Share this link via:

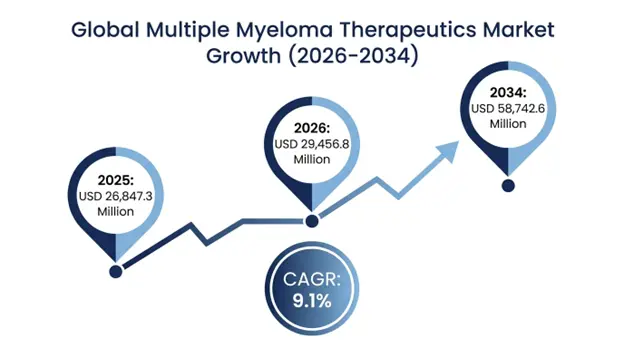

The size of the global multiple myeloma therapeutics market is estimated to be USD 26,847.3 million in 2025 and USD 29,456.8 million in 2026 and projected to reach USD 58,742.6 million in 2034, with a strong CAGR of 9.1% over the forecast period 2026-2024.

Multiple myeloma is the second most prevalent hematologic malignancy in the globe; it is a condition of malignant growth of plasma cells in the bone marrow causing osteolytic bone defects, kidney disorders, anemia, and hypercalcemia. The cancer makes up about 1.8% of all cancers and 10-15% of hematologic malignancies worldwide, where the International Myeloma Foundation reported about 176,404 new diagnoses and 117,077 deaths in 2024. Elderly groups are the most susceptible to the disease, with a median age of diagnosis of 69 years old, and shows significantly higher incidence rates in African Americans than in Caucasian populations.

Over the last two decades there has been a radical change in the therapeutic landscape, as traditional chemotherapy regimens, with median survival of 3-4 years, have been replaced with advanced multi-modal treatment approaches that have seen median overall survival of newly diagnosed patients rise to 8-10 years. This paradigm shift includes sequential introduction of immunomodulatory drugs (lenalidomide and pomalidomide), proteasome inhibitors (bortezomib and carfilzomib), monoclonal antibodies (daratumumab and isatuximab) and breakthrough cellular immunotherapies (CAR-T cell therapies and bispecific T-cell engagers)

This rapid growth pattern in the market is indicative of the intersection of increased disease burden with the global aging of all populations, the growing number of treatment-eligible patients with the advent of better diagnostic tools, regulatory endorsement of breakthrough immunotherapies and the shift in treatment paradigm towards continuous treatment modalities with earlier intervention using novel agents. More than 40 different treatment regimens are approved in clinical practice guidelines and there are now over 15 FDA-approved drug classes, which has a complex decision algorithm to balance efficacy, safety profiles, patient characteristics, and economic factors.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 26,847.3 Million |

| Forecast Value | USD 58,742.6 Million |

| CAGR | 9.1% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

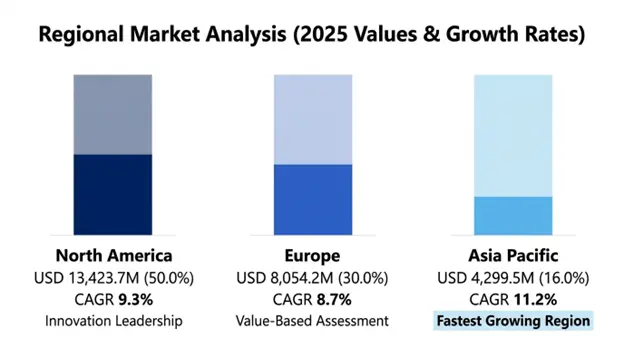

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Drug Class, By Line of Therapy, By Route of Administration, By Treatment Setting, By Distribution Channel, By End User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Spain, Italy, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Johnson & Johnson, Bristol Myers Squibb, Takeda Pharmaceutical, Amgen Inc., Sanofi S.A. |

