Share this link via:

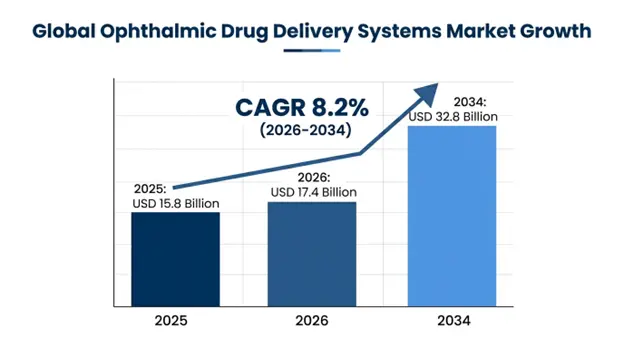

The market size of global ophthalmic drug delivery systems was estimated to USD 15.8 billion in 2025 and was estimated to grow to USD 17.4 billion in 2026 with a CAGR of 8.2 throughout the forecast period (2026-2034).

Ophthalmic drug delivery systems are advanced pharmaceutical technologies that are able to bypass the anatomical and physiological eye-specific obstacles to the delivery of therapeutic agents into specific ocular tissues in the most effective bioavailability, sustained release properties and with the lowest exposure to the body. The eye poses incredible obstacles to drug delivery due to various protective mechanisms such as the tear film that is quick to dilute and drain topical drugs, corneal epithelial barriers to drug entry with less than 5%of topical drugs entering intraocular structures, blood-retinal barriers to systemic drug entry with the posterior segment structures, and clearance mechanisms that turnover therapeutic drug concentrations in target sites.

The modern ophthalmic drugs delivery systems include a wide variety of technological techniques such as improved conventional formulations with viscosity-enhancing agents, mucoadhesive polymers and penetration enhancers that can increase the topical residence time of drugs and enhance permeation through the cornea, through advanced sustained-release methods such as biodegradable

The commercial value goes beyond the sale of pharmaceutical products to include entire therapeutic ecosystems based on drug delivery devices and diagnostic systems, patient surveillance systems, and tailored treatment regimens that maximize the clinical response and minimize treatment burden in terms of lower administration schedules, increased patient compliance, and reduced systemic side effects. The market aims at meeting the unmet needs of various ophthalmic conditions of more than 2.2 billion individuals in the world with impaired vision, 285 million with moderate to severe visual disability that needs continuous pharmacological control to chronic progressive diseases.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 15.8 Billion |

| Forecast Value | USD 32.8 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Technology, Formulation, Disease Indication, Route of Administration, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Novartis AG, Regeneron Pharmaceuticals, Bayer AG, AbbVie Inc., Bausch + Lomb, Alcon Inc., Roche (Genentech) |

Get more details on this report - Request Free Sample

The main structural force that is driving the growth of ophthalmic drug delivery market is the increasing burden of age-related eye diseases, age related macular degeneration of 196 million people worldwide in 2025 and diabetic retinopathy of 103 million people worldwide as the prevalence of diabetes reaches 537 million adults worldwide. These diseases are associated with the top causes of permanent blindness in the working-age and geriatric groups, necessitating long-term pharmacological therapy of anti-vascular endothelial growth factor and corticosteroids and neuroprotective substances to avoid the impairment of vision and support functional autonomy.

The ageing population aged 60 and older exceeded 1.1 billion in 2025 and is expected to rise to 2.1 billion by 2050, resulting in sustained growth in demand as prevalence of age-related eye diseases rises exponentially between 0.2% in 50–59-year-old population to 13.1% in over 80 years old population. Age-related macular degeneration is shown to be most closely correlated with demographic aging, wherein the wet type of the disease is present in 10-15 per cent of cases but causes 90 per cent of severe vision loss, necessitating the regular intravitreal injection of anti-vascular endothelial growth factor agents every 4-8 weeks indefinitely to sustain treatment efficacy.

