Share this link via:

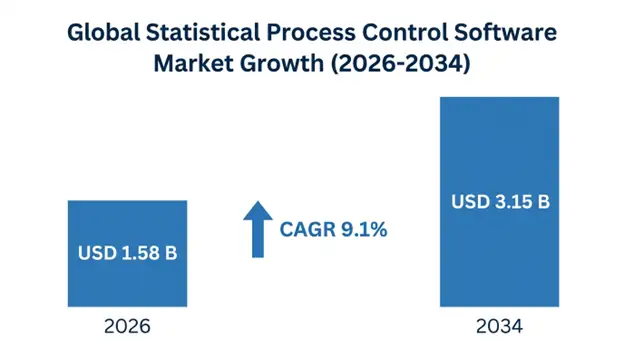

The global statistical process control software market size was valued at USD 1.44 billion in 2025 and is projected to reach USD 1.58 billion in 2026, expanding to USD 3.15 billion by 2034, growing at a CAGR of 9.1% during the forecast period (2026-2034).

An advanced form of quality management technology, statistical process control software relies on advanced statistical methods and real-time data analytics to monitor, control, and optimize manufacturing and business processes in various industries. These platforms use basic statistical concepts such as control charts, process capability indices, and rules of thumb based on probability to sort out common cause variation typical of all processes and special cause variation that suggests abnormal conditions that must be investigated and corrected. SPC software incorporates statistical rigor into its automated monitoring capabilities, allowing organizations to identify process drift before it leads to nonconforming products, systematically reduce process variation and maintain consistent quality across operations worldwide.

Today's statistical process control (SPC) platforms have matured beyond paper-based control charting to become full-fledged digital systems that communicate with sensors of the Industrial Internet of Things, Manufacturing Execution Systems, Enterprise Resource Planning platforms and Supervisory Control and Data Acquisition networks. This integration allows for the real-time collection of data from production lines, laboratory instruments, and quality inspection stations, with the ability to process up to millions of data points per second, and utilize advanced statistical algorithms such as multivariate analysis, machine learning data analysis and enhanced anomaly detection, and predictive quality models to detect potential process degradation before it reaches out-of-control conditions.

The impact of SPC software is not limited to quality assurance but can also be found in full operational excellence systems that utilize process stability information to shape product designs, supplier qualification processes, equipment maintenance schedules and continuous improvement efforts. Organizations with well-developed statistical process control programs routinely see a 45-65% reduction in defect rates, an average 4-7% improvement in manufacturing costs, a 60% or more reduction in customer complaints, and an improvement in regulatory compliance, which reduces inspection findings and enforcement actions. Measurable outcomes equate directly to the competition through customer satisfaction, warranty savings, faster new product introduction schedules and stronger regulatory compliance posture.

The addressable market includes discrete manufacturing industries and process manufacturing industries gaining strict quality requirements from regulatory agencies, original equipment manufacturers, and end customers who are setting a performance level of near zero defect. Numerous industries such as pharmaceutical manufacturing, semiconductor manufacturing, automotive component manufacturing, aerospace assembly and medical device manufacturing have regulations that mandate a documented statistical process control program, and this requirement continues irrespective of the economic cycle or budget constraint environment.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 1.44 Billion |

| Forecast Value | USD 3.15 Billion |

| CAGR | 9.1% |

| Forecast Period | 2026–2034 |

| Historical Data | 2022–2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Hexagon AB (Q-DAS), Advantive (InfinityQS), Minitab LLC, Siemens AG, Dassault Systèmes, Rockwell Automation, SAP SE |

Get more details on this report - Request Free Sample

The growing maturity of Industry 4.0 principles and smart manufacturing architectures, which fundamentally change the ways in which process information is gathered, analyzed and utilized in industrial settings, is the major structural trend driving the growth of statistical process control software. Convergence of Industrial Internet of Things connectivity, edge computing, advanced analytics platforms, and cloud infrastructure has opened really remarkable new possibilities for deploying statistical process control at scale and speed that would not have been possible under the old manual data gathering paradigm from periodic sampling exercises to real-time process surveillance , where there is little distinction between samples and the overall population.

In smart factory environments, data is pulled at the machine level, often in terabytes per day, coming from linked sensors, automated measuring systems, or other connected production equipment, and that is where the chance (and the need) appears for software platforms that can use statistical process control approaches at near machine speed. Those older manual workflows where an operator is basically comparing samples to rules, and then tuning the process based on what the pattern looks like on the control chart, just don’t really match today’s production reality. The reason is simple, because machines here can produce thousands of parts that don’t meet the required specs before the operator even has time to react and adjust things.

