Share this link via:

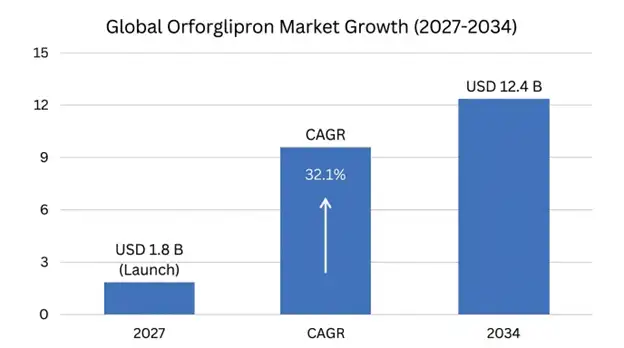

The global orforglipron market is projected to emerge as a transformative segment within the rapidly expanding GLP-1 receptor agonist therapeutic class, with the market expected to reach USD 1.8 billion in 2027 following anticipated regulatory approvals in major markets, expanding to USD 12.4 billion by 2034, representing a compound annual growth rate of 32.1% during the forecast period (2027-2034).

Orforglipron is the first commercially available, once-daily, oral, non-peptide GLP-1 receptor agonist, overcoming the basic hurdles that have slowed the widespread use of GLP-1 therapies. Oforglipron activates GLP-1 receptors in a structurally different way from other peptide-based GLP-1 receptor agonists (semaglutide, liraglutide, dulaglutide) that must be injected subcutaneously or take complex oral formulations, which are required to be taken with food and water and at a fixed time.

Thanks to its therapeutic value, orforglipron can be used in both two largest and most economically and public health impactful chronic disease groups in modern medicine: people with type 2 diabetes mellitus (T2DM) (537 million adults in the world) and obesity (around 890 million adults in the world). These are often present in the same patient, and share overlapping pathophysiological mechanisms and therapeutic goals: maintenance of a sustained glycemic status, significant body weight loss, and total cardiovascular risk reduction. The Phase III ACHIEVE trial for type 2 diabetes showed HbA1c decreases of 1.3% to 2.1% along with a parallel weight reduction of 7.9% to 10.1%, whereas the ATTAIN obesity trial showed a 16.0% reduction in body weight at the highest dose, representing efficacy profiles like injectable GLP-1 receptor agonists.

The commercial architecture around orforglipron extends beyond pharmaceutical product sales and is a complete therapeutic ecosystem, with streamlined administration protocols, digital health monitoring platforms, chronic disease management programs and personalized treatment optimization strategies. The absence of injection-related barriers is expected to significantly increase the number of patients beyond the current 30-40% of eligible patients using a GLP-1 receptor agonist, including populations that are needle-averse, those managed by primary care and emerging market segments that have barriers to access due to cold-chain logistics and training for injections.

| Report Coverage | Details |

|---|---|

| CAGR | 32.1% |

| Forecast Period | 2027-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Indication, Patient Demographics, Dosage Strength, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Eli Lilly and Company, Novo Nordisk, Pfizer Inc., AstraZeneca, Sanofi, Boehringer Ingelheim |

Get more details on this report - Request Free Sample

The two major categories of the global burden of disease driving growth of the orforglipron market are the remarkable and rapid global burden of obesity and type 2 diabetes, which overlap in populations, and present a massive unmet therapeutic need for effective pharmacological treatments. According to the International Diabetes Federation, there are 537 million adults with diabetes worldwide by 2025 and 783 million by 2045; the World Health Organization estimates that there are 890 million adults with obesity worldwide, which is an epidemic and has become a major factor in utilization of and costs of healthcare systems.

The combination of these epidemics results in a patient population of 250-320 million people worldwide who may have both conditions, and, because the GLP-1 receptor agonist class of drugs act on the same mechanisms to improve glycemic control and weight loss, these patients are the highest priority for these drugs. These conditions are chronic, progressive and require decades of therapeutic management with average treatment duration >15-20 years for most patients, thus high therapeutic value over a lifetime that warrants premium prices for highly effective drugs.

The economic impact of obesity and diabetes has become a crisis with direct medical costs in 2020 totaling USD 1.96 trillion annually worldwide, including hospitalizations due to cardiovascular disease, dialysis for diabetic nephropathy, surgical costs for diabetic foot complications, and disabled costs from work-limiting complications. This economic fact has dramatically altered health plan thinking about paying for high-cost, high-efficiency treatments that show that they produce tangible declines in downstream complication rates and health care utilization.