The prevalence of diabetic retinopathy is like the diabetes epidemic with around 35% of diabetes patients developing any type of diabetic retinopathy, and 7% developing diabetic retinopathy proliferative disease or diabetic macular edema necessitating aggressive pharmacological management. The chronic progressive nature of the conditions requires many years of treatment in many patients, with the average anti-vascular endothelial growth factor therapy treatment duration being over 7 years old and over 120,000 years old in age-related macular degeneration and diabetic macular edema, which generates significant lifetime therapeutic market value of between USD 85,000-120,000 on average per

Key Performance Metrics:

Biodegradable polymer technology, nanotechnology and controlled-release engineering have transformed ophthalmic drug delivery with transformative innovation by achieving sustained therapeutic drug levels with long-lasting administration of single doses with novel long-lasting treatment of chronic ocular diseases that used to require frequent injections or daily applications of topical medications with low patient compliance. The paradigm shift of patients to physician-controlled delivery is a very important aspect because research has repeatedly demonstrated that as many as 50% of patients with glaucoma will not continue to use eye drop therapy after six months because of difficulties in administration, forgetfulness, or local side effects.

Controlled release of drugs of 3-36 months using biodegradable intravitreal implants based on poly (lactic-co-glycolic acid) and other biocompatible polymers, with a careful balance between degradation kinetics and diffusion properties, and without surgical removal, can be achieved by solids engineering. The clinical utility and market acceptance of long-acting delivery systems have been confirmed by the FDA approval and commercial success of sustained-release platforms such as Ozurdex that offer 3-6 months of therapeutic duration, Iluvien that offer continuous therapy up to 36 months, and emerging port delivery systems that offer refillable reservoirs.

Nanotechnology-based delivery systems such as liposomes, nanoparticles, nanomicelles and dendrimers allow increased solubility of poorly water-soluble drugs, shielding of labile drug molecules against enzyme degradation, targeted delivery to a desired cell type by ligand functional groups on the surface of the delivery system, and controlled drug release kinetics to lengthen the therapeutic index. These platforms show specific potential in how they can be used in gene therapy, RNA interference therapy, and protein-based therapy which needs to be shielded against the harsh environment of the eye and has to reach sufficient tissue penetration and cellular absorption.

Innovation Impact Metrics:

Ophthalmic drug delivery market has a lot to gain by solving serious patient adherence problems undermining therapeutic success in various ocular diseases, with non-adherence rates of 33-42% per day of topical glaucoma medications and 19-27% per month of intravitreal injections undermining the success of therapeutic interventions, leading to avoidable vision loss, disease progress Several dosing schedules required in the treatment of ophthalmics, such as multiple topical drugs per day, specific intervals between various drugs to avoid washout, appropriate administration technique that needs hand dexterity and good visualization under typical conditions, and impaired ability to achieve high compliance with therapy are significant obstacles to effective therapy compliance.

The fear factor related to ocular injections also causes bed reluctance to treatment among patients with a large proportion of the patient population who are eligible to receive treatment postponing their treatment because of their anxiety about needle-based procedures. This mental inhibition compels clinicians to weigh between the advantages of aggressive therapy and patient tolerance usually leading into undertreatment and suboptimal results. The direct answer to these challenges is the sustained-release delivery systems, which lower the frequency of administration, which is now daily or multiple daily dosing, to once weekly, monthly, quarterly or even annual interventions.

Clinical trials have shown that changing the frequency of intake of glaucoma medications into once-daily instead of twice-daily intake, and changing the intake of daily topical therapy to quarterly intravitreal injections or annual sustained-release implants increase adherence rates by 18-24 and 35-48 percent, respectively, and directly lead to better disease management and vision retention outcomes. It is not just the administration of drugs but the entire treatment process of attending a clinic regularly, followed up appointments, side effects, and management of these effects that impose significant time and financial burdens of lost work productivity and caregiver burden.

