Share this link via:

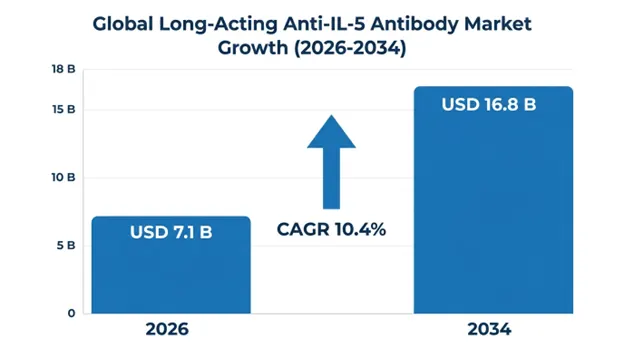

The global long-acting anti-interleukin-5 (IL-5) antibody market was valued at USD 6.2 billion in 2025 and is projected to reach USD 7.1 billion in 2026, expanding to USD 16.8 billion by 2034, growing at a CAGR of 10.4% during the forecast period.

Long-acting anti-IL-5 antibodies are among the newest classes of biologic drugs designed to block IL-5 pathways over extended periods for the treatment of eosinophilic inflammation. Indeed, anti-IL-5 agents have revolutionized the treatment of numerous pathological conditions, including eosinophilic asthma, eosinophilic granulomatosis with polyangiitis, chronic rhinosinusitis with nasal polyps, and other diseases characterized by eosinophil excess. IL-5 is one of the main cytokines responsible for the regulation of eosinophil proliferation, activation, and survival.

There are two broad categories of mechanisms in treatment therapies. One of these is neutralization therapy of IL-5, using drugs such as mepolizumab and reslizumab. This works by binding circulating IL-5 cytokines and preventing activation of receptors responsible for eosinophil growth and survival. On the other hand, IL-5 receptor alpha-blocking drugs such as benralizumab inhibit IL-5 signaling by binding to IL-5 receptors on eosinophils and basophils. Additionally, this blockade promotes antibody-dependent cell-mediated cytotoxicity resulting in almost complete depletion of eosinophils.

Long-acting properties of such drugs are made possible by innovations in antibody engineering technology, allowing for dose intervals of up to four to eight weeks, with potential for quarterly or half-yearly dose regimens in the future. Such advancements in antibody technology include Fc-engineering, albumin-fusion systems, and sustained-release formulations.

The market extends beyond biologic drug sales to include integrated care ecosystems involving biomarker-based patient selection, digital disease monitoring, patient support programs, and value-based pricing. that is based on patient selection by means of biomarkers, digital monitoring of the disease, support programs, and value-based pricing. Health economic advantages of these drugs are illustrated by fewer exacerbations of the disease, less use of steroids, fewer hospitalizations, and improved disease management.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 6.2 Billion |

| Forecast Value | USD 16.8 Billion |

| CAGR | 10.4% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Indication, Mechanism of Action, Route of Administration, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | GlaxoSmithKline plc, AstraZeneca plc, Teva Pharmaceutical Industries Ltd., Sanofi SA, Regeneron Pharmaceuticals Inc. |

Get more details on this report - Request Free Sample

Key factors contributing to growth in the anti-IL-5 antibodies market include the increasing prevalence of eosinophilic inflammatory diseases around the world, notably severe eosinophilic asthma, which is experienced by a large percentage of the global asthmatic population. Awareness of the heterogeneity of asthma as an inflammatory condition with specific inflammatory endotypes has led to increased use of biologic drugs based on biomarkers, particularly those patients suffering from high levels of eosinophils in the blood. Patients with severe eosinophilic asthma are a costly portion of the patient population because of their high rate of asthma exacerbations, repeated hospitalization, and need for systemic corticosteroids with various side effects.

Anti-IL-5 biologics have shown excellent clinical results with regards to reduction in exacerbations, improvement of lung functions, and reduction of corticosteroids. Furthermore, additional conditions such as eosinophilic granulomatosis with polyangiitis, hyper eosinophilic syndrome, and chronic rhinosinusitis with nasal polyps have contributed to an even larger market opportunity.

Key Performance Metrics:

Another key factor contributing to the adoption of anti-IL-5 biologics is the increasing recognition of the cumulative toxicity burden associated with chronic administration of oral corticosteroids in severe eosinophil disorders. Around 30-40% of severe asthmatics need maintenance oral corticosteroid treatment, and cumulative exposure to low oral prednisolone equivalents (daily dose of 5-7.5 mg) results in significantly increased rates of adverse events such as osteoporosis, adrenal insufficiency, diabetes mellitus, cardiovascular diseases, and immunosuppression, thus thereby creating additional morbidity and healthcare costs that often exceed the direct cost of disease treatment.

The steroid-sparing clinical benefit of anti-IL-5 agents was demonstrated in several pivotal studies, showing 75% median dose reductions by benralizumab in the ZONDA trial and 50% median dose reductions and 14% full elimination achieved with mepolizumab in the SIRIUS trial. This steroid-sparing effect contributes significantly to preventing steroid-induced co-morbidities, which, in turn, creates annual cost savings of USD 8,400-14,200 per patient, thus supporting pharmacoeconomic cases for anti-IL-5 biologics reimbursement.