Get more details on this report - Request Free Sample

The key driver in the growth of the multiple myeloma therapeutics market is the radical shift in the approach of breakthrough immunotherapies to earlier treatment lines, radically changing the treatment paradigm and dramatically broadening the patient population available to treatment. The revolutionary introduction of BCMA-targeted CAR-T cell therapies with unprecedented response rates of 73-98% in highly pre-treated patient groups who had exhausted standard treatment options was the FDA approvals of idecabtagene vicleucel (ide-cel) in March 2021 and ciltacabtagene autoleucel (cilta-cel) in February 2022

The clinical effect has been groundbreaking with these engineered cellular therapies reprogramming the own T-lymphocytes of patients to acknowledge and erase malignant plasma cells that express B-cell maturation antigen, and yield long-term remissions in populations where past results were 4-6 months with salvage chemotherapy. Recent advances in the use of ide-cel as a second-line therapy in patients who have undergone at least two therapies mark a paradigm shift toward the earlier application of cellular immunotherapy as a treatment, potentially expanding the population of patients that can be addressed by at least 12,000-15,000 patients/year in the United States alone.

Simultaneously, bispecific T-cell engager antibodies, such as teclistamab, elranatamab, and talquetamab have shown impressive efficacy in the relapsed/refractory setting with an overall response rate of 63-74% and the crucial benefit of off-the-shelf usage without tailored manufacturing necessities that restrict CAR-T accessibility. These agents offer direct access to powerful immunotherapy without the 4–6-week manufacturing cycle to produce autologous CAR-T, which allows prompt treatment to start in community oncology where CAR-T administration infrastructure can be scarce.

Key Performance Metrics:

The use of CAR-T cells therapy in multiple myeloma grew by 247% in 2023-2025, and there were about 4,800 patients with CAR-T cell therapy in the United States in 2025 compared to 1,400 in 2023. The world has increased its number of licensed CAR-T treatment centers, reaching 87 in 2022 and 312 in 28 nations by December 2025, enhancing geographic coverage and decreasing patient travel load. Increases in manufacturing efficiency led to a decrease in the average time between apheresis and CAR-T infusion by 6.2 weeks in 2022 versus 3.8 weeks in 2025, and prevented excessive disease progression during manufacturing periods. In 2025, there was a 418% year-over-year increase in prescriptions of bispecific antibodies, with around 8,700 patients starting therapy worldwide, which was propelled by the convenience of subcutaneous administration and immediate access to the product, without delays associated with manufacturing.

The greatest barrier limiting the expansion of multiple myeloma therapeutics market is the unprecedented increase of treatment expenses that jeopardizes the sustainability of healthcare systems and introduces a significant access gap between socioeconomic groups as well as geographical areas. Cellular immunotherapies have significantly raised the cost per patient of treatment, with CAR-T cell therapies priced at USD 475,000-515,000 per infusion, monoclonal antibody regimens priced at USD 180,000-240,000/year and a combination regimen of multiple drugs priced at USD 300.

The monetary cost is more than the direct drug acquisition cost by covering both high ancillary cost, such as hospitalization of CAR-T administration and management of cytokine release syndrome, averaging USD 85,000-120,000 per episode, and regular imaging studies and lab monitoring, costing USD 35,000-50,000 a year, and treatment-related complicit The average out-of-pocket costs to patients are USD 12,000-18,000/year regardless of whether they have insurance or not, and 42% of patients with multiple myeloma report experiencing high financial distress and 28% report non-adherence to treatment because of financial issues, according to surveys conducted by patient advocacy organizations.

The economic problem is further exacerbated by the chronicity of the multiple myeloma disease path that necessitates sequential lines of therapy during the course of disease, and patients are generally given 3-5 varying treatment options over their lives. The hard choices of resource allocation that healthcare systems have to make are due to the fact that new therapies are taking up a larger share of oncology budgets, and multiple myeloma therapeutics are consuming 8-12% of the total oncology drug spending in developed markets, yet represent 1-2% of the cancer patients.