Key Performance Indicators:

The transformative commercial opportunity for orforglipron comes pretty much from the fact that it can deliver GLP-1 receptor agonist pharmacology using a normal oral tablet, so it avoids the biggest “real world” sticking points that have limited how much this top therapeutic class gets used. Injectable GLP-1 receptor agonists, even though they show outstanding clinical value for blood sugar control, weight loss, and cardiovascular outcomes, still run into adoption issues. These issues are tied to people not wanting to start, and then continue, self-injection, plus some healthcare providers are just reluctant to prescribe injectables in primary care. On top of that there are also practical hurdles like cold-chain storage logistics and the need for extra training around injection devices.

Looking at broad patient preference studies, demonstrate that that about 28-44% of patients who could take a GLP-1 receptor agonist decline starting treatment, mainly because of injection aversion. That translates to tens of millions of patients worldwide who stay undertreated, even when the clinical case is clear and guidelines recommend it. Oral semaglutide helps with the route thing, but it still needs kind of tricky administration steps: fasting, limiting the water volume, and waiting 30 minutes before eating, or taking other meds. So, adherence gets harder in everyday life, and it can also make prescribing less convenient for patients who already have complicated medication schedules.

Orforglipron’s small-molecule design lets it be taken orally without special steps, in a simple way that feels like common oral antidiabetic agents like metformin or SGLT2 inhibitors. That sets it up for smoother placement into existing treatment pathways and more familiar primary care prescribing habits. This oral approach is expected to drive serious market uptake in primary care, where most diabetes and obesity care decisions happen. And because primary care physicians tend to feel more at ease prescribing pills than injectable options, especially since those injectables require patient training and ongoing injection site monitoring, orforglipron has a clearer path to broader use.

Adoption Barrier Elimination Metrics:

A key competitive advantage that can help orforglipron market expansion is basically tied to the plain manufacturing and distribution upsides that come with small-molecule pharmaceutical production, compared with the much more complicated biological manufacturing steps needed for peptide based GLP-1 receptor agonists. With the usual chemical synthesis routes used for small-molecule drugs like orforglipron, there is an already known manufacturing setup, highly scalable too, that can be ramped up quickly for worldwide demand. It avoids the specialized bioreactor capacity, plus the extra layered purification systems and the tougher quality control conditions that tend to show up with peptide manufacturing.

Then the supply chain benefit kind of follows you all the way through. Oral tablets, for the most part, only need standard pharmaceutical cold-chain handling, not the specialized ultra-cold storage and transport setup that peptide stability usually demands. That simplification makes it easier to plug into conventional retail pharmacy networks, mail order systems, and even some emerging market distribution channels. In places where cold-chain infrastructure has been weaker, this historically limited access to injectable GLP-1 options, so the difference matters.

On costs, the small-molecule manufacturing cost profile does require a serious upfront investment, but it also gives a path toward economies of scale and, later, generic entry after patent protection ends. That sequence could broaden access to GLP-1 therapy globally. By contrast, peptide-based biologics keep a higher cost baseline because the process is more intricate, and that keeps biosimilar competition harder. This effect can be especially strong in emerging markets, where advanced biotechnology manufacturing capacity still isn’t widely available.

Manufacturing and Distribution Metrics:

The primary constraint slowing down immediate orforglipron market reach is pretty tied to the uncertainties around its long-term safety profile and the cardiovascular outcome evidence that regulators, prescribing physicians, and payers usually want before they feel comfortable with chronic disease use. Since orforglipron is a novel non peptide small-molecule GLP-1 receptor agonist, it doesn’t yet have a huge long-term safety record built from more than a decade of real clinical experience with the peptide based GLP-1 receptor agonists. So, many stakeholders take a wait and see stance, with careful prescribing, until broad post marketing surveillance and cardiovascular outcome trial results come through clearly.

The GLP-1 receptor agonist class already has known links with gastrointestinal side effects such as nausea, vomiting, diarrhea, and constipation, and those can trigger treatment stopping in roughly 15-25% of patients during the early titration window. Even though these symptoms are often manageable through slower dose escalation plans and supportive interventions, the tolerability stuff really matters for real world adherence and persistence, and those rates end up deciding whether the therapy keeps working overtime. That in turn feeds into long-term effectiveness and commercial success.