Steroid-Sparing Evidence Metrics:

One of the key barriers to the adoption of anti-IL-5 antibodies of anti-IL-5 antibodies is the high cost due to premium pricing strategies that create significant access challenges for cost-sensitive healthcare systems or in environments where there is little biological coverage capacity. The annual cost of treatment runs between $28,000-$38,000 in the US, before rebates, with European annual list prices running at between 15,000-24,000 Euros a year, presenting affordability problems to people who do not have adequate insurance coverage.

Health Technology Assessment organizations such as the National Institute for Health and Clinical Excellence (NICE), Haute Autorité de Santé (HAS), and their equivalents in other European markets, apply incremental cost-effectiveness ratio thresholds of $20,000–$30,000 per quality-adjusted life year (QALY), making reimbursement approval for anti-IL-5 biologics challenging without managed access agreements or outcome-based pricing arrangements., thus requiring patient access agreements and outcome-based arrangements.

Access Challenge Metrics:

The upcoming patent expirations for the first wave of IL-5 inhibitors is a key structural challenge in terms of sustainability of income streams, since mepolizumab will expire between 2027 and 2030, while the patents for reslizumab have similar expiration times. The need for high expertise in the production of biosimilars, especially of the more complex monoclonal antibodies biosimilars, might restrict the number of biosimilar competitors, resulting in less price competition than in the generic pharmaceutical case.

Biosimilar Impact Projections:

Significant commercial opportunities exist through the expansion of anti-IL-5 indications into chronic obstructive pulmonary disease with eosinophilic phenotypes, potentially addressing 96–144 million patients worldwide out of the approximately 480 million global COPD population. About 20-30% of COPD patients exhibit high levels of blood eosinophils exceeding 300 cells per microliter linked with high rates of exacerbation and increased lung function deterioration, presenting the greatest single indication extension potential due to COPD’s much greater prevalence than severe asthma.

The RESOLUTE trial of Benralizumab and METREX/METREO trial of mepolizumab have formed the basis of COPD development, with regulatory filings expected in 2026-2027 that would increase the market size by 300-500%. At the same time, eosinophilic gastrointestinal disorders, such as eosinophilic esophagitis, gastritis, and colitis, present emerging opportunities, with dupilumab’s eosinophilic esophagitis approval confirming biologic treatment efficacy and setting a precedent for reimbursement of biologic therapies targeting eosinophilic gastrointestinal disorders.

Indication Expansion Metrics:

Significant opportunities exist in the development of ultra-long-acting anti-IL-5 formulations that aim for quarterly or semi-annual dosing via novel Fc-engineering, albumin fusion approaches, and controlled release mechanisms. YTE mutations enhance neonatal Fc receptor binding under acidic endosomal conditions, avoiding lysosomal destruction and recycling of antibodies back into the bloodstream, doubling their half-lives to over 80 days and allowing for 26-week dosing intervals.

Such ultra-extended formulations align well with scheduled specialist follow-up visits, and at the same time create unique market positioning despite biosimilar threats. Moreover, combination biologics targeting multiple inflammatory mediators of the type 2 pathway at once are precision medicine prospects for patients with dual eosinophilic and allergic traits, which account for 35-45% of biologic-eligible severe asthmatics.

Innovation Opportunity Metrics:

The anti-IL-5 therapeutic landscape is evolving toward precision medicine approaches, transitioning to precision medicine frameworks involving the application of biomarkers, digital health technologies, and treat-to-target approaches where achieving clinical remission, rather than merely managing symptoms, serves as the primary treatment objective. Patient stratification tools use sophisticated combinations of biomarkers, such as blood eosinophil numbers, exhaled fractional nitric oxide concentrations, history of exacerbation, and even genomic markers to identify the most effective biologic therapy for patients.

Treat-to-target programs establish clinical remission as zero exacerbations, zero maintenance oral corticosteroids, stable lung function, and normalized outcomes reported by patients; in this context, long-term administration of anti-IL-5 agents can help achieve these goals because of their unique ability to provide eosinophil depletion without trough level variation. Digital health technologies make possible real-time monitoring of patients between doses through applications, digital spirometry, and remote symptom tracking.

Patient-centric healthcare delivery models emphasize convenience, self-reliance, and minimization of healthcare system interfaces through home-administration programs facilitated by extensive patient education, nursing training programs, and electronic compliance tools. Extended-release medicines with an 8-week or longer period provide effective home care while ensuring professional supervision through routine visits to specialists synchronized with medication cycles.

North America emerged as the leading regional market, accounting for USD 2.8 billion in 2025, and is poised to retain a strong compounded annual growth rate of 10.1% till 2034. This is attributable to extensive Medicare Part B and commercial insurance coverage for physician-administered biologicals, a developed specialist network with sound knowledge in biologic prescribing, and the United States acting as the key launch market for novel IL-5 inhibitors. North America enjoys a strong advantage owing to highly aggressive direct-to-consumer marketing campaigns and well-developed clinical trial facilities.