In 2025, the global manufacturing Industrial IoT market stood at USD 89.7 billion, and Statistical process control (SPC) software was a vital analytical layer in the larger manufacturing intelligence architecture. Employing a statistical process control system built into an integrated smart manufacturing platform results in a 62% reduction in the number of defects escaping, when compared to facilities employing manual or semi-automated quality monitoring approaches, and provides strong ROI rationale in operating environments with limited capital.

Key Performance Metrics:

Regulatory compliance mandates are a very strong non-discretionary driver for statistical process control software, especially in industries where documented process control programs are legally required (such as the pharmaceutical, medical device, automotive supply chain and aerospace component manufacturing sectors). The FDA, EMA, and other regulatory agencies around the world enforce CGMP requirements that mandate statistical process monitoring, batch release and continuous process verification throughout the entire product life cycle.

The FDA guidance framework for PAT and the International Council for Harmonisation (ICH) Q8, Q9, and Q10 guidelines make the following sets of expectations for science-based, risk-informed approaches to manufacturing, with statistical process control as the backbone of the manufacturing infrastructure that supports validation and establishes and maintain validated states of manufacturing control. Warning letters, consent decrees, and import alerts are issued during regulatory inspections for inadequate statistical process monitoring, which can stop production and result in the average cost of USD 18-52 million per enforcement.

International Automotive Task Force (IATF) 16949 certification requirements are part of automotive industry quality standards and require statistical process control (SPC) implementation in manufacturing processes that contain safety-critical characteristics, leading to compliance-based automotive industry procurements spread across global automotive supply chains with more than 95,000 tier-one and tier-two suppliers. Documented process monitoring using statistical methods is also required by Aerospace quality management standards AS9100 and Federal Aviation Administration production approval requirements, bringing the use of statistical process control software into aerospace manufacturing ecosystems.

Regulatory Compliance Performance Indicators:

As customer expectations for higher quality at stable or lower prices grow, input costs fluctuate, and competitive pressures expand, manufacturers across industries are placing greater emphasis on the cost of poor quality metrics that are becoming more visible on the profit and loss statement and on the radar of executives, such as scrap costs, rework costs, line downtime, warranty costs, returns, and brand damage. Organizations can benefit from statistical process control software, especially those with intricate, multi-step processes and high material costs such as automotive, semiconductors, aerospace, specialty chemicals, and high-value electronics, which are particularly vulnerable to hidden quality-related losses.

By reducing variability at critical process steps to improve yield and reduce over-processing, Statistical Process Control (SPC) software helps cost reduction and margin protection programs succeed by limiting the amount of suspect output when processes shift, shortening the time required to detect and respond, quantifying the impact of the improvement programs with metrics to prioritize programs with the highest potential for return on investment, and allowing for systematic tracking of improvement programs with before/after capability validation. Statistically valid data, capability studies, and control charts provided on a consistent basis throughout the organization are crucial to structured improvement processes, such as Lean, Six Sigma, and Operational Excellence, which are used by organizations to ensure they are committed to continuous improvement.

Cost Impact Metrics:

The most notable obstacle to the use of statistical process control software is the significant organizational change initiatives that must accompany the implementation of the technology; success with the software is far more likely to be related to workforce capability development, cultural change management and process redesign activities than technology configuration. For the successful implementation of a statistical process control system, statistically literate workforces are needed that can interpret the signals on control charts, understand the results from a capability analysis and can make decisions based on statistical evidence rather than intuition or experience.

Manufacturing skills gap is a recurring challenge in the adoption process and surveys have shown that less than 26% of the production floor staff on small and medium-sized enterprises have enough statistical knowledge to be able to use statistical process control software without significant training investment. Resistance from quality professionals and experienced operators can be a common hurdle in implementation projects, often mistaking statistical process control as a bureaucratic task instead of an enabling one for them to keep their projects moving, thereby extending project timelines and minimizing value derived from software investments.

The cost of full enterprise software deployments can be 4–6 times the software purchase cost, so the financial hurdles can be significant, especially for small and medium businesses that are constrained in their quality improvement budgets. Longer payback to measurable ROI, as financial benefits are not typically realized in organizations emphasizing short-term financial performance until 15-30 months after implementation of a statistical process control program, continues to create difficulties in building business cases.

