Share this link via:

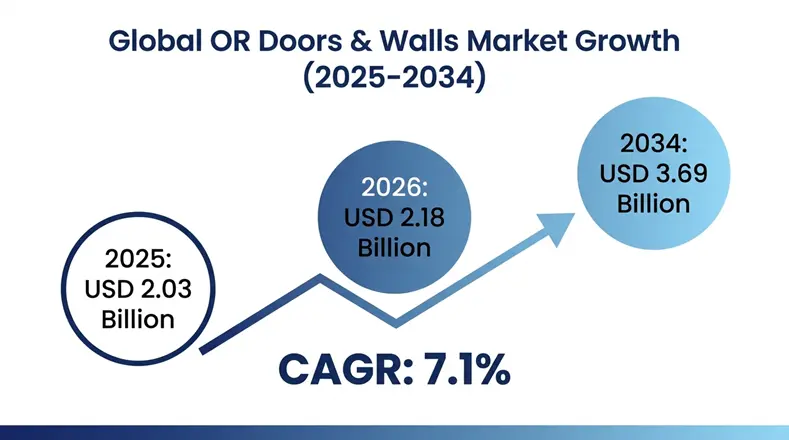

The market size of the global operating room doors and walls is estimated to be USD 2.03 billion in 2025 and in 2026, it is expected to be USD 2.18 billion and reach USD 3.69 billion by the year 2034 with a CAGR of 7.1% over the forecast period (2026-2034).

The operating room doors and walls are vital infrastructure elements that constitute the physical envelope of the surgical setting, which is a complex of protective barriers that keep the environment sterile, regulate the airflow, avoid cross-contamination, offer radiation protection, acoustic insulation, and integrate the most advanced medical devices and digital technologies. Such specialized architectural features are required to meet high regulatory standards such as Joint Commission International standards, Centers for Disease Control and Prevention infection control guidelines, American Society of Heating Refrigerating and Air-Conditioning Engineers ventilation guidelines and Facility Guidelines Institute construction guidelines, which regulate the design and operation of modern healthcare facilities.

The market has changed beyond mere architectural barriers to engineered systems with hermetic sealing technologies to maintain a precise pressure differential, antimicrobial surface treatment technologies utilizing silver ion and copper alloy technologies, electromagnetic interference shielding to protect sensitive medical electronics, and modular construction methods allowing quick installation with little disturbance to current hospital operations. Contemporary operating rooms operate in technology-rich ecosystems whereby doors and walls need to support ceiling-mounted surgical robots, intraoperative imaging systems, advanced environmental control systems, and extensive digital infrastructure to support telemedicine potential and surgical education broadcasting.

The changes are associated with changing surgical practice such as the spread of minimally invasive surgery with the need to integrate advanced imaging, the development of hybrid ORs with surgeries and interventional radiology, the growing use of robotic surgery, and the growth of infection prevention consciousness due to healthcare-associated infection reduction efforts and regulatory actions. The modern operating room is becoming a more and more integrated system, where architecture elements are expected to integrate smoothly with medical equipment, building automation and hospital information networks, and remain the most sterile, safe, and efficient operations.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 2.03 Billion |

| Forecast Value | USD 3.69 Billion |

| CAGR | 7.1% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, By Door Type, By Wall System Type, By Material, By Application, By End-User |

| Region Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Spain, Italy, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | ASSA ABLOY AB, Dortek Ltd., STANLEY Healthcare, Getinge AB, Lindner Group, Manusa, TANÉ HERMETIC, Kingspan Group, Metaflex Doors, Steris PLC |

Get more details on this report - Request Free Sample

The market in which the operating room doors and walls market competes is a part of the larger healthcare infrastructure ecosystem, which includes specialized manufacturers, architectural engineering firms, healthcare construction contractors, infection control consultants, and facility management organizations. Market dynamics indicate the convergence of worldwide hospital construction endeavor, modernization of the aging surgical units, adoption of high standards of infection control, technological advancement in the materials science and automation systems and the use of modular construction procedure that provides quicker completion of the project and less operational disruption on the project during installation phases.