Patient Adherence Challenge Metrics:

The biggest bottleneck restricting the innovation in ophthalmic drug delivery is the incredibly high development cost and complicated regulatory routes of novel delivery technologies, especially combination products incorporating drugs and medical devices that necessitate thorough evaluation of both drug and device aspects by rigorous preclinical studies, elaborate clinical trials, and drug manufacturing procedures. The average time it takes to develop a new ophthalmic drug delivery system is 10-15 years between the first concept and market approval, with the total cost of development of these systems having been USD 800-2.1 billion including failed development and opportunity costs.

FDA regulations of sustained-release intraocular devices stipulate extensive biocompatibility assays, stability assessments in the long-term, dose-response studies on an optimal drug loading and release rate, and long-term clinical trials that demonstrate efficacy and safety during the period of intended treatment, which can be 1-3 years of long-acting implants. The combination products are even more complicated as regulatory authorities consider drug-device interactions, manufacturing reproducibility that guarantees the same drug release profiles with manufacturing lots, and long-term safety of possible complications such as inflammatory reactions to biomaterials.

The high-regulatory-barriers, although necessary in-patient safety, present barriers to market entry and therefore competition, and sustain high prices of approved products, sustained-release ophthalmic implants command USD 15,000-18,500 per treatment versus USD 1,850-2,200 per intravitreal injection, which present reimbursement problems and barriers to access, particularly in price-sensitive markets and for patients with limited insurance coverage.

Development Challenge Metrics:

The most common delivery route, intravitreal injection procedures, which are used to deliver drugs into the anti-vascular endothelial growth factor and corticosteroid categories of anti-vascular endothelial growth factor and corticosteroid, have inherent risks of severe complications such as endophthalmitis with rates of 0.02-0.08/per injection, retinal detachment in 0.01 Although the rates of complications of the procedure at an individual level are low, the risk of the procedure is cumulative over years with a significance level of monthly or bimonthly injections.

Fear of injection procedures is a significant psychological barrier to ideal treatment adherence, with surveys showing that 34-42% of patients are moderately to severely anxious before intravitreal injection, 28%of patients complain of injection pain despite topical anesthesia, and 19%of patients delay or avoid scheduled injections because of fears about the procedure. This mental load is a part of the treatment non-adherence and poor results despite patients being knowledgeable about the need to receive regular therapy to preserve their vision.

The necessity of periodic visits to the clinic to get an injection procedure generates significant resource use in the healthcare system, and the capacity limitations of injection clinics restrict access to patients in most healthcare systems, and introduce delays in terms of scheduling that can hurt the therapeutic outcome in a disease where prompt treatment onset or regular maintenance therapy is required.

There is a transformative opportunity in the market to develop delivery systems that are optimized towards emerging gene therapy and RNA interference therapeutic modalities that could be used as curative or disease-modifying therapies to inherited retinal diseases as well as neovascular age-related macular degeneration and other diseases currently treated by lifelong administration of pharmaceutical drugs. The clinical feasibility of transplanting into the eye was confirmed by the FDA approval of Luxturna to treat RPE65-mediated inherited retinal dystrophy and many programs are underway to treat additional genetic forms of retinal degeneration, Leber congenital amaurosis, and choroideremia that affect about 350,000 individuals worldwide with inherited retinal diseases that can be treated by gene therapy, offering the potential for long-term restoration of vision or slowing of disease progression through a single or limited number of treatments, thereby reducing or eliminating the need for chronic, lifelong pharmaceutical interventions.

Gene therapy vectors such as adeno-associated viruses necessitate special delivery methods that yield sufficient transduction of target cells in the retina and reduce inflammatory reactions and toxicities associated with the vectors. The emergence of streamlined surgery, purification of vectors and regimen to suppress immune reaction against transduced cells are the significant market potential of companies that produce complete gene therapy delivery systems other than the therapeutic vector itself. The possibility of curative treatments that are administered and sold at a premium price of USD 425,000-850,000 per eye generates a huge market value even with a comparatively low number of patients.