United States Performance Metrics:

Europe held a value of USD 2.0 billion in 2025, with a forecasted CAGR of 9.8% from 2025 to 2034, showing high adoption rates in clinical settings but limited by health technology assessment considerations and managed access agreements that introduce 12-24 months of delays from receiving approval to market launch. Germany, France, and the United Kingdom combined make up 58% of Europe’s revenue, with varying processes for payment.

European Market Characteristics:

The fastest growing regional market has been Asia Pacific, estimated to have a CAGR of 12.8% until 2034 and to grow to reach USD 1.1 billion in 2025. The growth in regional markets is fueled by increasing prevalence of allergies, developing expert networks and insurance reimbursement in Japan, South Korea, Australia, and urban China. Japan remains a leading market for biologic therapies targeting eosinophilic diseases due to coverage under National Health Insurance Scheme, whereas the high growth rate can be observed in China.

Regional Growth Drivers:

Benralizumab is the leading product segment, accounting for a 46% market share, valued at USD 2.9 billion in 2025, with a growth rate of 11.8% CAGR during the forecast period until 2034. The novel mode of action using IL-5 receptor alpha antagonism in combination with potent antibody-dependent cellular cytotoxicity resulting in rapid eosinophil clearance, along with an 8-week maintenance schedule being the most convenient treatment regimen available to date, contributes to commercial success.

The pioneer drug of the class, Mepolizumab, has a market share of 40%, valued at USD 2.5 billion. It is the first anti-IL-5 monoclonal antibody with indications covering severe eosinophilic asthma, eosinophilic granulomatosis with polyangiitis, hyper eosinophilic syndrome, and chronic rhinosinusitis with nasal polyps. Reslizumab covers 8% of the market share and is used in intravenous administration.

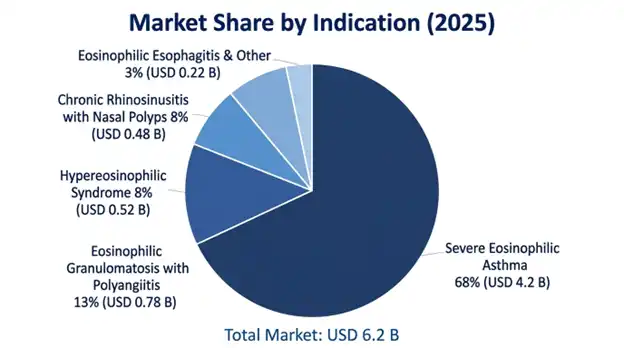

Severe eosinophilic asthma represents the largest indication segment with USD 4.2 billion in 2025, and it is set to hit 10.1% CAGR through 2034, it is basically the foundational indication, and it also has the largest patient base plus established clinical proof. Eosinophilic granulomatosis with polyangiitis accounts for approximately USD 780 million, with a 13.8% CAGR. Next Hyper eosinophilic Syndrome comes in at USD 520 million and shows 12.4% CAGR. Chronic Rhinosinusitis with Nasal Polyps is at USD 480 million, and the CAGR is 15.6%, which makes it the fastest-growing approved indication.

Subcutaneous Injection holds the largest share, accounting for 82%, with a valuation of USD 5.1 billion, owing to the ease associated with self-administration and fewer clinic visits needed. Intravenous Infusion constitutes 18% share and comprises reslizumab delivery as well as other instances necessitating prompt systemic action.

The global anti-IL-5 antibodies segment is The market is highly concentrated, with three major companies accounting for nearly 94% of total sales owing to robust intellectual property protection, substantial clinical proof across various indications, proven international commercial footprint, and ongoing research pipelines for indication expansion and second-generation therapies. Competition in the market is primarily based on differentiation through clinical performance, dosing ease, broad range of indications, and patient assistance programs as opposed to pricing wars.

April 2026: AstraZeneca reported positive findings from Phase III clinical trial of benralizumab in the management of chronic obstructive pulmonary disease with an eosinophilic phenotype, where there was 28% decline in the number of exacerbations per year. The filing plans for US and EU markets are scheduled for Q3 2026.

March 2026: Approval granted by FDA to GlaxoSmithKline for mepolizumab in eosinophilic esophagitis following completion of Phase III trial, showing statistically significant improvements in both symptoms and histological outcomes in biomarker selected patients. This marks largest extension of indication since original asthma approval.

February 2026: First filing of biosimilar version of IL-5 inhibitor reslizumab filed by Teva Pharmaceutical at FDA, with expectation of receiving approval decision in Q4 2026.

January 2026: AstraZeneca initiated a Phase II trial for every 12 weeks administration of subcutaneous benralizumab at dose of 100 mg, with a promising pharmacokinetic profile for sustained eosinophil suppression.

List of Key Players in Global Long-Acting Anti-IL-5 Antibody Market

Global Anti-IL-5 Antibody Market Segments

By Product Type:

By Indication:

By Mechanism of Action:

By Route of Administration:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

15 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.