Share this link via:

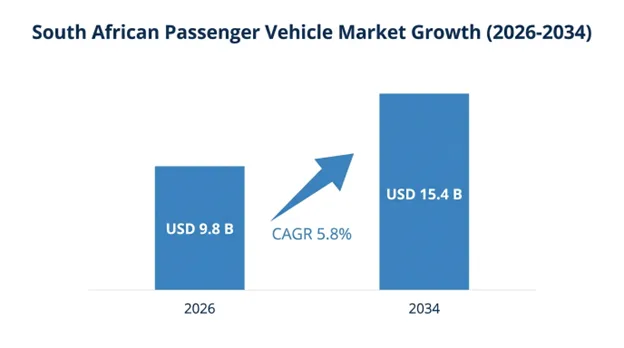

The South African passenger vehicle market was valued at USD 9.2 billion in 2025 and is projected to reach USD 9.8 billion in 2026, expanding to USD 15.4 billion by 2034, growing at a CAGR of 5.8% during the forecast period (2026-2034).

South Africa is the biggest and most advanced automotive market in Africa, acting not only as a prominent automotive production center but also as a major vehicle export hub and an intricate domestic market driven by structural economic disparities, logistical obstacles, and ever-changing consumer tastes. In South Africa, there exists an unusual dualism wherein vehicle assembly operations by global original equipment manufacturers (OEMs) such as Toyota, Volkswagen, Ford, BMW, and Mercedes-Benz runs side-by-side with extensive auto imports.

Economic and Manufacturing Context:

The South African passenger vehicle market closely reflects the country’s broader economic structure. It features an affluent middle- and upper-class population that drives the premium segment market, while a much larger lower-income population faces affordability constraints, is unable to participate in the purchase of vehicles due to affordability issues, high finance rates, and uncertainty in their future income prospects. Consequently, the market is characterized by a much larger size of the used cars segment relative to the new car segment, featuring a ratio of 2.8 used vehicles for every new one purchased.

In terms of the contribution of the automotive industry to the economy of South Africa, the industry represents 7.5% of GDP if one takes into consideration its entire value chain from manufacturing to retail and the aftersales market. The country's six vehicle assembly plants manufacture about 620,000 units per year. Out of the total production volume, 65% is exported to over 150 countries around the world, primarily owing to preferential trade agreements such as the African Growth and Opportunity Act (AGOA) and the EU-South Africa Trade, Development, and Cooperation Agreement.

Consumer Behavior and Market Dynamics:

South African consumers exhibit several distinct vehicle purchasing behaviors, among which one can note high financial cost to finance a car in this country, since its prime lending rate was fluctuating around 10.5-11.75%. High insurance costs persist due to elevated vehicle theft and accident rates, along with unpredictable prices of fuel caused by the exchange rate of the South African rand to US dollar and world oil prices. In addition, there are significant differences in the quality of the country's roads in urban and rural areas that result in certain preferences in purchasing passenger cars with high ground clearance.

The passenger vehicle market has been increasingly dominated by SUVs and crossovers that take up over 38% share on the market and replacing sedans across multiple price segments. The reason for this phenomenon may be found in such factors as deteriorated road infrastructure and preferences towards elevated driving position, but at the same time the segment of cheap hatchbacks was still in great demand.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 9.2 Billion |

| Forecast Value | USD 15.4 Billion |

| CAGR | 5.8% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Gauteng |

| Fastest Growing Market | Western Cape |

| Segments Covered | By Vehicle Type, Fuel Type, Price Segment, Sales Channel, End-User |

| Countries Covered | Gauteng, Western Cape, KwaZulu-Natal, Eastern Cape, Other Provinces |

| Key Market Playes | Toyota SA, Volkswagen SA, Ford SA, BMW SA, Mercedes-Benz SA, Hyundai SA, Chinese OEMs |

Get more details on this report - Request Free Sample

South Africa’s economy, which was recovering from the impact of the pandemic despite being fragile, has been creating gradual demand from people within the aspirational middle class who have been postponing major purchases when faced with economic and load-shedding challenges. The ongoing trend of monetary easing, which began in 2024 when the South African Reserve Bank reduced the prime lending rate from 11.75% to an estimated 9.5-10.0% by 2026, is making it easier for people to finance vehicles and hence stimulate demand among credit-dependent consumers who account for 85% of vehicle sales.

The South African government plans to invest ZAR 1 trillion in infrastructure projects within five years which will provide job creation and income generation in the construction industry and other sectors supporting vehicle manufacturing. The better and more reliable power availability after operational efficiency of Eskom and increased use of renewable energy decreases risks to businesses that were holding back consumer spending.

The long-term shift toward SUVs and crossovers is considered a structural growth driver that not only considers the consumer’s lifestyle needs but also addresses transport considerations in a South African landscape characterized by varied road infrastructures. SUV share has grown from 28% in 2020 to 38% in 2025 and forecasts point to further growth into the range of 45-48% by 2030.

