopted managed-entry programs with pay-for-performance pricing or limited use in certain high-risk patient sub-groups, thus confining market uptake to a smaller proportion than than what is permitted under the full FDA indication. Emerging economies, which are characterized by a high prevalence of CMV infection and inadequate healthcare infrastructure, also face significant barriers to access.

The biggest growth opportunity in the upcoming years would be the attainment of regulatory approval of letermovir for further solid organ transplant indications, which have a patient population that is multiple times larger compared to the approved allogeneic HSCT indication. The FDA approval in 2023 for kidney transplant patients demonstrated that letermovir can be used for solid organ transplants, and other Phase III studies running through 2026-2027 for liver, lung, and heart transplants are also underway.

Expanding pediatric indications is yet another promising growth area, with approval from the FDA now obtained for patients aged 12 years and above who weigh at least 40 kg, with further ongoing studies examining the lowering of the age threshold. Pediatric patients receiving allogeneic HSCT for malignancies, bone marrow failure syndromes, and primary immune deficiency conditions constitute an important clinical and under-served commercial area where effective CMV prophylaxis treatments have not previously been available.

North America: Market Leadership Through Advanced Healthcare Infrastructure and Early Adoption

North America led the letermovir market and accounted for a share worth USD 445 million, or 48% of the global market revenue. This was due to the timely FDA approval, fast adoption in leading academic transplant centers, wide coverage through commercial payers and Medicare, as well as the presence of the highest volume of transplant programs worldwide. The number of annual allogeneic HSCT cases in the US is close to 9,200, of which more than 65-70% is sero-positive recipients of CMV, resulting in letermovir prophylaxis penetration exceeding 88% at transplant centers.

North America enjoys favorable reimbursement frameworks for specialty medicines in transplantation, where Medicare Part B, as well as various commercial insurers, provide coverage, subject to preauthorization according to approved indications. Patient support programs have been actively developed around letermovir by specialty pharmacies, ensuring proper adherence and effective clinical coordination.

Asia Pacific: Fastest Growth Through Transplant Program Expansion and High CMV Seroprevalence

The Asia Pacific region is the fastest-growing regional market with a forecasted CAGR of 11.8% between 2025 and 2034 owing to the rising number of transplant programs, near-total seroprevalence of CMV resulting in a considerable at-risk population, healthcare infrastructure development, and increased awareness about the clinical significance of CMV infection. China dominates the regional market growth due to more than 12,000 allogeneic HSCT transplants annually, accounting for the second-highest national transplant volume in the world.

The letermovir market is highly concentrated due to Merck & Co. Inc.'s exclusive rights for the manufacture and marketing of letermovir across all approved markets, making it the only product with such approval within the forecast period. Letermovir has patent protection for its composition and method of use up until 2031-2033 in major markets, thus providing protection against competition within the forecast period since there are no competing brands for letermovir. Its competitive advantage is based on superior efficacy and safety compared to other treatments like valganciclovir as a prophylaxis and preemptive treatment.

March 2026: Positive top-line Phase III trial results for letermovir in preventing CMV disease in liver transplant recipients were reported by Merck, showing strong efficacy and good safety data, in support of filing for registration towards the end of 2026.

January 2026: A supplementary filing was received for the use of letermovir in children less than 12 years old, and an EMA decision is expected in Q4 2026 following completion of pediatric PK assessment.

October 2025: Publication of real-world evidence on the efficacy of letermovir in haplo-HSCT recipients showing a 68% reduction in relative risk of CMV reactivation.

List of Key Players in Global Letermovir Market

By Route of Administration:

By Indication:

By Patient Demographics:

By End-User:

By Distribution Channel:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

19 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.