The main factor that triggers the market growth is the introduction of more stringent infection control policies and healthcare-associated infection prevention policies in all healthcare systems worldwide that generate unprecedented demand on special doors and walls that actively keep the sterile environment and help prevent the spread of pathogens. In the United States alone, healthcare-associated infections impact about 1.7 million patients each year, and surgical site infections alone contribute to 31% of all healthcare-associated infections among hospitalized patients, generating huge clinical, financial, and legal burdens to healthcare institutions.

Regulatory bodies such as Centers of Disease Control and Prevention, Joint Commission International, and European Centre of Disease Prevention and Control have developed detailed guidelines that mandate healthcare facilities to provide environmental controls that can prove to reduce the risk of microbial transmission and includes require hermetically sealed doors providing positive pressure differentials, smooth wall surfaces that avoid microbial sites of harboring, and antimicrobial materials that sustainably suppress the These needs have changed the cost-optimization strategies of operating room construction to the infection prevention-based specifications that focus on the clinical results and regulatory compliance rather than on the capital expenditure concerns in the long-term.

Healthcare accreditation organizations have further enhanced the regulatory environment, as more and more of these organizations are now including environmental infection control assessments as part of the facility certification process, non-compliance with which may lead to the loss of accreditation, reimbursement fines, and legal liability. Medicare and other large payers have introduced value-based purchasing initiatives that involve a monetary penalty on the hospitals with an above-average infection rates and a monetary reward to the hospitals that can prove their better infection prevention performance, which leads to a direct monetary incentive to invest in infrastructure that the maintenance of the sterile environment.

Key Performance Metrics:

Healthcare facilities that have adopted the use of holistic environmental infection control protocols such as hermetically sealed doors, antimicrobial wall surfaces and optimized ventilation systems record a reduction of 32-47% in the rates of surgical site infections over conventional construction methods, which will translate to estimated savings of USD 2.1-3.8 million per year due to reduced readmission rates, reduced length of stay, and reduced exposure The Centers for Medicare and Medicaid Services Hospital-Acquired Conditions Reduction Program imposed penalties on 764 hospitals in fiscal year 2025, USD 367 million worth of payment penalties and the 25% best-performing hospitals in infection prevention earned bonus payments averaging USD 2.4 million, showing clear financial incentives in infection control infrastructure investment.

The volume of surgical procedures across the globe is growing by 6.8% every year between 2022-2025 to around 421 million procedures, and every additional operating room will need USD 285,000-420,000 in specialty doors and walls, which provide modern infection control standards, creating a significant growth in the addressable market as healthcare systems worldwide invest in surgical capacity growth

The greatest obstacle that hinders market penetration deals with the high capital outlay requirements and the lengthy project implementation schedules of operating room construction and renovation projects, especially in integrating sophisticated hermetic sealing systems, antimicrobial surface finishes, and modular wall systems that incur high prices compared to the traditional building methods. Automatic doors with built-in environmental monitoring and access control systems that are hermetically sealed cost USD 15,000-35,000 per unit, versus USD 3,500-7,500 per unit on ordinary hospital doors, modular wall systems with antimicrobial surfaces and built-in utilities cost USD 1,850-2,650 per square meter, versus USD

The economic issue is heightened by the long project life cycle requiring up to 18-36 months between the initial planning and final commissioning involving the architectural design, regulatory approvals process, competitive procurement processes, construction processes, and overall performance verification testing before surgical operations can start. The long timelines not only pose a problem of cash flow to the healthcare systems but also pose a risk of specification obsolescence as technology and regulatory requirements keep changing during the various development stages of the project.

Healthcare systems with limited capital budgets have to make decisions on investments between competing priorities such as medical equipment modernization, information technology infrastructure, staff growth and facility repair with specialized doors and walls being viewed as non-revenue generating infrastructure investment but with very important infection prevention and regulatory compliance purposes. The situation is especially true in emerging markets, where public hospitals and healthcare systems have specific challenges that make it worthwhile to invest in premium infrastructure in order to support the provision of basic healthcare access and capacity issues by serving more and more patients at large.

Financial Impact Metrics:

Construction projects involving use of premium operating room doors and walls have average cost increase of 22-34% over the normal construction methods with specialized components comprising 8-12% of the total operating room construction costs averaging USD 2.8-4.2 million per fully equipped surgical suite. Financing issues in projects lead to one in four intended operating room building projects being postponed or reduced in emerging markets as well as one in five projects in developed markets having scope reductions affecting the door and wall specification in the project to help control costs.