Significant disparities exist in the quality of South Africa’s road infrastructure, Whereas the national roads and the urban roads are of high quality, the secondary roads tend to be of poor maintenance. Higher ground clearance and four-wheel-drive capability provide practical advantages on such roads. Another favorable point for the SUV segment is their decreasing prices due to global competition.

South Africa’s economic structure remains the primary constraint on passenger vehicle market expansion, with 32.9% unemployment rate by the narrow definition and 43.1% unemployment rate by the broad definition. Due to the extremely high unemployment rate, as well as very high-income disparity with 0.63 Gini coefficient, many consumers remain unable to afford vehicle ownership despite financing availability.

In 2025, the average cost of a new vehicle in South Africa was about ZAR 485,000, which meant monthly repayments ranging from ZAR 8,500 to ZAR 10,200 for a 72-month period with currently available interest rates, i.e. about 85-105% of an average formal sector wage per month. This limits the addressable market for new vehicles, only about 4-5 million households.

Even though South Africa’s electricity situation improved quite a lot during 2024-2025, the extensive load-shedding experienced between 2021 and 2024, continues to negatively affect consumer confidence, on how firms decide to invest, and on overall economic growth. That lingering impact continues to suppress vehicle demand. At the same time, the continued uncertainty around Eskom’s long-term financial stability, the reliability of its aging generation fleet, and how quickly the renewable energy shift is happening, keeps a low-level worry in the air for both consumers and companies.

Infrastructure issues beyond power also weigh in, like road quality that keeps deteriorating in many municipalities, plus fuel costs that keep climbing, which together raise total costs of owning a vehicle. For many households, that really strains already tight budgets. This hits electric vehicle adoption extra hard, because range anxiety does not stay alone, it mixes with charging infrastructure gaps. Concerns regarding grid reliability further complicate EV purchase decisions.

South Africa is at an inflection point for the uptake of electric vehicles with government’s Green Transport Strategy and South African Automotive Masterplan 2035 providing the basis for the structuring of EV industry growth. With less than 0.5% of electric vehicle uptake against total new vehicles purchased, the market is shifting from curiosity among early adopters towards commercial development through increasing charging infrastructure availability and introduction of cheaper EV models.

Incentive framework for EV production provided by the Department of Trade, Industry and Competitions, along with commitment from South African corporations towards making sustainable transport choices within their corporate fleets, presents structured demand which may lead to increased uptake beyond that fueled by organic market developments. At this stage, the biggest immediate growth opportunity is Hybrid Electric Vehicles which provide a transition into better fuel consumption without use of charging infrastructure.

The evolution of automotive retail presents significant growth opportunities by means of omnichannel digital retailing that allows customers to arrange financing, trade-in evaluations, and even car configurations via online platforms. Car subscription services and guaranteed future value financing models are some examples of how consumers can enjoy easier and risk-free approaches to enjoying cars, particularly young consumers.

ADAS features such as adaptive cruise control, lane-keeping assist, and autonomous emergency braking were previously limited to high-end and luxury vehicles but are gradually becoming standard equipment on mid-segment and budget cars, mostly due to competition between Chinese OEMs who use technology to distinguish themselves from other companies, which then prompts established brands to improve their own standard equipment.

New Energy Vehicles (NEVs), including battery electric vehicles, plug-in hybrids, and hybrid vehicles, are steadily reshaping the market landscape. Hybrid Electric Vehicles constitute the most rapidly growing category of automobiles, with a forecasted compound annual growth rate (CAGR) of 14.5% until 2034, satisfying South African consumers’ needs in terms of fuel efficiency without dealing with issues faced by plug-in hybrids.

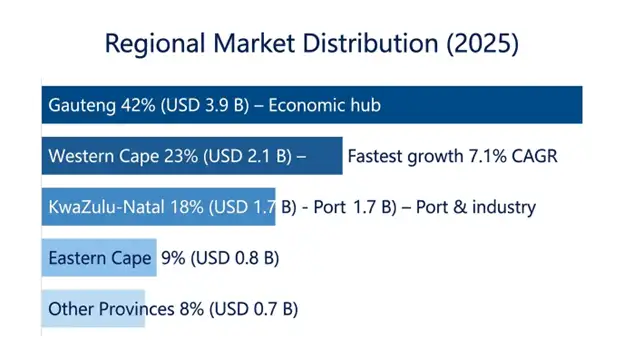

Gauteng holds 42% of the country’s sales of new vehicles worth USD 3.9 billion in 2025. This is because Gauteng is the economic hub of the country with a population of approximately 16.1 million. It is home to the headquarters of companies, banks, and industries, which have created a high level of middle and upper-middle class employment, thus creating a demand for luxury vehicles. Johannesburg and Pretoria have the largest share of luxury and premium cars sold in the country.