Regulatory authorities generally ask for cardiovascular outcome trials for new diabetes therapies, and although Eli Lilly has started the CONVEY cardiovascular outcomes study for orforglipron, meaningful results aren’t expected until 2028-2029. Without clear cardiovascular safety and efficacy data, prescriber confidence and payer coverage choices may wobble, especially for patients who already have cardiovascular disease. These patients are often high priority candidates for GLP-1 receptor agonist therapy, largely because existing outcome data for the injectable GLP-1 agents has already shown benefits.

Safety and Regulatory Timeline Constraints:

Reimbursement coverage policies are a big market access problem, especially for the obesity indication, because payer coverage stays kind of uneven and restrictive across a lot of healthcare systems worldwide. In the United States, Medicare Part D has historically left weight loss medications out, and this is tied to Social Security Act language, it really impacts around 67 million beneficiaries, who are a major share of the highest-prevalence obesity group. There are legislative ideas, like the Treat and Reduce Obesity Act, that could open coverage, but the timing and exact reach of any policy shift is still unclear, or at least hard to pin down.

On the commercial insurance side, coverage for obesity pharmacotherapy varies a lot. Many employer-sponsored plans exclude it or limit it, mainly due to cost worries, and these costs are driven by the high “sticker” prices of the current GLP-1 receptor agonists when used for obesity. For example, injectable semaglutide for obesity is priced at about USD 1,349 per month. Tirzepatide is roughly USD 1,059 per month. So even when coverage exists in theory, people still hit affordability barriers through high deductibles, copays that feel heavy, or prior authorization hurdles.

Also, obesity treatment is chronic by nature, so pharmacotherapy often needs an indefinite duration to keep the weight loss results. That means lifetime treatment spend, and it puts payers under pressure, because they may not want to offer open-ended coverage without strong proof of durable clinical benefit and cost-effectiveness, especially if it’s not clearly shown through reduced healthcare utilization related to obesity complications. For that reason, the orforglipron pricing strategy is going to matter a lot for how deep the product can go into the market. Early projections from analysts suggest a list price around USD 800–1,100 per month for obesity indications.

Reimbursement Challenge Metrics:

transformative market opening to broaden orforglipron access across emerging markets in Asia, Latin America, Middle East and Africa. In these places the combined burden of type 2 diabetes and obesity has basically gone epidemic, but GLP-1 receptor agonist penetration is still extremely low. The reason tends to be cost, plus infrastructure and the annoying administration complexity that comes with injectable formulations, so a lot of systems just don’t keep up. China is still the biggest single-country diabetes population worldwide, with about 140 million affected adults. Meanwhile India has around 101 million diabetes patients, and with a rapidly urbanizing population plus rising obesity prevalence there are market opportunities at an almost extraordinary scale.

An oral tablet formulation removes the cold-chain storage problem, which is often the core infrastructure barrier that blocks injectable GLP-1 rollouts in regions where refrigeration capacity is limited. That change makes distribution possible using standard pharmaceutical supply chains, including rural and semi urban healthcare environments where most diabetes and obesity patients get treatment. Also, the manufacturing cost structure based on small molecule synthesis may allow pathways for tiered pricing strategies. In other words, it could help make orforglipron affordable at price points that fit within emerging market healthcare budgets and insurance frameworks, at least more realistically than injectables.

Regional pharmaceutical partnerships along with local manufacturing licensing arrangements are strategic levers too. They can speed up market penetration while also turning pricing to local economic conditions. On top of that, removing injection training requirements and specialized storage infrastructure lowers implementation costs for healthcare systems. That reduction helps broader deployment through primary care networks, which in many emerging markets serve most chronic disease patients.

Emerging Market Opportunity Metrics:

Beyond the core type 2 diabetes and obesity indications, orforglipron really looks like it has room to grow across a wider set of metabolic and neurological areas where GLP-1 receptor agonist pharmacology makes sense, plus there’s early clinical signal. Metabolic dysfunction-associated steatohepatitis, formerly known as non-alcoholic steatohepatitis, is estimated to impact about 115 million adults worldwide, and there’s still a big gap in what pharmacology can do right now. In that space GLP-1 receptor agonists have shown things like reduced hepatic fat, improvements in liver enzymes, and even histological progress. These effects are thought to come from a mix of reduced hepatic lipogenesis, along with better insulin sensitivity.