Complexity of installation needs specialized labor with certification in healthcare building, hermetic sealing system and infection control plans, which generates labor shortages that add 18-25% to the construction cost of the installation and adds 6-9 weeks to the project schedule in markets with short supplies of specialized contractors. All these are obstacles to adoption, especially in price sensitive markets where the initial capital cost is given more weight than the long-term operational benefits and infection prevention value propositions.

There is a market opportunity in creating and commercializing fully integrated modular prefabricated operating room systems that comprise of doors, walls, ceiling systems, environmental controls and technology infrastructure in factory manufactured modules that can be quickly assembled and commissioned on site. These solutions solve key pain points in the market such as long construction times, inconsistencies in quality control, workforce skills, and on-site operational interruptions to operational hospitals, and also have potential cost savings of 15-25 by manufacturing efficiency, less on-site labor, and shorter installation times to yield faster payback.

The modular construction methodologies allow healthcare systems to quickly increase theoretical capacity in a surgical department in response to demand changes, natural disaster response, pandemic preparedness needs and military field hospital deployments, with full operating room modules able to be installed and commissioned within 4-8 weeks instead of the 12-18 months of a conventional construction. The strategy also facilitates the standardization of different healthcare networks, which allows economies of scale in the buying process, easier maintenance procedures, and uniformity of performance levels in various facilities.

The realization of smart technology features also opens up further value creation potentials such as doors and walls with IoT sensor networks to check the surrounding conditions, automated access control systems, integrated display surfaces, and predictive maintenance functions to maximize performance at minimal operating expenses. Such intelligent systems may be connected with hospital information systems, building automation systems, and infection control monitoring systems to deliver real-time environmental data, automated records to meet regulatory requirements, and predictive analytics to meet proactive facility management.

Opportunity Metrics:

In 2025, the global modular healthcare construction sector topped USD 12.4 billion, with the operating room modules accounting about 14% of the market, at USD 1.74 billion, with a growth rate of 11.8% CAGR as compared to 7.1% under the conventional construction method. Early adopters have testified 32-45% savings in total cost of project and 65-78% savings in installation schedules with modular systems and have achieved the same or better results in terms of infection control measures and regulatory compliance mandates.

The integration of smart building technology in healthcare buildings is expected to grow USD 8.9 billion by 2030, with operating room applications being a high-value market where the technology premiums can be recovered through infection control advantages, operational efficiency enhancements, and automation of regulatory compliance. Smart operating room technologies have been shown to produce an average 18-24% energy cost savings through improved environmental control systems in healthcare systems, and have been reported to lower equipment downtime by 28-35% average over reactive maintenance methods.

A combination of the advanced materials science with the automation technologies is fundamentally changing the operating room doors and walls as passive architectural components and making them active infection prevention systems that constantly suppress the viability of pathogens and allow the use of touchless operation to eliminate the risk of contamination. The materials of next-generation antimicrobial include copper alloys, silver nanoparticles, photocatalytic titanium dioxide overcoats, and technologies that show persistent antimicrobial activity over product lifecycles, where third-party testing has shown 99.9% pathogen reduction of healthcare-associated pathogens such as MRSA, E. coli and Clostridioides

Touchless automation systems have gone beyond the basic motion sensors to incorporate advanced systems such as radar-based presence detection, biometric access control, voice recognition and integration with hospital staff badge systems that result in fully hands-free functionality without compromising the security and access control measures. These systems have become especially prominent due to the COVID-19 pandemic and are still growing, as healthcare systems realize their usefulness in routine infection prevention and efficiency in operations.

The trend moves to smart glass technologies to allow walls to become transparent and opaque to allow teaching and observation, integrated display surfaces, which remove the need to have separate monitors, but still be sterile, and adaptive environmental control systems, which automatically change lighting, temperature and ventilation based on the type of procedure and occupancy.