Challenge Performance Metrics:

The rate of insurance prior authorization denial of novel multiple myeloma therapies rose by 18% in 2022 to 27% in 2025, with an average of 28-42 days to resolve the appeal causing a treatment delay and risk of disease progression. In the United States, it is estimated that about 34% of eligible patients fail to start CAR-T therapy when recommended by their physician, and in 58% of cases, financial considerations were cited as the most important barrier to CAR-T, according to surveys of academic medical Centers. The capacity limitations in the manufacturing of CAR-T therapies led to an average waiting time of 3.5 months during peak demand times in 2025, and 22% of patients who could have treatment in the European Union countries were not able to do so because of restrictions on reimbursement and center qualification.

Combining ultrasensitive minimal residual disease detection technologies and next-generation immunotherapy platforms opens groundbreaking opportunities to optimize personalized treatment that could largely enhance patient outcomes and overcome cost-effectiveness issues. State-of-the-art MRD detection systems based on next-generation sequencing and multiparameter flow cytometry can detect a single malignant plasma cell in 1 million normal cells, and can accurately measure the depth of treatment response with a substantial number of clinical studies showing that MRD negativity is associated with better progression-free and overall survival across all disease stages.

This accuracy diagnostic approach allows risk-based treatment plans in which the intensity and duration of therapy are adjusted according to response kinetics, not based on standard guidelines, which may permit de-escalation of therapy in patients that develop deep molecular remissions and increase therapy in those with persistent MRD positivity. The resulting paradigm shift to MRD-guided management opens up the market to significant opportunities to pharmaceutical companies to form companion diagnostic alliances, design adaptive clinical trials with MRD-based endpoints that may accelerate the regulatory approval cycles, and create differentiation by deeper response metrics.

At the same time, the creation of new targets other than BCMA will prove the urgent unmet demand of patients developing resistance to existing immunotherapies. New targets such as GPRC5D, FcRH5, and SLAMF7 have potential sequential therapy options and combination therapies that can potentially avoid antigen escape strategies. The next frontier in curative-intent strategy is the development of bispecific antibodies and CAR-T therapies that combinatorically target multiple antigens and early clinical data has indicated that these therapies are better in terms of durability of response than single-target therapies.

Opportunity Metrics:

The multiple myeloma MRD testing market is expected to reach USD 890 million by 2030 with a CAGR of 18.4% and pharmaceutical companies are progressively considering MRD endpoints in clinical development strategies to hasten regulatory routes. By 2025, routine MRD monitoring in academic medical centers is present in approximately 67% of medical centers and in 42% of community oncology practices; Medicare and commercial payers are expanding reimbursement coverage of prognostic testing. In 2025, the non-BCMA targeted immunotherapy pipeline consisted of 47 clinical-stage agents, with the market size expected to increase by 14.2% CAGR through 2034 as resistance to BCMA-targeted therapies is expected to rise. Phase 1/2 Dual-target CAR-T therapies have already shown preliminary response rates of 68-78% in BCMA-refractory populations, indicating that they may overcome single-antigen resistance mechanisms.

One of the emerging trends that have transformed the multiple myeloma therapeutics paradigm is the standardization of quadruplet induction regimens as the new standard of care therapy alongside the emergence of next-generation oral agents, which provide convenient outpatient exposure with therapeutic effects equal to intravenous regimens. The historical progression of doublet combinations to triplet and recently quadruplet regimens with the addition of anti-CD38 monoclonal antibodies can be considered a logical escalation of the initial therapy with an overwhelming effect on depth and durability of response.

Landmark trial clinical data such as PERSEUS and GMMG-HD7 have proven daratumumab-containing quadruplet regimens as new standard of care in transplant-eligible patients, whereby progression-free survival and minimal rates of residual disease negativity have been superior when compared to conventional triplet combinations. This standardization generates unremitting pressure on high-priced biologics in the first-line scenario and sets up treatment paradigms that prefer to focus on continuous therapy patterns that persist into several years.