RNA interference therapeutics such as small interfering RNA and antisense oligonucleotides, have a need to be delivered by systems that prevent enzymatic degradation of these labile molecules, but allow them to be internalized by cells and escape endosome barriers to therapeutic function. Nanotechnology based systems such as lipid nanoparticles, polymer-based carriers, and cell-penetrating peptides show promise in preclinical studies with a few programs undergoing clinical progression towards geographic atrophy, neovascular age-related macular degeneration and diabetic macular edema.

Gene and RNA Therapy Opportunity Metrics:

The biggest opportunity is to resolve the issue of topical delivery of drugs to the retina in the posterior segment, thus avoiding invasive injections. The enabling platform is nanotechnology via lipid nanoparticles, liposomes, dendrimers and cyclodextrins which are designed to carry drugs and can be delivered by overcoming corneal and scleral barriers which in traditional dosage systems could not allow topical drugs to reach therapeutic levels in retinal tissues.

Further studies in nano micellar formulations also show that it has potential to solubilize hydrophobic drugs and has a higher ability to penetrate ocular tissues as compared to the other formulations. Should topical preparations have a capability to reach therapeutic levels in the retina in conditions such as age-related macular degeneration, products would devastate the multi-billion-dollar injectable market with the ability to provide the same efficacy without the risks of injections, patient anxiety or burden of the condition due to the need to attend the clinic regularly to undergo the injection procedure.

Mucoadhesive polymers that enhance the residence time of topical medicines on the corneal surface present immediate possibilities of enhancing efficacy of dry eye syndrome treatment, which afflicts hundreds of millions of people around the world with a great gap in effective and convenient treatments. Combination of permeation enhancers and iontophoresis technology and uses of microneedles with nanotechnology platforms forms synergistic strategies that may one day deliver drugs to the posterior segment via minimally invasive or non-invasive methods.

Nanotechnology Opportunity Metrics:

The ophthalmic drug delivery industry is going through a period of transformative innovation with refillable port drug delivery systems implanted in the eye wall, which can deliver drugs continuously over 6-12 months and which, rather than the repeated intravitreal drug injections, can be refilled by operating the eye in the office. The ranibizumab Genentech Port Delivery System, which received FDA approval, provided evidence-of-concept of such a system, which distributed the treatment burden of monthly or bi-monthly intravitreal injections to refill procedures and also every 6 months, without losing therapeutic efficacy compared to conventional injection regimens.

The technology entails a titanium port implantation procedure that uses a catheter that is inserted through the pars plana into the vitreous cavity with an internal drug reservoir that can be refilled via a self-sealing septum with the use of common office procedures, and does not require surgical intervention. This method has both the advantages of prolonged drug delivery and flexibility to tailor therapy to disease activity, change medications in case of insufficient response to therapy or simply do not have to remove implants, which is not the case with biodegradable sustained-release implants.

The port delivery platform is shown to be versatile in the delivery of a wide range of therapeutic agents, and development programs are exploring the delivery of corticosteroids, tyrosine kinase inhibitors, and combination therapeutic agents not just with ranibizumab, as first developed. The technology overcomes the inherent shortcoming of traditional sustained-release implants that release pre-determined amounts of drugs at specific times irrespective of the respective therapeutic needs of individual patients which may differ depending on the severity of the disease, patient response, and disease progression.

Port Delivery System Performance Metrics:

The removal of preservatives, benzalkonium chloride, which is effective against bacteria but leads to corneal toxicity, worsening of the symptoms of dry eye, and destruction of the ocular surface with prolonged use is another prevalent trend in topical ophthalmic delivery. The market is also moving towards preservative-free formulations and the innovation is with multi-dose preservative-free bottle systems with complex tip-technology such as filtering membranes and non-return valves to prevent bacterial entry whilst allowing patients to use the same bottle several months without any preservatives.