Cardiovascular risk reduction which could be a serious angle for indication expansion. The GLP-1 class, in general, has already shown meaningful decreases in major adverse cardiovascular events among people with type 2 diabetes and established cardiovascular disease. The CONVEY outcomes trial is the one to watch for orforglipron, and if it turns out positive it could justify use not just for glucose or weight management, but also for cardiovascular protection. That kind of label change could expand the addressable patient base a lot, and it may also help premium pricing, since it would be tied to demonstrated outcome benefits.

The longer arc of the pipeline includes investigational uses such as polycystic ovary syndrome affecting roughly 116 million women of reproductive age globally, plus Alzheimer’s disease with a focus on cognitive protection, and even addiction disorders. Those areas are the sort of opportunities that might extend the product’s commercial life, and widen the market scope for orforglipron, well beyond the first approvals. The oral delivery advantage matters a lot here, especially for neurological indications, where staying on therapy over time, and patient willingness, tend to decide whether treatment sticks and works in practice.

Indication Expansion Opportunity Metrics:

The market for orforglipron is developing against the backdrop of a healthcare setting characterized by the technological and clinical success of the integration of digital health with the pharmacological treatment of chronic disease. The combination of digital health technologies including medication adherence monitoring through smart packaging, the connection of continuous glucose monitoring devices, diet and exercise tracking, and telemedicine-driven clinical services has been shown to deliver tangible benefits in terms of lowering HbA1c, maintaining weight loss, and improving patient satisfaction compared to the use of medicines alone.

The orally administered form of orforglipron allows its integration into the digital health landscape via established pharmaceutical supply chains without the need for additional training in self-injection or proper sharps waste disposal. Electronic medication adherence monitoring, automated pharmacy refills, and dose alerts through apps can be introduced using existing digital technology solutions proven effective in other therapeutic areas for chronic diseases.

There is increasing interest among payers for value-based contracting mechanisms that reward payments based on metrics such as reduction in HbA1c levels, sustained weight loss, and cardiac risk prevention. The use of digital health tools to objectively measure outcomes serves as a mechanism to enable this type of innovation in healthcare payment. Value-based contracts can also serve as a means of enhancing market access and pricing.

Digital Health Integration Metrics:

Regional Insights

North America: Market Leadership Through Advanced Healthcare Infrastructure and Commercial Readiness

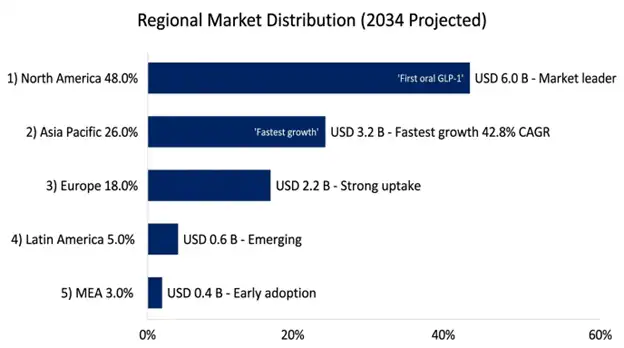

North America will continue its reign of market dominance with its anticipated 48% share of the total global orforglipron market revenue throughout the next two decades, attributed to the world’s highest GLP-1 receptor agonist use per capita, advanced specialty network infrastructures for endocrinology and obesity care, effective regulatory infrastructure allowing rapid review of novel pharmaceutical applications, and effective reimbursement infrastructure providing the basis for the introduction of novel metabolic therapies regardless of existing deficiencies in obesity indications.

The US accounts for almost 87% of total regional market revenue thanks to high price markets, which result in disproportionately high revenues from modest patient numbers, established infrastructure for direct consumer marketing of medications, and specialized pharmacies accustomed to distributing expensive pharmaceuticals for chronic diseases requiring special authorization and management programs.

The regulatory environment fosters innovations with initiatives from the Food and Drug Administration (FDA) such as breakthrough designation, priority review pathways, and fast-tracked approvals for drugs treating serious diseases without adequate medical solutions. Orforglipron is among the drugs that have been granted priority review status due to its ability to meet unmet needs regarding the treatment of type 2 diabetes and obesity, and whose approvals are expected by 2026.