At the same time, the creation of oral small molecule agents that could target key disease pathways provides the chance to enhance the quality of life and decrease the health care system load associated with the use of the infusion centers. The next generation oral proteasome inhibitor, new immunomodulatory therapy, and new targeted protein degraders with the use of PROTAC technology to selectively degrade BCMA and other myeloma-essential proteins are the next step in convenient home-based treatment regimens that do not compromise therapeutic efficacy.

Trend Performance Metrics:

The adoption of quadruplet regimens has gone up in 2023 (40% of newly diagnosed patients with transplant-eligible conditions) to 2025 (65% of interventions) in major US cancer centers due to the new NCCN recommendations that reflect the new clinical trial results. Patient preference surveys indicate 78-84% preference of oral therapy over intravenous delivery of identical efficacy and safety profiles, with quality-of-life measures showing marked increases in treatment satisfaction scores. Economic evaluations of healthcare indicate that oral therapy regimens result in a decrease of USD 18,000-28,000 per patient/year in the overall cost of care by avoiding visits to infusion centers, a decrease in monitoring, and lessening supportive care. The late-stage development of novel oral CELMoDs has the potential to capture the USD 4.2 billion USD-refractive lenalidomide market, with estimated highest sales potential of USD 1.8-2.4 billion in the event they are approved across multiple diseases.

North America controls and dominates the biggest market value of USD 13,423.7 million in 2025, 50.0% of the global market value and its CAGR is projected to be 9.3% through 2034. The market dominance in the region is indicative of the convergence of the largest per-capita healthcare spending in the world, developed oncology facilities including myeloma specific treatment centers, broad insurance coverage of novel treatments, and concentration of pharmaceutical innovation with most of the new treatment receiving first regulatory approval in the United States.

In the North American market, United States represents the 89% of the market worth USD 11,947.1 million, with Medicare coverage of about 62% of the multiple myeloma patients with median age at diagnosis of 69 years and full reimbursement of innovative therapies such as CAR-T cell immunotherapies. The nation boasts the highest globally adoption rates of breakthrough therapies of 73% of newly diagnosed patients using daratumumab-based regimens by 2025 versus 45% worldwide, and 28 per 100,000 patients using CAR-T cell therapies versus 12 per 100,000 in Europe.

Evidence-based treatment recommendations presented in the National Comprehensive Cancer Network guidelines are highly influential to clinical practice patterns and payer coverage decisions, and include 47 different treatment regimens at different disease stages currently. These recommendations focus on treatment methods and maintenance treatment methods which are capable of prolonging treatment and enhancing survival results, which further contributes to the rising revenue of pharmaceutical companies.

Europe had USD 8,054.2 million market value in 2025 with 30.0% of the world market share and an estimated 8.7% CAGR to 2034. The area is marked by advanced regulatory systems via the European Medicines Agency, the full procedure of health technology assessment that focuses on cost-effectiveness, and the unequal national healthcare systems that produce different patterns of access across the member states.

Germany is the biggest national market with USD 2,013.6 million in 2025 as it enjoys the statutory health insurance system that offers universal coverage and fairly quick post-approval entry to novel therapies. The added therapeutic benefit in the AMNOG health technology assessment process in the country necessitates pharmaceutical companies to prove a added therapeutic benefit, and 67% of novel multiple myeloma therapies received either considerably added therapeutic benefit or major added therapeutic benefit designations during the 2020-2025 period, enabling them to support premium pricing and wide reimbursement.

The United Kingdom has more restrictive patterns of access, and NICE demands cost-effectiveness ratios less than £30,000-50,000 per quality-adjusted life year to routinely commission. In 2022, car-T cell therapies were conditionally approved via the Cancer Drugs Fund mechanism that allows patients access to the treatment as more real-world evidence is produced to finalize reimbursement decisions.

