Share this link via:

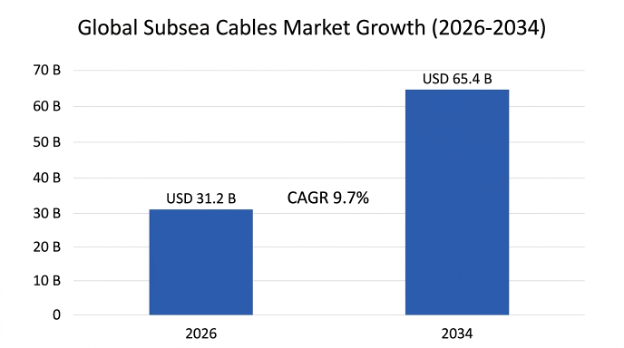

The global subsea cables market was valued at USD 28.5 billion in 2025 and is projected to reach USD 31.2 billion in 2026, expanding to USD 65.4 billion by 2034, growing at a CAGR of 9.7% during the forecast period (2026–2034).

Subsea cables are important physical infrastructure that supports the global digital economy as well as international power transmission, acting as the unseen network that allows over 99% of trans-ocean Internet traffic flows as well as the integration of offshore renewable power into domestic electrical grid networks. Subsea cable systems can be grouped into two main types: optical fiber telecommunication cables used to transport the Internet traffic across the seabed; and high voltage cables carrying the electricity from offshore power generating stations to the shore power distribution networks.

Contemporary optical fiber submarine cables are designed as multi-fiber optic systems enclosed in steel-armored, water-blocked sheaths capable of operating for 25-30 years at extremely high hydrostatic pressure up to 1000 atmospheres, temperature changes, seismic activity, and possible mechanical damages from marine works. Coherent transmission and Dense Wavelength Multiplexing technologies are utilized to deliver total capacity more than 400 terabits per second in major oceanic routes using Space Division Multiplexing technology to increase the number of fiber pairs in cables up to 16-32 fiber pairs rather than usual 6-8 fiber pairs.

Subsea power cables employ high-voltage direct current (HVDC) and alternating current (HVAC) to transport electricity over underwater paths that vary from short inter-array submarine cables used within offshore wind farms, to longer international submarine cables linking countries together over distances that can stretch into hundreds of kilometers. High-voltage direct current (HVDC) sub-sea cables can transmit electrical energy over long distances in an economical manner while maintaining low loss levels, while unique dynamic cables allow for constant movement of offshore wind platforms.

Due to the importance and necessity of submarine cable networks in today’s world, submarine cables have evolved from simple communication and electrical infrastructure assets to becoming critical national infrastructure that need protection, redundancy, and proper route selection. The combination of rapid increases in worldwide data traffic, increased installation of offshore wind facilities, and energy security awareness has seen massive investments being made by the submarine cable industry.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 28.5 Billion |

| Forecast Value | USD 65.4 Billion |

| CAGR | 9.7% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Europe |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Type, Voltage, Application, Installation Depth, Component, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Norway, Denmark, Netherlands, China, Japan, India, Australia, South Korea, Singapore, Brazil, UAE, Saudi Arabia |

| Key Market Playes | Prysmian Group, Nexans SA, Alcatel Submarine Networks, SubCom LLC, NEC Corporation, Sumitomo Electric, NKT A/S, HMN Technologies |

Get more details on this report - Request Free Sample

The most significant structural driver of the subsea cable market is the rapid global expansion of offshore wind energy development of offshore wind energy development, which, in turn, requires extensive subsea cable infrastructure , including inter-array cables that link individual turbines, export cables that carry the combined power to onshore grids, and international interconnectors that allow cross-border renewable energy trading and real-time grid balancing. Offshore wind capacity hit around 280 GW in 2025, and development targets continue to expand, with goals getting close to 2,000 GW by 2040 in net-zero scenario thinking, requiring the installation of approximately 180,000 to 220,000 kilometers of new subsea power cable. That amount of installation translates into roughly USD 85-120 billion for cable procurement.

European offshore wind farm construction is driving global cable demand, accounting for more than USD 45 billion worth of subsea cable investments in the North Sea alone between now and 2034. Europe's offshore renewable energy strategy aiming at generating 300 gigawatts of offshore wind energy by 2050 demands not only cable connections for each offshore wind farm but also offshore grid connections that link all these energy sources and allow for energy exchange between various nations within Europe. This can be seen in some major cable interconnection projects like NordLink and North Sea Link.

Technological advancements in high-voltage HVDC lines with voltages of up to 525 kV and higher make it possible to deliver multi-gigawatt power through one line, decreasing the size of its installation on the seabed and installation expenses per transmitted unit of power. Technical advances toward cables suitable for floating wind projects allow harnessing huge areas of the deep sea that had not been available before due to a lack of technological capabilities.