The Western Cape is the fastest-growing regional market with a compound annual growth rate (CAGR) of 7.1% between 2025-2034, mainly due to an increase in population due to internal migration, increased tourism industry growth, growth of the technology sector, and Cape Town’s rising reputation as a destination of choice for wealthy individuals.

KwaZulu-Natal represents 18% of the total sales of passenger vehicles in the country, with Durban being the main center of commerce and a port town. The industrial sector of KwaZulu-Natal creates middle-class jobs through manufacturing automotive components located near the Toyota facility at Prospection. The Durban port is responsible for the importation and exportation of vehicles.

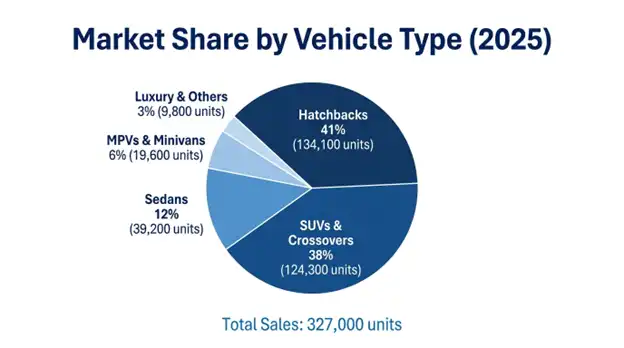

The SUV & Crossover segment dominates market growth with a 38% volume share in 2025, translating into approximately 124,300 units and a growth rate of 9.2% CAGR until 2034. These vehicles have benefited from a growing range of models across all price categories across all pricing levels, higher lifestyle orientation of buyers, and utility of increased ground clearance. Entry level crossovers are seeing the fastest pace of growth due to competitive offerings by Chinese and Korean car makers.

The hatchback category maintains the largest volume share with a 41% share in 2025, translating into 134,100 units being the most popular choice of middle-income buyers seeking a private vehicle option that fits into their budget. These segments continue to be dominated by high-performance cars such as the Volkswagen Polo, Toyota Starlet, and Suzuki Swift.

The petrol engine cars have a market share of 72%, which stands at around 235,500-unit sales in 2025 because of fuel availability and infrastructure, and customer familiarity. Diesel vehicles account for a 22% market share and are primarily concentrated in SUV and premium segments. Hybrid Electric Vehicles have a 5.2% market share growing at 18.4% CAGR to 2034 as the fastest-growing fuel type category. Battery Electric Vehicles comprise 0.8% market share with limitations on their charging infrastructure and expensive purchase cost.

Mid-Range Vehicles within the range of ZAR 300,000-550,000 constitute the largest market share segment at 44%. It includes those cars in which money matters most in the purchasing decision process in the South African new vehicle market. Entry-Level Vehicles costing less than ZAR 300,000 hold 28% market share in the country. Premium and Luxury Vehicles constitute a 28% market share in total.

South Africa’s passenger vehicle market features a relatively concentrated competitive structure with the top five producers accounting for about 62-68% of the total volume of passenger cars sold in the country due to their well-developed dealership network, brand reputation, and benefits associated with local production. Toyota South Africa has retained its dominant position within the South African passenger vehicle market with approximately 25-27% market share since the 1970s owing to its Hilux, Corolla Quest, and Fortuner line-up.

Volkswagen South Africa occupies second place with 16-18% market share owing to the successful launch of locally produced Polo and Polo Vivo. The most threatening competitive force within the industry comes from Chinese manufacturers that have managed to penetrate the South African passenger car market and challenge established market leaders through aggressive pricing strategies and improving quality perceptions.

April 2026: Toyota SA announced investment worth ZAR 4.2 billion into the Prospection manufacturing facility for increasing production volume of the Corolla Cross as well as launching a new hybrid model range in local and regional export markets.

March 2026: Volkswagen SA received approval from regulators for the launch of its newly developed Polo model with a standard 48-volt mild hybrid powertrain system, slated to start local assembly in Q3 2026 at its Uitenhage plant.

February 2026: Expansion plans for BYD South Africa saw an increase from 18 to 45 dealerships throughout South Africa by December 2026, targeting ZAR 850 million in annual sales through its EV product lineup.

January 2026: According to NAAMSA, the total number of new vehicles sold in 2025 was 327,200, representing a 4.8% increase from 2024 and the strongest annual performance since 2019.

December 2025: The Department of Trade, Industry, and Competition gazette new regulations for APDP Phase 2, extending production incentives through 2035 while introducing new EV-related incentive categories.

List of Key Players in South African Passenger Vehicle Market

South African Passenger Vehicle Market Segments

By Vehicle Type:

By Fuel Type:

By Price Segment:

By Sales Channel:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

15 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.