Asia Pacific was the fastest rising region with a predicted CAGR of 11.2% up to 2034 with a projected USD 4,299.5 million in the year 2025 with a global market share of 16.0%. The increased pace of development in the region is indicative of escalating disease rates related to the aging of the population and the development of improved healthcare infrastructures and insurance programs, growing wealth that can afford high-cost treatments, and regulatory harmonization to provide more rapid novel therapy approvals.

China will be 48% of the regional market value of USD 2,063.8 million in 2025, and the National Medical Products Administration introduced regulatory reforms that decreased the average drug approval times of 36-48 months in the past to 12-18 months presently. National Reimbursement Drug List negotiations in the country have also been successful in lowering the cost of multiple myeloma therapies by 60-75% in favor of volume commitments, with the use of lenalidomide use surging 340% in 2020-2025 after price cuts.

Japan has the highest incidence of multiple myeloma per-capita in Asia at 6.2 per 100,000 population, and has the most advanced healthcare infrastructure and national health insurance, which means that new treatments are quickly available. Only 14 months after US approval, the country approved daratumumab, and CAR-T cell therapies were approved in 2023 and the manufacturing capacity is set to grow to treat 800-1,000 patients per year by 2027.

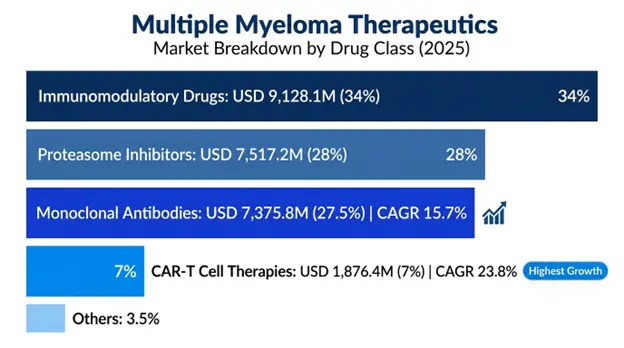

Immunomodulatory Drugs have the majority market share (34% of total revenue in USD 9,128.1 million in 2025) and includes lenalidomide, pomalidomide and next-generation CELMoD drugs that regulate immune system activities to bolster anti-tumor responses and directly suppress the growth of myeloma cells. Lenalidomide is the backbone medication involved in about 70% of new diagnosis and 85% of control treatment regimens but generic competition that begins in 2025 is expected to lower the originator prices by 70-85% during the forecast period.

The Monoclonal Antibodies have the highest growth rate of 15.7% CAGR until 2034 with a valuation of USD 7,375.8 million in 2025. This category includes CD38-targeted antibodies daratumumab and isatuximab, SLAMF7-targeted elotuzumab and emerging bispecific T-cell engagers. Daratumumab is the most used agent that is used in 73% of patients who are newly diagnosed in the United States as of 2025 due to clinical trial data that shows a significant increase in progression-free survival with the use of this agent in addition to standard backbone regimens.

CAR-T Cell Therapies are the most rapidly growing segment that grew off a smaller base with a market value of USD 1,876.4 million in 2025 and a CAGR of 23.8% through 2034. This group includes BCMA-targeted autologous cellular therapies ide-cel and cilta-cel, and is set to expand to second-line indications, significantly expanding the number of addressable patients per year to more than 25,000 patients in the United States.

Proteasome Inhibitors retain 28% of the market share of USD 7,517.2 million in 2025, comprising of bortezomib, carfilzomib and ixazomib which interfere with the cellular protein degradation mechanisms that are vital to the survival of myeloma cells. Competition by generic bortezomib since 2022 has brought down prices whilst clinical use remains the same, with next generation agents’ carfilzomib and ixazomib priced as premium due to their better safety profiles and convenience of oral intake.