The telecommunication segment is experiencing transformative growth due to the exponential growth in internet traffic, adoption of cloud computing technologies, and strategic move by hyperscale technology firms to own capacity on transoceanic cables as they seek to have control over the capacity, performance, and route diversity of their global cloud computing services. International bandwidth capacity increased from 850 Tbps in 2020 to 2,400 Tbps in 2025 and is estimated to reach 8,500 Tbps in 2030.

Large-scale technology firms like Google, Meta, Microsoft, and Amazon have revolutionized the subsea communications market by financing about 68% of all new transoceanic cable system construction in 2025 by switching from carrier-led consortiums to privately-owned cables, thus giving them full control over key digital infrastructure. Next-generation cable systems will have aggregate capacities of more than 400 Tbps using Space Division Multiplexing allowing for 16-32 fiber pairs in a single cable, compared to the typical 6-8 fiber pairs in current generation cables.

The geographical spread of cloud computing services to developing countries is fueling investments in the construction of more cable routes that will link previously under-served regions like Africa, Southeast Asia, and Latin America to the rest of the world’s internet. The number of internet users in Africa increased from 570 million to 780 million between 2020 and 2025 between 2020 and 2025, which means there needs to be additional bandwidth capacity.

The increasing acknowledgment that sub-sea cables represent a vital part of the nation’s infrastructure necessary for maintaining continuity, energy security, and secure defense communications is resulting in increased investments above mere minimum capacity needs with governments and operators focusing on redundancy, security, and diversification of routes to minimize the possibility of damage arising from either accident, environmental factors, or malicious acts. The high value of subsea infrastructure has thus made cables more than simple utilities and into geographically strategic entities.

Multiple cable systems which are physically different are being put in place on strategic intercontinental paths such that continuity can be guaranteed even when an individual cable system or a landing point is affected, whereas alternate routes are preferred, irrespective of the additional cost involved, where there may be geopolitics or high traffic areas. In addition, the current global health situation brought by the COVID-19 pandemic has made it clear just how important good digital infrastructure is.

The issues surrounding geopolitical conflicts have also made it clear to the world how important the diversification of the supply chain away from one source is in protecting the vulnerable subsea cables. For the power sector, subsea interconnectors are considered critical infrastructures which directly tie into issues of energy security and decarbonization targets, and hence regulatory support is available for long-term investments and coordination between nations.

The most critical constraint restricting the growth of the subsea cable market is this serious shortage of specialized cable lay vessels, that can handle large diameter, heavy gauge power cables, which offshore wind export systems and HVDC interconnectors keep needing. In practice global fleet capacity turns into a kind of hard bottleneck, and it tends to drag project timelines by something like 12-24 months, while also letting installation contractors ask for big price premiums, so overall project costs jump around 15-25%. If you look at the numbers, the global stock of heavy lift cable lay vessels that match large power cable installations is roughly 40 vessels in 2025, and utilization rates are already above 95%, which then creates booking lead times in the range of 18-30 months.

Building new cable lay vessels is a lengthy process taking 3-4 years from order to delivery and costing between USD 250-500 million per vessel due to capacity issues at the yards producing these ships. The specialization required in the installation process demands skilled marine engineers, cable joiners, and ROV specialists with several years of experience, limiting workforce capacity as well and affecting the capability to expand the installation contractor’s operation fast.

Advanced technology and equipment involved in the cable lay process make this work especially difficult to do for HVDC cables, particularly dynamic cables for floating offshore wind installations, meaning that only certain cable lay vessels can carry out this task, which limits capacity even more and results in higher prices.

The newly emerging floating offshore wind industry presents a revolutionary market opportunity in need of special dynamic sub-sea cables that can endure perpetual mechanical stress resulting from wave-induced movement of the platforms over a 25-year period at a depth range of 60-1,000 meters in environments where conventional bottom-fixed structures cannot be installed. As of 2025, global floating offshore wind pipelines are expected to surpass 250 GW, whereas commercial operation is expected to be achieved between 5-15 GW in 2030.

Dynamic cable innovation calls for breakthroughs in conductor construction, insulation systems, and mechanical protection capable of withstanding dynamic bending, varying tension, and thermal stress due to operation in harsh marine environments. Despite being barriers to entry, these factors offer pricing advantages to manufacturers successfully producing reliable solutions for dynamic cables, which command premiums 2-3 times those for fixed-bottom operations due to their technical complexity and low number of suppliers.

The emergence of floating wind technology will open access to extensive deep-water zones with excellent wind energy, making possible up to 4-5-fold growth of the offshore wind market and generating demand for cables that can serve such installations.