North American Market Leadership Metrics:

Asia Pacific: Fastest Growth Through Population Scale and Infrastructure Compatibility

Asia Pacific is still the fastest-growing regional market, with a projected CAGR of 42.8% through 2034, mostly because the region holds a disproportionate share of the global diabetes burden. People here also tend to prefer oral medications over injectable therapies, for cultural and practical reasons, plus pharmaceutical insurance coverage is expanding quickly. The middle-class is growing, and that gives more purchasing power for advanced long-term treatment options for chronic disease. In 2025 the region includes about 206 million adults living with diabetes, which is 38% of the worldwide burden. Prevalence is especially high in places like China, India and several Southeast Asian countries, where rapid economic development, and lifestyle transitions are happening at the same time.

China is leading the regional growth story, with roughly 140 million people with diabetes. That’s the biggest single-country diabetes population globally, and it comes alongside about 51 million adults with obesity. Healthcare reforms are also widening access, partly through insurance coverage that’s expanding via national reimbursement drug list inclusion mechanisms. The National Healthcare Security Administration has shown it’s willing to bring in newer diabetes therapies using negotiated pricing frameworks, these can substantially cut list prices, in return for volume commitments and broader patient access across large populations.

The oral administration advantage of orforglipron matters so much in Asian markets. Injectable therapy adoption has often lagged what the epidemiology would suggest, due to cultural preferences, healthcare delivery infrastructure limitations, and cost sensitivity. Even now, GLP-1 receptor agonist penetration among eligible patients averages only 3.8% across Asia Pacific, versus 22.4% in the United States, which points to a significant opening for growth in the oral therapy market.

Asia Pacific Growth Opportunity Metrics:

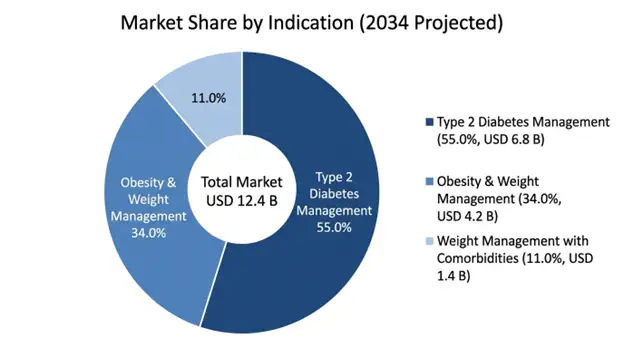

Type 2 Diabetes Management feels like the dominant indication segment, with a projected USD 6.8 billion market value by 2034, and that is about 55% of total orforglipron revenue. This specific label gets a big edge because the Phase III clinical picture looks the most complete through the ACHIEVE program, plus there are regulatory approval routes already in place, and reimbursement mechanics that are well defined. Also, it sits in the largest immediately reachable patient population among the approved indications. In addition, diabetes indication shows clear clinical endpoints that regulators accept, lots of comparator context versus existing GLP-1 receptor agonists, and guideline-supported prescribing logic.

Obesity and Weight Management looks like the highest-growth indication segment, with a projected USD 4.2 billion contribution by 2034. It is forecast to grow at a 38.4% CAGR, after the anticipated regulatory go-ahead tied to the ATTAIN Phase III program data, where 16.0% body weight reduction is reported at an optimal dosing approach. Still, this indication has a tougher time with reimbursement uncertainty compared to the diabetes area, but it also serves the wider global patient base. And it is the therapeutic space where the oral administration advantage really gives the most noticeable commercial separation versus injectable options.

Weight Management with Comorbidities accounts for the remaining market share, covering people with obesity plus diabetes, cardiovascular disease, or other metabolic complications, who can gain from broader cardiometabolic risk reduction. This segment tends to show the greatest per-patient lifetime value, partly because there is an overlap indication, and because treatment is chronic.

Retail Pharmacies are basically the biggest distribution route at 42% of the market volume, and it kind of shows how orforglipron fits into an oral therapy idea that can move through normal pharmaceutical distribution networks without any special handling kind of needs. Also, the retail side tends to do well because patients already feel comfortable with it, they get easier access, and it plugs into the existing prescription management systems, so dispensing can happen seamlessly alongside other long-term, chronic disease medications.

Specialty Pharmacies at 28% of distribution volume. This portion is mainly for the more complicated patients who need close, ongoing observation, careful dose optimization, and that broader patient support during the start of treatment and throughout maintenance, or whatever you want to call it. Specialty pharmacies really bring useful pieces, like prior authorization help, insurance coverage navigation and clinical monitoring too. All that, together, helps improve treatment outcomes and supports persistence over time.