Connected ophthalmic devices are becoming available to handle digital health integration, which monitors patient compliance in real-time. The smart dispensers capture the date and time of every drop dispensed and send the information to smartphone apps so that the physician can distinguish between drug ineffectiveness and non-adherence. The technology proves to have specific benefits in glaucoma care where monitoring adherence has a direct effect on the progression of the disease and patient outcomes.

Continuous drug delivery Smart contact lenses with the ability to simultaneously measure intraocular pressure are the future of customized ophthalmic care, uniting drug delivery and diagnostic functions into one platform. These systems allow the ongoing control of the parameters of the disease and provide therapeutic agents, which opens a prospect of closed-loop therapies systems that can adapt to real-time physiological feedbacks and modify drug delivery.

Smart Technology Performance Metrics:

In 2025, North America controls the highest market share of USD 6.2 billion and is projected to have a CAGR of 8.1% till 2034. The dominance of the region is based on advanced ophthalmology subspecialty networks with specialized knowledge in new drug delivery methods, extensive insurance coverage of new ophthalmic therapies provided by Medicare and commercial insurance, the high prevalence of age-related ocular disease, 16.4 million Americans with age-related macular degeneration and 7.7 million with diabetic retinopathy, and pharmaceutical innovation being concentrated with

The United States constitutes 87% of regional market value with Medicare coverage offering a reimbursement basis of costly sustained-release therapies and intravitreal injection procedures and justifying adoption of novel delivery technologies despite high prices. The market has well-established networks of retina specialists (more than 2,800 board-certified vitreoretinal surgeons), well-developed infrastructure of imaging (to provide accurate monitoring of treatment), and patient population is focused on preserving quality of life and functional independence.

The regulatory framework also encourages innovation by providing FDA programs such as breakthrough therapy designation, regenerative medicine advanced therapy designation, and priority review pathways that compress development timelines of therapies to treat serious ailments and unmet medical requirements, and extensive post-market surveillance systems to track real-life safety and effectiveness in generating evidence to support expanded indications.

Key Performance Indicators:

Asia Pacific was the world's fastest-growing region projected to grow at 9.8% through 2034, to USD 4.1 billion in 2025. Massive population scale with high diabetes prevalence resulting in huge diabetic retinopathy burden, the rapid aging of the population with aging populations in Japan, South Korea, and China, advancing health care systems and insurance coverage providing access to more advanced ophthalmic therapies, and rising middle classes willing to pay out-of-pocket to preserve sight, all drive regional expansion.

China has a market share of 38% and is the fastest growing in the region with 140 million diabetes patients forming the largest global population with diabetic retinopathy, 51 million with age related macular degeneration and healthcare reforms are increasing insurance coverage to intravitreal anti-vascular endothelial growth factor therapy with its national reimbursement drug list. The market is enjoying the rapid growth of the retina subspecialty training programs, advanced ophthalmic surgical centers within large urban areas, and government programs encouraging medical tourism.

India shows high adoption acceleration by increasing awareness of the importance of diabetic eye disease screening, increasing the number of beneficiaries of health insurance schemes via Ayushman Bharat program (covering 500 million citizens) and establishing high-volume low-cost delivery models so that more people can access intravitreal therapies. The region enjoys the advantage of having large-scale ophthalmology hospital networks that have been the first to develop affordable care delivery models that provide quality care at cost-structures that can make treatment affordable in price-sensitive markets.

Regional Growth Drivers:

In 2025, Europe had a market value of USD 4.8 billion with a forecasted CAGR of 7.9% until 2034. The area features extensive incorporation of ophthalmic treatments in universal healthcare systems, rigorous regulatory frameworks that provide therapeutic safety and efficacy with the European Medicines Agency, focus on comparative effectiveness studies and health technology assessment as the drivers of treatment authorization and reimbursement choices, and aging populations with 20.3% of the population aged over 65 creating a long-term demand of age-related ocular diseases management

The European market has high levels of uptake of cost-effective therapeutic options such as biosimilar anti-vascular endothelial growth factor agents with biosimilar penetration of 42% of the anti-vascular endothelial growth factor prescription versus 18% in the United States, demonstrating healthcare system focus on cost containment and therapeutic outcomes. The area is a pioneer in the area of developing clinical guidelines, creating real-life evidence, and registry-based outcomes research that guides the best therapeutic regimens.