The telecommunications sector is undergoing a major technological transformation through the implementation of Space Division Multiplexing technology, which allows for the development of cable systems supporting up to 16-32 fiber pairs against conventional 6-8 pairs and improves overall capacity significantly while improving power efficiency through the use of shared optical pumping systems across fiber pairs. This revolution in the technological front helps overcome previous limitations to sub-sea cable capacity due to electrical power limitations from the feeder equipment at shore-end locations.

SDM technology necessitates advancements in the wet plant, such as improvements in repeaters, advanced branching units, and high voltage power feeders that can accommodate dense fiber configurations spanning thousands of miles. This architectural evolution allows cable companies to realize economies of scale by having a higher capacity per cable while at the same time realizing redundancy and reliability in their networks using optimized power systems.

This change in technology is pushing cable manufacturers to seriously invest in advanced manufacturing facilities and new component developments since realization of SDM technology will become a key competitive advantage in gaining lucrative trans-oceanic contracts from hyperscale technology firms and telecommunications companies.

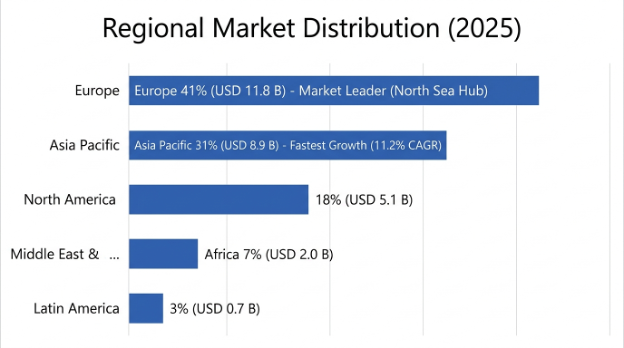

Europe has the largest market share at USD 11.8 billion in 2025 and is expected to witness an annual growth rate of 9.4% until 2034, given the fact that Europe has the most advanced offshore wind development program, detailed cross-border grid interconnection strategy, and established regulatory framework that facilitates project development and financing. North Sea is the region with the most intensive use of subsea cables in the world, where more than USD 45 billion in committed cable investment is expected to be dedicated to offshore wind export systems, inter-array networks and international interconnectors by 2034.

European demand is led by the United Kingdom, which has 50 GW of offshore wind in development that will need extensive export cable infrastructure, as well as ambitious interconnector projects such as Eastern Green Link projects between offshore wind generation in Scotland and generation demand in England. The UK's Contracts for Difference mechanism allows for revenue certainty, allowing long-term cable procurement contracts for 3–4-year manufacturing lead time.

The demand from continental European countries such as Germany, Netherlands, Denmark, and Norway is boosted by the offshore wind policies in individual nations and the European Commission’s plans for building a networked system to support inter-country transmission of renewable energy using the grid. The region is in close geographical proximity to cable production giants such as Prysmian, Nexans, and NKT.

Asia Pacific is the fastest-growing region, projected to grow at a CAGR of 11.2% during the forecast period to reach USD 8.9 billion in 2025, due to the massive expansion of transoceanic telecommunications infrastructure to support the world's largest internet user base, rapidly expanding offshore wind development in Taiwan, South Korea, Japan, and Vietnam, and significant island grid connection programs in Pacific archipelagos. It contains more than 60% of the world's population and has high growth rates in Internet penetration, resulting in high and growing demand for international bandwidth capacity.

China's investments in the region in the cable manufacturing sector have totaled more than USD 12 billion for the period 2018-2025, allowing the country to achieve full production capacities for optical fiber, power cables, and specialized marine cables, which are sold to domestic and export markets. Taiwan has an offshore wind procurement pipeline of 20GW, South Korea has a 12GW program and Japan has a 45GW floating offshore wind program all representing multi-decade cable procurement requirements for specialist deep water and dynamic cables.

Southeast Asia is a region of archipelagic states, where domestic connectivity demands for subsea fiber systems are naturally high, and emerging economies are some of the fastest internet users with increased investment in new cable systems for the Southeast Asian region, which are supplementing existing but congested cable landlines.