Many manufacturing facilities have distributed technology environments that are integrated with a mix of modern, automated measurement systems, legacy manual data collection systems, older programmable logic controllers (PLCs) that don't communicate with the network, and enterprise software that communicates in proprietary data formats that are not supported by current statistical process control software architecture. Data integration complexity poses challenges to implementation as costs and effort associated with setting up reliable and clean data feeds into statistical process control platforms are higher than expected, and deployments are delayed, resulting in less value from the analysis because of incomplete or inconsistent data.

The ability to combine artificial intelligence and machine learning with the fundamentals of statistical process control to allow predictive quality management systems that predict deterioration before the process becomes out-of-control, suggest optimal process parameter adjustments to keep the process in capability, and automatically take corrective action in closed-loop processes represents a transformative market opportunity. The traditional statistical process control approach looks at process data collected over time and identifies process shifts after they have happened by interpreting the data using rules on control charts; the AI-driven approach examines patterns in the process data collected over time, and flags potential shifts hours or days before they occur.

By using multivariate process data streams and machine learning algorithms, complex patterns of interaction between dozens of process variables that cannot be captured by traditional univariate statistical process control methods can be detected, allowing for earlier intervention and more accurate root cause identification in complex manufacturing processes. In some application areas, such as semiconductor manufacturing, pharmaceutical continuous manufacturing, and chemical processing, multivariate process complexity is beyond the analytical capability of conventional statistical process control approaches, particularly those of high value.

With the combination of statistical process control and AI, software vendors can offer platform differentiation opportunities by providing a mix of mathematical rigor and regulatory acceptance of proven statistical methods with pattern recognition and predictive capabilities of modern machine learning, by meeting customer needs for a single platform to handle compliance documentation and for operation performance optimization.

Although cloud computing and subscription pricing are effective solutions for reducing upfront software investment barriers, they are still not widely adopted in SMEs with limited budgets and small information technology infrastructures, thus creating a market expansion opportunity for deployable subscription models. By eliminating the need for server infrastructure, software-as-a-service brings implementation from months to weeks and transforms one-off hefty up-front capital spending into reasonable monthly operational cost linked to the volume of manufacturing.

There is a significant opportunity for the small and medium enterprise manufacturing sector, which is expected to make up 71% of manufacturing facilities around the world but only 28% of the statistical process control software revenue in 2025, which can be addressed by cloud-based platforms that are easy to deploy and are priced at levels that can be accommodated in typical quality management operational budgets without the need for dedicated information technology staff.

The statistical process control software industry is going through a paradigm shift in architecture with vendors shifting away from legacy on-premises client-server systems to cloud-based systems with elastic scalability, global access, and continuous feature delivery via modern DevOps practices. Cloud-native statistical process control platforms offer the ability to deploy process control analytics across an enterprise, whereby manufacturing plant performance data from locations in various continents can be brought together in a single analytical environment, for cross-facility process comparisons and for identifying quality trends across the entire enterprise that are impossible with site-isolated legacy systems.

Cloud-based statistical process control platforms with built-in real-time streaming analytics can continuously stream data from automated measurement systems and process the data in real-time at measurement rates measured in milliseconds, instead of minutes or hours as batch processing legacy systems would do. This capability is especially beneficial in high-speed manufacturing settings such as the semiconductor, electronics, and pharmaceutical continuous manufacturing segments where process dynamics necessitate monitoring frequencies that are not traditionally used in the implementation of statistical process control.

Current efforts to integrate statistical process control software into digital twin platforms offer opportunities to optimize the process virtually through statistical models that can be calibrated using actual manufacturing data to simulate changes of process parameters, capability improvement interventions and control strategy modifications before they are executed physically. By integrating a digital twin, quality engineers can assess the statistical impact of the proposed process changes through Monte Carlo simulation, design of experiments analysis, and capability projection modeling, without causing any disruption in production or costs for material tests.

AI and machine learning algorithms are becoming more widespread, with advanced statistical process control platforms now using tools that go beyond the standard statistical chart rules to detect complex multivariate relationships, to predict process deterioration before statistical limits are violated, and to automatically suggest and/or initiate corrective actions. These systems are dynamically designed to learn from their past process behavior to set control limits that fit the current process conditions but remain statistically valid for regulatory requirements.

North America dominates the market, with the largest market value of USD 531.2 million in 2025 and expected to register a CAGR of 8.8% through 2034. Regional dominance is driven by the concentration of technology innovation with major SPC software vendors located in the United States, advanced manufacturing quality cultures that are focused on data-driven decisions, stringent regulatory requirements that set an absolute requirement for compliance, and high levels of technology adoption with sophisticated information technology infrastructure.