European systems have an emphasis on strict benefit-risk analysis, long-term safety follow-ups, and open health technology evaluation systems considering clinical and cost-efficiency over existing therapeutic protocols, and imposing market access obstacles to premium-valued innovations that have not proven their superiority but guarantee that approved and reimbursed technologies produce significant clinical worth.

Product Type Insights

The market share of the Novel Drug Delivery Systems is 62% with a valuation of USD 9.8 billion in 2025 at a 9.4% CAGR to the year 2034. This group includes sustained-release implants, intravitreal injections, iontophoresis devices, punctal plugs, ocular inserts and nanotechnology-based formulations that address the limitations of traditional topical drugs with respect to increased bioavailability, prolonged therapeutic effects, and direct delivery to specific tissues of the eye. The segment has an advantage of premium pricing based on better clinical outcomes, less treatment burden, and better patient adherence.

The Conventional Drug Delivery Systems have 38% at USD 6.0 billion in 2025 with traditional topical formulations including eye drops, ointments, and gels which continue to be the conventional therapy of the anterior segment conditions such as glaucoma, dry eye syndrome and allergic conjunctivitis. As competitors introduce new delivery methods, traditional formulations are still relevant due to proven efficacy, positive safety profiles, familiarity with patients, and much lower costs, which allow them to be accessible to a wider population.

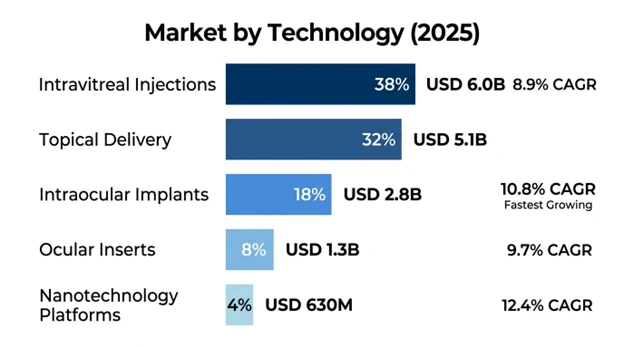

The largest technology segment is Intravitreal Injections which has a market share of 38% with a market value of USD 6.0 billion in 2025 with a 8.9% CAGR through 2034. It is the most common route of delivery used in the posterior segment therapy of age-related macular degeneration, diabetic retinopathy, and retinal vein occlusion because it allows direct drug delivery to vitreous cavity and retinal tissues avoiding anterior segment barriers. The segment enjoys a history of clinical guidelines, safety data of millions of procedures every year, and efficacy of various therapeutic agents.

Topical Delivery controls 32% market at USD 5.1 billion in 2025, which applies to anterior segment disease, such as glaucoma, dry eye and inflammatory disease, in which corneal penetration to target-tissues attains therapeutic levels. Poor bioavailability is a challenge to the segment, but the patients prefer non-invasive administration and continuous formulation developments such as mucoadhesive systems and penetration enhancers are of importance.

Fastest-growing technology segment is Intraocular Implants with 18% market share of USD 2.8 billion in 2025 at a 10.8% CAGR. Sustained-release implants deliver therapeutic drugs to the body continuously over 3-36 months on biodegradable or non-biodegradable levels and avoids regular injections, maintaining therapeutic drug levels. The segment has proven clinical efficacy in terms of treatment adherence as well as patient satisfaction.