First-Line Treatment controls the market value at 52% at USD 13,960.6 million in 2025 with initial therapy to newly diagnosed patients with the highest number of patients and the longest treatment period. Combination regimens (quadruplet combination regimens) involve the use of daratumumab in combination with backbone therapies, which are then followed by long-term maintenance regimens with a median time to progression of 48-62 months in modern regimens.

Second-Line Treatment has market share of 31% in USD 8,322.7 million in 2025 and the highest growth rate of 12.4% CAGR through 2034, due to increased treatment options such as CAR-T cell therapies approved to be used earlier, bispecific antibodies and new drug combinations. This segment is the major arena of new therapy approvals and competitive differentiation.

Third-Line & Beyond is 17% market share at USD 4,564.0 million in 2025, which comprises highly pre-treated relapsed/refractory populations with a poor history of outcomes. The introduction of CAR-T cell therapies and bispecific antibodies have revolutionized this segment with response rates of 63-98 and median progression-free survival of 12-24 months and highest per-patient cost of treatment.

The multiple myeloma therapeutics market is a highly competitive ecosystem with the five major companies dominating about 68-74% of the global market share due to diversified product portfolio comprising of various drug classes, long clinical development pipelines and positioning across all lines of therapy. Competitive differentiation focuses on the development of new mechanism of action, clinical trial design with better efficacy, combination regimen approaches, and real-world evidence to support incorporation of guidelines and payer reimbursement.

Johnson and Johnson has been able to maintain market leadership through its entire myeloma franchise which comprises of Darzalex (daratumumab), Carvykti (ciltacabtagene autoleucel) and Tecvayli (teclistamab) which has allowed it to develop proprietary combination regimen and sequential therapy programs. Bristol Myers Squibb has a good standing with Abecma (idecabtagene vicleucel) CAR-T therapy, Revlimid (lenalidomide), and Empliciti (elotuzumab), and it is strategically positioned to grow its cellular immunotherapy platform.

The areas of innovation focus are next-generation immunotherapies with better safety profiles and manufacturing efficiencies, oral small molecule agents with convenient administration, biomarker-driven patient selection strategies, and minimal residual disease-adapted treatment. Firms are implementing vertical integration plans that include manufacturing, diagnostic alliances, and platforms of real-life evidence to facilitate value-based care.

March 2026: Johnson & Johnson gained FDA endorsement of expanded indication of Carvykti (ciltacabtagene autoleucel) in patients receiving 1 prior line of therapy, as clinical data revealed a 60% decrease in progression threat in comparison to typical care, with the ability to expand the number of patients to be addressed by 15,000 patients/year in the United States.

February 2026 Bristol Myers Squibb reported positive Phase 3 results of Abecma (idecabtagene vicleucel) in earlier-line relapsed/refractory patients, showing it to have an improvement in progression-free survival over standard regimens and providing a regulatory submission pathway to expand Abecma indication into the second-line.

January 2026: Takeda Pharmaceutical finished USD 240 million expansion of CAR-T manufacturing plant in Houston, Texas, which increased annual production capacity to 12,000 patient doses up to 4,500, and shortened manufacturing times to 2-3 weeks instead of 4-5 weeks, addressing supply issues that limited commercial adoption.

December 2025: Amgen Inc. reported positive Phase 3 results showing addition of carfilzomib to daratumumab-dexamethasone led to an increase in median progressionfree survival of 28.6 months to 45.8 months in relapsed/refractory patients, with new triplet combination established as a new standard care.

November 2025: Sanofi S.A. commenced Phase 3 trial of isatuximab in combination with novel oral CELMoD agent iberdomide versus standard regimens in newly diagnosed ineligible patients (transplant) and planned to enroll 1200 patients across 28 countries with primary completion expected in 2029.

List of Key Players in Global Multiple Myeloma Therapeutics Market

Global Multiple Myeloma Therapeutics Market Segments

By Drug Class:

By Line of Therapy:

By Route of Administration:

By Treatment Setting:

By Distribution Channel:

By End User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

26 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.