The U.S. accounts for 82% of the market value and has a strong focus on pharmaceutical, aerospace, semiconductors and automotive manufacturing industries, which have the strictest quality requirements and the highest levels of statistical process control software investment. Food and Drug Administration Process Analytical Technology requirements, IATF 16949 automotive quality system requirements and the AS9100 aerospace standards all establish the need for statistical process control program maintenance for hundreds of thousands of manufacturing facilities; this need is not dependent on economic cycles.

Well-developed ecosystems of statistical process control software vendors, implementation consultants, training organizations, and industry associations are strengths of the regional market and ease the path to realizing successful implementation and adoption rates. There are workforce development infrastructure mechanisms to support statistical literacy in using software effectively, provided by the American Society for Quality, the American Statistical Association and industry-specific quality organizations.

Key Regional Performance Indicators:

Asia Pacific was the fastest-growing region, projected to grow at a CAGR of 10.7%, reaching USD 387.4 million in 2025. The world's largest manufacturing base aiming for quality improvements to access premium export markets, the fast growth of the pharmaceutical and medical device manufacturing industry with the need for regulatory compliant quality systems, China, Japan, South Korea and India government-led initiatives to deliver manufacturing excellence, and increasing acceptance of international quality management certification leading to the procurement of statistical process control software are leading the way towards regional expansion.

In the region, China has the largest market share at 42%, owing to industrial policy initiatives under the Made in China 2025 program, efforts to modernize the regulation of the pharmaceutical industry to meet international Good Manufacturing Practice standards and the automotive industry's growth mandate, which calls for IATF 16949 certification for its domestic supply chains. The government pays attention to the transition from volume to quality competitiveness of manufacturing, which supports the adoption of quality management technology.

Japan has established extremely sophisticated statistical process control traditions that are founded on the principles of the post-war quality revolution and are based on a combination of traditional Japanese methods of quality management and new digital tools in advanced analytical platforms, which continue to be invested in. Among the most competitive industries worldwide that have high standards for quality workmanship and production control, South Korea's semiconductor and electronic manufacturing industries invest the most per facility in statistical process control software.

Regional Growth Metrics:

Software licenses and subscriptions dominate with 68% market share valued at USD 979.2 million in 2025, growing at 9.4% CAGR through 2034. This segment encompasses standalone statistical process control applications, integrated quality management suite modules, cloud-based subscription platforms, and embedded analytical components within manufacturing execution and enterprise resource planning systems. The transition from perpetual licensing to subscription models has increased revenue predictability for vendors while reducing initial investment barriers for customers, particularly benefiting small and medium enterprises seeking enterprise-grade analytical capabilities.

Software licenses and subscriptions dominate the market with a 68% market share worth USD 979.2 million in 2025, and it’s set to grow 9.4% CAGR through 2034. In practice this chunk includes standalone statistical process control tools, plus modules inside broader quality management suites, also cloud-based subscription platforms, and embedded analytical components that sit within manufacturing execution systems or enterprise resource planning environments. The shift from perpetual licensing to subscription models gives vendors steadier revenue expectations, while for customers it usually means lower upfront spending, which helps especially small and medium enterprises that want enterprise-grade.

Professional services sit at about 32% market share, reaching USD 460.8 million in 2025, and they cover implementation consulting, systems integration, workforce training, validation services across regulated industries, plus ongoing technical support. This segment remains resilient because enterprise statistical process control deployments require significant implementation support that need customization, data integration, and organizational change management help that plain software products alone just cannot handle well. Also, validation services for pharmaceutical and medical device manufacturers are especially high value.

Cloud-based deployment is the fastest-growing segment of the market, at 59% market share worth USD 849.6 million in 2025, and it’s projected to keep a 11.2% CAGR through 2034. Cloud deployment growth is tied to a bunch of things, like digital transformation efforts across manufacturing, the way subscription models improve accessibility, plus the practical gains from deploying across multiple sites, and the usual advantage of ongoing feature improvements without forcing disruptive upgrade projects each time. Also, security enhancements and validated cloud infrastructure choices for regulated industries have helped remove earlier sticking points for cloud adoption in areas like pharmaceutical and aerospace.

On-premises deployment still holds 31% market share, valued at USD 446.4 million in 2025. It supports organizations that care about data sovereignty, work in air-gapped manufacturing settings, depend on legacy system integrations, or need regulatory validation with fixed software configurations that are not meant to shift. Then there’s hybrid deployment at 10% market share, which is for enterprises wanting on-premises data processing for real-time control use cases, while also using cloud-based analytics for corporate reporting, and for managing performance across multiple sites.