Ocular Inserts have a 8% market share of USD 1.3 billion in 2025 with 9.7% CAGR to 2034, which includes the devices that are implanted in the conjunctival fornix to deliver hours to weeks of sustained drug delivery. The technology offers the solution to compliance issues with topical drugs without the invasiveness of injections, which has shown potential in the treatment of dry eye syndrome and inflammatory diseases of the anterior segment.

The Nanotechnology Platforms has 4% market share at USD 630 million market in 2025 at 12.4% CAGR through 2034, which represents emerging technologies such as nanoparticles, liposomes, and dendrimers that help in improving the solubility of drugs, protecting labile molecules, and targeted delivery to select populations of cells within the ocular structures.

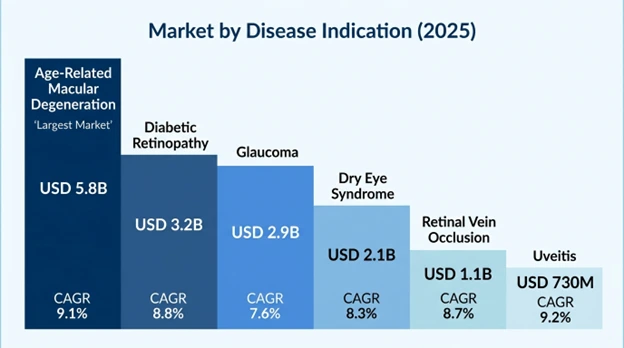

Age-Related Macular Degeneration takes the lead in indication segments with USD 5.8 billion in 2025 and an estimated 9.1% CAGR in 2034, the largest therapeutic market of intravitreal anti-vascular endothelial growth factor agent and sustained-release corticosteroid implants. The suggestion has the advantage of large population of patients with 196 million affected worldwide, established therapeutic efficacy with prevention of loss of vision in 90% of treated patients and chronic treatment needs that have produced high lifetime therapeutic value.

Diabetic Retinopathy has USD 3.2 billion in 2025 with 8.8% CAGR until 2034, and 103 million patients with diabetic retinopathy worldwide with vision-threatening complications needing intravitreal anti-vascular endothelial growth factor or corticosteroid implants. The segment enjoys the increase in diabetes prevalence, enhanced screening, and increased treatment indications of the earlier stages of the disease.

Glaucoma is USD 2.9 billion in 2025 with 7.6% CAGR through 2034 including topical drugs that lower intraocular pressure by a variety of mechanisms as in prostaglandin analogs, beta-blockers, and carbonic anhydrase inhibitors. The segment shows the same growth at a steady rate with aging population and the innovation is revolved around sustained release delivery systems that enhance compliance.

Dry Eye Syndrome has USD 2.1 billion in 2025 with CAGR of 8.3% to 2034 with more than 344 million cases of chronic inflammation of the ocular surface and tear film instability in the world. The segment is advantaged by the increasing disease awareness, diagnostic abilities, and new therapeutic agents such as anti-inflammatory and immunomodulatory drugs.

Retinal Vein Occlusion USD 1.1 billion in 2025 with 8.7% CAGR until 2034, managed as intravitreal anti-vascular endothelial growth factor injections or corticosteroid implants to treat related macular edema. The segment shows a constant growth due to the increasing ageing population and increased adoption of treatments.

Uveitis will contribute USD 730 million in 2025 with a CAGR of 9.2% to 2034 and will include inflammatory diseases requiring corticosteroid treatment in either topical, periocular, or intravitreal routes. The segment enjoys the sustained-release corticosteroid implants that decrease the systemic side effects.

The biggest end-user segment is Hospitals & Clinics with 48% market share with USD 7.6 billion in 2025; which includes the department of ophthalmology, retina specialty practices, and ambulatory surgery facilities with intravitreal injections, implantation surgeries, and surgical operations that require specialized equipment and trained staff. The segment is advantaged by a focalization of complex cases that need complex therapeutic interventions and a well-established reimbursement of facility-based procedures.