Trend Performance Metrics:

Advanced antimicrobial surface technologies applied to healthcare facilities indicate a 28-41% decrease in the level of surface contamination relative to conventional materials and remain effective over 5-7 years of testing despite the intense cleaning regimens with strong disinfectants. There was a 156% increase in the adoption rate of touchless door systems over 2020-2025 with 67% of new construction projects of operating rooms specifying automated hands-free operation instead of 23% in 2019.

Smart glass wall systems incur 180-240% higher prices than traditional glass installations but provide value due to their expanded functionality, with academic medical centers reporting a 34% increase in the effectiveness of surgical education and a 22% decrease in the number of disruptions caused by observing procedures with switchable transparency technologies. The average operational efficiency improvement of 15-21% in healthcare systems that adopt full-fledged smart operating room technologies is due to decreased turnover time, increased resource utilization, and improved workflow coordination possibilities.

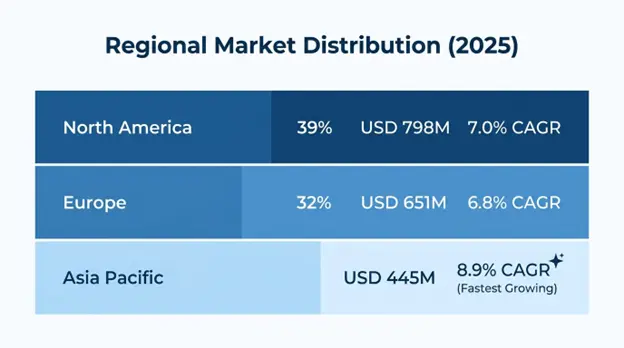

The North America market leadership stood at USD 798 million in 2025 with 39% market share globally with a projected growth of 7.0% CAGR up to 2034. The regional dominance is an indication of the largest concentration of high-level surgical facilities in the world, full regulatory systems that set high environmental control standards, large investment in healthcare infrastructure in the face of a mature market, first to adopt hybrid operating rooms and robotic surgical systems and established ties between major manufacturers and major healthcare systems, group purchasing organizations and specialized healthcare construction companies.

Key Performance Indicators:

In 2025, the healthcare system of the United States had about 52,400 operating rooms, 4,200 new ones installed, and 8,700 major renovations that required specialized doors and walls worth USD 642 million annually. Mean investment per room in doors and walls was USD 325,000-485,000 in premium installations, such as hermetic sealing, antimicrobial surfaces, radiation shielding in hybrid ORs, and capabilities of a smart building integration. The regulating environment is well established, and the Joint Commission International standards and the CMS quality reporting measures have created constant demand to invest in compliance-related infrastructure.

Hybrid construction of ORs was 18% of new OR construction in 2025, compared to 8% in 2020, and such special designs need a wall system able to support heavier equipment loads of 3,500-8,500 kilograms and lead-lined radiation protection that increases the cost of construction by USD 280-450 per square meter. The renovation and modernization component comprises 67% of market value, as healthcare systems adapt aging facilities that had been constructed during the 1980s-1990s boom of hospital construction to current needs of infection control and integration of technology.

Europe was USD 651 million market value in 2025 covering 32% of the global share with a forecasted 6.8% CAGR by 2034. The regional market is defined by the high environmental sustainability regulations, detailed infection prevention, focus on renovation and modernization instead of new construction, and the high interest in modular construction methods, which cause minimal disturbance to the operation at the stage of installation.

Regional Market:

In 2025 Germany has USD 189 million as it has invested heavily in the hospital modernization efforts to address the aging infrastructure, and 67% of German hospitals with a facility over 30 years old require a full renovation. The market is geared towards sustainability; 78 of the new projects under construction are LEED Gold or comparable European standards by expressing the use of recyclable materials, energy efficient thermal construction and low emission manufacturing.

The UK can be considered a high-growth state, although the budget of the National Health Service is limited, and infection prevention facilities are fully funded as the first priority after the high-profile cases of healthcare-associated infections. Copper alloy antimicrobial surfaces are starting to become a standard specification in UK facilities, with 58% of surface contamination reduction being demonstrated to warrant 25-35% of price over standard materials. Nordic countries are the European leaders in the adoption of smart building technologies, with 45% of new operating room projects being built with IoT-enabled environmental monitoring and automated control systems.