Hospital Pharmacies contribute 18% of distribution volume. They’re mostly used for inpatient diabetes management and for immediate after-discharge medication reconciliation, so medication isn’t just left hanging. And Online Pharmacies, meanwhile, are the fastest-growing channel at 12% market share, largely because people like the convenience of ordering quickly and getting home delivery. This is especially relevant for chronic medications where long-term adherence matters, not just a short course.

Primary Care Settings are still the most strategically important end user group, and they’re expected to make up about 54% of prescribing volume by 2030. This reflects orforglipron’s role as an accessible oral therapy, that can be started and kept up within primary care workflows, where most diabetes and obesity patients already get ongoing medical care. Having it oral means there’s no need for injection training, and no extra specialized monitoring.

Specialty Diabetes and Endocrinology Centers represent roughly 31% of prescribing volume, and this points to early adoption prescribing in the first commercial window, plus continued management for patients with more complex needs who really do require closer observation. These centers also support combination therapy tuning, and care for refractory disease when it does not respond the usual way. They also have a big impact on real world evidence, they help set up treatment protocols, and they train primary care physicians on patient selection and monitoring.

Weight Management and Obesity Medicine Clinics contribute around 15% of prescribing volume, basically capturing practices that focus only on obesity treatment, and broader weight management programs. In those clinics the pharmacotherapy gets blended with lifestyle interventions, behavioral counseling, and longer-term maintenance planning.

The global orforglipron market works in this very intense competitive space, mostly led by established injectable GLP-1 receptor agonists and then newer oral options coming in, and Eli Lilly is basically holding the first-mover edge here because orforglipron has that non-peptide oral mechanism that’s kind of distinct. The main competitive pressures come from things like Novo Nordisk’s semaglutide franchise, covering both diabetes and obesity, plus Eli Lilly’s own tirzepatide which is dual GLP-1/GIP receptor agonism in practice, and then there are pipeline challengers too, including Pfizer’s danuglipron program, along with other small-molecule GLP-1 methods in different clinical development stages.

When it comes to what really sets orforglipron apart, it’s mostly oral administration convenience, manufacturing scale-up or “capacity” advantages, and the possibility of wider global reach compared with the injectable products that often need cold-chain logistics and all those extra steps. Still, the pressure doesn’t disappear, because the already-known injectable agents come with long-term safety evidence, proven cardiovascular outcome benefits, and prescriber familiarity that can delay early uptake until more real-world evidence.

For positioning, the company’s strategy leans on oral convenience, smoother prescribing workflows that can fit into primary care routines, and manufacturing capacity that supports steady global supply, without the kind of shortage disruptions that have happened now and then with injectable GLP-1 availability. Going forward, long-term competitiveness hinges on showing efficacy that’s comparable with injectable alternatives, while using the oral delivery benefits to push market penetration beyond today’s current GLP-1 therapy adoption levels.

March 2026: Eli Lilly said the FDA has okayed orforglipron for type 2 diabetes, and they’re planning a commercial start in Q2 2026 across the United States. This approval really leaned on the broader ACHIEVE Phase III program numbers, which showed statistically meaningful HbA1c declines plus body weight loss across essentially all dose levels.

February 2026: Eli Lilly also sent a supplemental new drug application to the FDA for that indication, using ATTAIN Phase III data. In that set of results, the 36 mg dose came with a 16.0% average body weight reduction over 36 weeks. The PDUFA action date is expected to land in Q4 2026.

January 2026: the European Medicines Agency accepted the Marketing Authorization Application for orforglipron under the centralized procedure. The decision is expected around 2027, which would allow a simultaneous big launch across European Union member states.

December 2025: PMDA started a priority review for the new drug application. The review timeline is being sped up thanks to the unmet medical need designation, specifically for oral GLP-1 therapy within Japanese diabetes and obesity groups.

November 2025: Eli Lilly is also putting money into production. They announced strategic manufacturing capacity expansion investments totaling USD 2.4 billion across several facilities, aimed at backing the global orforglipron launch and handling demand that they expect will overshoot the early production capacity forecasts.

List of Key Players in Global Orforglipron Market

Global Orforglipron Market Segments

By Indication:

By Patient Demographics:

By Dosage Strength:

By Distribution Channel:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

14 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.