Fastest-growing end-user segment, Ophthalmic Centers take 28% market share at USD 4.4 billion in 2025 with 9.1% CAGR. Specialty ophthalmology institutions show an operation efficiency in terms of high-volume standardized processes, specialized equipment, and a wide range of services with a focus on diagnostics, treatment, and follow-ups.

Home Healthcare has 16% market share at USD 2.5 billion in 2025, treating patients who administer topical drugs themselves, use punctal plugs or inserts into their eyes and managing chronic illnesses such as glaucoma and dry eye syndrome. The segment enjoys patient choice of home-based care and cost benefits as opposed to facility-based administration.

Ambulatory Surgical Centers will have market share of 8% at USD 1.3billion in 2025, offering intravitreal injection procedures and implant surgeries in outpatient facilities with cost benefits over hospital-based centers. The segment reflects expansion with payer inclination towards less expensive ambulatory care and patient inclination towards convenient community-based care.

Global ophthalmic drug delivery systems market is moderate in terms of the concentration as the leading seven players maintain the industry value of about 56-63%based on a broad portfolio of products across various delivery technologies and disease markers, the extensive clinical development pipeline, the established network of relationships with ophthalmology specialist networks, and advanced manufacturing facilities that guarantee the quality of products and supply consistency. Competitive differentiation focuses on clinical evidence of better efficacy or safety profiles, new delivery technologies that lead to less treatment burden, service programs that provide full-service support and clinical adoption, and strategic collaboration with healthcare organizations that ensures preferred formulary positions.

The most active pharmaceutical companies are pursuing a variety of strategic options such as Regeneron and Genentech developing biological therapeutics and proprietary delivery platforms, Novartis and Bayer with broad portfolios and multiple disease indications and technologies to deliver them and specialized companies with Bausch + Lomb and Alcon with an emphasis on surgical products and anterior segment therapies. Competitive environment is increasingly focusing on biosimilars competition in already existing anti-vascular endothelial growth factor drugs, which puts pressure on pricing but expands patient access.

Strategic positioning is becoming more about the overall disease management model that combines pharmaceuticals with diagnostic technologies, digital health solutions and patient support services that can bring forth differentiated value propositions beyond drug delivery, and alliances between pharmaceutical companies and medical device manufacturers are speeding up the creation of sophisticated delivery platforms.

March 2026: Novartis stated that its new port delivery system brolucizumab had positive Phase III results in neovascular age-related macular degeneration by showing non-inferiority to monthly intravitreal injections with a median refill interval of 32 weeks. The company submitted regulatory applications in US and Europe with the expected decisions on approvals in late 2026.

February 2026: Regeneron Pharmaceuticals was approved by FDA to use high dose aflibercept formulation to allow longer dosing intervals, up to 16 weeks, to treat neovascular age-related macular degeneration and diabetic macular edema, reducing treatment burden by increasing the dosing interval. Commercial release in Q2 2026.

January 2026: Bayer AG acquired specialized ocular drug delivery company with USD 380 million, gaining access to proprietary nanoparticle platform technology that has the capacity to deliver gene therapy vectors and RNA therapeutics to specific retinal cell populations, bolstering Bayer ophthalmology pipeline.

December 2025: AbbVie Inc. reported favorable Phase II outcomes with new tyrosine kinase inhibitor administered as sustained-release intravitreal implant to diabetic macular edema showing that treatment can last 6 months with an equivalent effect to monthly anti-vascular endothelial growth factor injections.

November 2025: Alcon Inc. released next-generation sustained-release dexamethasone implant with a superior insertion device to facilitate easier implantation procedure and lower complication rates, getting FDA approval of the macular edema related to retinal vein occlusion and non-infectious uveitis.

List of Key Players in Global Ophthalmic Drug Delivery Systems Market

Global Ophthalmic Drug Delivery Systems Market Segments

By Product Type:

By Technology:

By Formulation:

By Disease Indication:

By Route of Administration:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

26 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.