Asia Pacific became the fastest-growing region with a projected CAGR of 8.9% up to 2034 to USD 445 million in 2025 compared to USD 267 million in 2022. Growth rate increase indicates unprecedented growth in the healthcare infrastructure, government program on building hospitals to counter the gap in surgical capacity, increasing middle-class populations using high-quality healthcare services, growth of medical tourism sector, and regulatory maturity to establish standards of infection control almost at the international level.

Regional Growth Drivers:

China has experienced an 89% increase in its market, USD 198 million in 2025, and national healthcare infrastructure growth of 1,450 new hospitals (average of 12 operating rooms per hospital), and widespread modernization of existing surgical facilities to meet new standard requirements of infection control. The USD 47 billion allocated by the government to the infrastructure in the healthcare sector in the course of the 14th Five-Year Plan generated a long-standing demand on the international-standard doors and walls systems.

The same period in India displayed a growth of 108% which was driven by an ever-increasing number of private hospitals and government health insurance plans that contributed to initiating the construction of surgical hospitals. India is increasing its number of new operating rooms by about 3,200/year in 2024-2025, and high-end facilities are now starting to specify hermetically sealed doors and antimicrobial wall systems to attract medical tourism and wealthy domestic clients. The overall growth of 78% of Southeast Asian markets including Indonesia, Vietnam, and Thailand in 2022-2025 is a sign of economic development activities and healthcare system modernization.

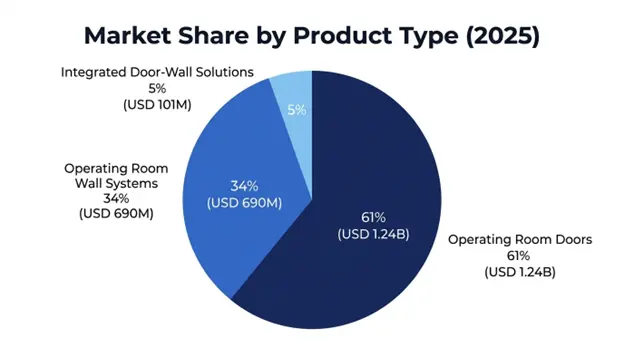

Operating Room Doors holds the largest market share of USD 1.24 billion, 61% in 2025, including hermetically sealed sliding doors, automatic swing doors, radiation-protective doors and manual doors used in various applications, including main surgical suite access, equipment transfers and emergency exit. The segment has replacement cycles of 12-15 years on mechanical parts and 20-25 years on door panels, which generates a consistent aftermarket demand to offset new construction activity. Premium hermetically sealed automatic doors contain 42% of segment value of 26% of unit volume, average selling prices of USD 18,000-32,000 versus USD 4,500-8,500 of standard hospital doors.

Operating Room Wall Systems will have a 34% market share of USD 690 million in 2025 comprising modular panel systems, fixed wall construction, cleanroom grade panels, and lead-lined radiation shielding walls serving hybrid operating rooms and interventional suites. It has the largest growth potential with the 8.4% CAGR through 2034 attributed to the rising use of modular construction, the expansion of hybrid ORs, and the trend to specify the antimicrobial surfaces with more complex materials science such as copper alloys and photocatalytic surfaces.

Integrated Door-Wall Solutions are 5% market share with USD 101 million in 2025 but has the highest growth rate with 12.1% projected CAGR, include fully prefabricated systems where doors, walls and environmental controls are designed as a unit. These high-end solutions are highly priced with an average USD 2,150-2,950 price premiums over the conventional construction of USD 1,050-1,650 with the advantage of shorter installation time, better quality, and environmental performance.

Topped by Hermetically Sealed Sliding Doors with 46% door segment share of USD 571 million in 2025, are the advanced systems with inflatable gasket seals, precise closing mechanism and automated operation that ensures maintenance of stringent pressure differentials and hands-free movement. These high-end doors will also feature customizable sealing pressure, emergency manual mode, inbuilt status displays, and interfaces to building automation system to monitor the environment and record compliance.

Automatic Sliding Doors capture 28% of the door segment share (USD 347 million) in 2025, which includes space-efficient operation, quiet operation and hands-free operation to uphold infection prevention measures. Sensors-activated, push-button, and badge-reader are also part of the segment, where touchless activation will grab 73% of automatic door value in 2025, in contrast to 41% in 2020, indicating a faster adoption rate following hygiene awareness during the pandemic.