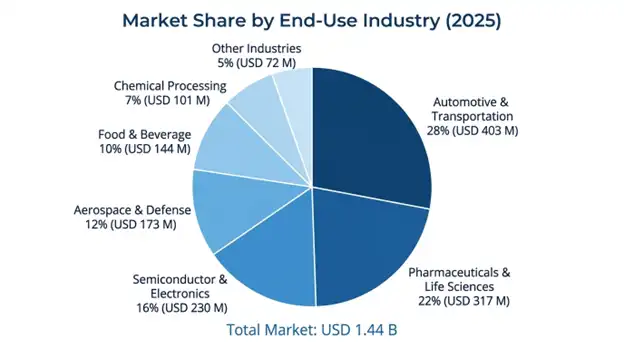

The Automotive & Transportation vertical leads all other segments with a market share of 28% and revenue of USD 403.2 million in 2025 thanks to IATF 16949 regulations and very high standards of quality set by automotive OEMs through supply chain quality agreements. Complex multi-tiered supply chain and high-quality standards of safety-critical components drive demand for consistent SPCs across hundreds of suppliers manufacturing plants globally.

Pharmaceuticals & Life Sciences vertical has witnessed fastest growth in 2017-2034 with CAGR of 11.8%, backed by regulatory compliances and significant economic impact of process failure in pharmaceutical drug manufacturing. This segment has witnessed steady growth due to the adoption of continuous process manufacturing, increase in biological drugs manufacturing, and advanced process monitoring required for personal medicines.

The semiconductor and electronics segment accounts for 16% market share and is characterized by disproportionately high spending in software investment per unit due to very high complexities involved in semiconductor wafer manufacturing, in which nano scale differences affect yield performance.

The statistical process control software market has been characterized by some degree of concentration where the top firms command an estimated 57-64% of the market in terms of value with advanced statistical and analytics solutions, industry vertical specialization, proven regulatory compliance track record, as well as extensive deployment experience. The competitive advantage is based on advanced analytical capabilities and comprehensive statistics, integration with manufacturing execution systems and ERP solutions, regulatory compliance capabilities in the specific industries served, intuitive user experience design that allows adoption by quality experts without strong statistics background, and scalable cloud-based technology.

The competitive landscape includes advanced statistical software providers competing against quality management solution providers with deeper manufacturing integration, while companies active in industrial automation increasingly integrate their SPC capabilities in broader manufacturing intelligence solutions. New entrants in the form of artificial intelligence native quality analytics startups compete against established vendors with better predictive capabilities but no regulatory compliance credentials and deployment experience.

Their strategic initiatives typically include adopting artificial intelligence and machine learning through organic growth or through an acquisition, or both, along with transitioning toward cloud-native platforms, mostly since SaaS demand keeps going up and it’s like the market just pushes there. After that they often go vertically into industries that carry regulations, and they fold in compliance specific capabilities, so it’s not just compliance, it’s kind of engineered compliance, if that makes sense. Companies are also collaborating with manufacturing execution system vendors and ERP vendors, to get improved integration

April 2026: Hexagon AB (Q-DAS) released a new generation of its statistical process control software with built-in machine learning for predictive quality assurance that allows companies to forecast process breakdowns 6–24 hours before control charts indicate a violation.

March 2026: Advantive (InfinityQS) signed a strategic agreement with a top cloud computing provider to offer industry-specific statistical process control software such as pharmaceutical, automotive, and aerospace with ready-made validation documents included.

February 2026: Minitab LLC has introduced the multivariate analysis feature to its family of statistical process control solutions with principal component analysis and partial least squares regression tools for analyzing continuous manufacturing processes in the pharma and chemical sectors.

January 2026: Siemens AG added statistical process control features to its Opcenter production control software eliminating the need for separate installations for Siemens automation system customers.

December 2025: Dassault Systèmes acquired a quality data analytics firm for USD 210 million and integrated its AI-based process monitoring technologies into its DELMIA manufacturing operations control system.

November 2025: SAP SE partnered with a statistical process control software vendor to add sophisticated analytics tools to SAP Digital Manufacturing Cloud software.

List of Key Players in Global Statistical Process Control Software Market

Global Statistical Process Control Software Market Segments

By Component:

By Deployment Mode:

By Organization Size:

By Functionality:

By End-Use Industry:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

16 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.