Type Insights

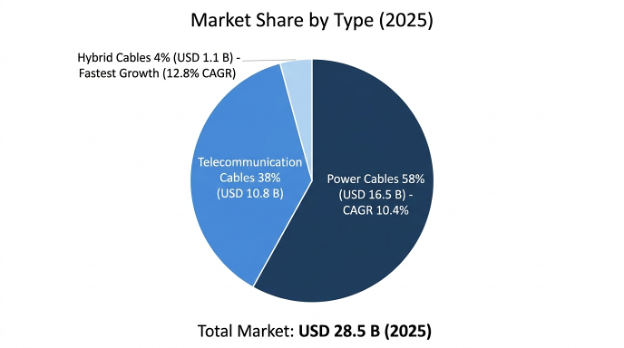

Power Cables take the lead with a market share of 58%, valued at USD 16.5 billion in 2025 and grew at a CAGR of 10.4% during 2025-2034 owing to massive expansion in offshore wind farms, interconnector installations between countries, and connecting islands with power grids. The market segment is supported by premium pricing based on material cost, technological complexity, and the manufacturing process needed with large-scale HVDC systems priced between USD 800,000 – 1,400,000 per km.

Telecommunication Cables hold a market share of 38%, valued at USD 10.8 billion in 2025 and grew at a CAGR of 8.6% till 2034 consisting of undersea fiber optic cables supporting global internet networks, local connectivity networks, and communication systems installed on offshore locations. The market segment will be supported by investments by hyperscale technology companies in addition to ongoing capacity increases through Space Division Multiplexing and coherent optical transmissions.

Hybrid Cables hold a market share of 4%, valued at USD 1.1 billion in 2025 and grew at a CAGR of 12.8% till 2034 due to growing installations of offshore wind farms using hybrid cables.

The Offshore Wind Energy segment is the largest application segment with 42% market share, valued at USD 12.0 billion in 2025, and is projected to grow at a CAGR of 11.1% during the forecast period 2025-2034, including inter-array cables connecting turbines, export cables transmitting power to shore, and offshore substation connections. The application has faster worldwide deployment, larger project scale and greater distances which require higher voltage systems.

Intercontinental Data Transmission holds a share of 31% market share at USD 8.8 billion in 2025, representing established transoceanic telecommunication routes that carry the global internet traffic. The application is poised for steady growth powered by expanding bandwidth demand and technology company infrastructure investment.

Grid Interconnection Market to Reach USD 5.1 billion by 2025 with a CAGR of 9.8% Grid interconnection market size is estimated to reach USD 5.1 billion by 2025. The market is projected to witness a CAGR of 9.8% during the forecast period. The market is driven by increasing cross-border power links to facilitate renewable energy trading and grid balancing across national boundaries.

Shallow water systems, which include 0-200 meters deep waters, represent 48% of total installation volume with superior prices due to higher requirements for protection in high-risk fishery zones and commercial marine traffic.

Deep water systems, covering water depth of 200-2000 meters, have 34% share in market valuation and are used for offshore power generation plants as well as inter-regional communication cables.

The subsea cable industry globally is a highly concentrated one, with six major companies accounting for a combined market share in the range of 75%-82% based on the ownership of advanced technology, custom manufacturing capacities, installation vessels, and maintenance skills, all acting as key entry barriers in this business segment.

Innovation in terms of cable capacity and performance efficiency, capabilities and readiness of a company’s fleet of installation vessels, offshore project management knowhow, and maintenance and repair of systems over a period of up to 25-40 years form the main basis for competitive differentiation in this market segment. Expansion of production capacity forms the focal point of investments for industry leaders, who have announced capital expenditures totaling USD 3.2 billion during the period of 2022-2026.

Since the manufacture of large power cables is highly specialized, the need to have plants designed for the continuous extrusion of high voltage insulations makes it very difficult to expand capacity due to the long construction periods (3-5 years) involved and the huge initial investments (USD400-800 million per plant). The ownership of installation vessels or their long-term lease is a crucial competitive advantage.

April 2026: Prysmian Group awarded USD 1.4 billion contract for Scotland to England Eastern Green Link 2 HVDC project, which involves 525 kV cable systems totaling 540 kilometers in connecting offshore wind generation in Scotland to the English transmission grid, set for completion in 2028-2030.

March 2026: Nexans S.A. has completed the commissioning of Halden, Norway factory, which increases the company's annual output of HVDC cables in North Sea application by 1,200 kilometers (28%).

February 2026: USD 600 million contract signed by SubCom LLC for transpacific cable system connecting United States, Japan, and Philippines awarded to technology company consortium that uses 350 Tbps capacity through advanced coherent optical transmission covering 14,000 kilometers.

January 2026: Sumitomo Electric unveiled a cable-lay vessel with a capacity of 10,000 tons specially built for large HVDC projects to cater to vessel limitations in Japanese and South-East Asian markets. The vessel is expected to enter commercial service in quarter three of 2026.

December 2025: Alcatel Submarine Networks recorded the achievement of 525 kV rating in extruded HVDC cables, which helped transmit 2,000 MW in single circuits.

By Type:

By Voltage:

By Application:

By Installation Depth:

By Component:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.