Swing Doors have 26% door segment share USD 322 million in 2025, as secondary access, equipment doors and applications with less strict hermetic sealing needs. Swing doors retain their relevance despite the decreasing of the relative market share due to reduced acquisition cost, reduced maintenance and applicability in renovation projects of space or budget limitations.

Stainless Steel has the highest market share of 41% with USD 832 million in 2025 and it provides optimal durability, corrosion resistance, cleanability and inherent antimicrobial properties, especially the 300-series austenitic grades that include copper and silver elements. High-end antimicrobial stainless-steel grades fetch a 35-50% price advantage and exhibit 99.9% reduction in the surface bacterial viability in 2-4 hours according to EPA-registered testing standards.

High-Pressure Laminate has a market share of 22% at USD 447 million in the year 2025 offering cost-effective solutions which have various aesthetics and are compatible to antimicrobial surface treatments. Innovations such as copper infused laminates, photocatalytic surfaces, integrating silver nanoparticles that offer long-term antimicrobial protection during product lifecycles are strengths of the segment.

Tempered Glass will have a market share of 18% at USD 365 million in 2025, with the glass finding favor on non-porous surfaces, resistance to chemicals, and aesthetics that facilitate the modern design of a surgical suite. Back-painted glass systems allow built-in LED lighting and smart glass technologies provide adjustable transparency at a high price to support teaching and observation uses.

Lead-Composite Materials are 11% market share with USD 223 million in 2025 and are used in specialized radiation shielding in hybrid operating rooms and interventional suites. These materials have lead sheets or lead-loaded compounds that deliver desired radiation attenuation and structural integrity and surface durability specifications.

The global operating room doors and walls market is moderately concentrated with the top eight manufacturers holding about 58-64% market share of the global market due to extensive product portfolio, developed distribution channels, technical support, and good brand name among health facility planners and construction professionals. The focus of competitive differentiation is regulatory compliance certifications, technical innovation in sealing systems and antimicrobial technologies, customization opportunities, project management experience, and long-term warranty and service programs, which guarantee performance and customer satisfaction in the long term.

The market structure indicates geographic specialization where European manufacturers have shown dominance in hermetic sealing and modular system, North American manufacturers have shown dominance in smart building integration and automation technologies and emerging Asia Pacific manufacturers are gaining market share by offering competitive prices and also improving the quality standards and regulatory compliance. The market is also still consolidating with strategic acquisitions with building materials conglomerates and healthcare infrastructure experts developing complete operating room solution portfolios, and specialized niche players targeting certain technologies such as radiation shielding, antimicrobial treatments, and modular prefabricated construction.

March 2026: ASSA ABLOY AB announced next-generation SW300 hermetically sealed door system with improved sealing performance that retains 75 Pascal pressure differentials, built-in IoT monitoring network and copper-silver antimicrobial surface treatments, which will be installed in 22 academic medical centers around the world in 2026.

February 2026: Dortek Ltd. finalized a USD 15 million expansion in the United Kingdom, automated production and manufacturing factory, leading to 35% shorter lead times and more accurate manufacturing, with its focus on increasing infrastructure projects in the Middle East and modernization programs in European hospitals.

January 2026: STANLEY Healthcare was granted a Regulatory approval of an integrated access control and environmental monitoring system (integrated hermetic doors with real-time pressure monitoring), automated compliance documentation, and integration of the hospital information system to cover infection prevention measures and regulatory standards.

December 2025: Getinge AB stated that it had strategic alliance with a modular construction leader to create prefabricated operating room modules with built-in door and wall systems, focused on European and Middle East markets with complete solutions that would accommodate 6-8 week installations.

November 2025: Lindner Group announced new advanced antimicrobial wall system with sustained-release silver ion technology throughout panel cores, which had lifecycle antimicrobial efficacy and third-party validation of 99.99% reduction of pathogens in 24 hours of contamination.

List of Key Players in Global Operating Room Doors and Walls Market

Global Operating Room Doors and Walls Market Segments

By Product Type:

By Door Type:

By Wall System Type:

By Material:

By Application:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

26 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.