Share this link via:

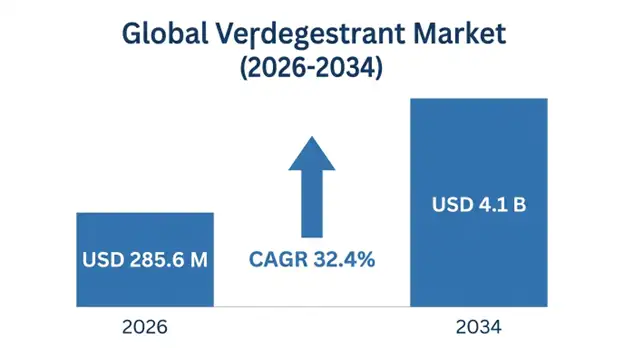

The global vepdegestrant market is projected to reach USD 285.6 million in 2026, expanding to USD 4.1 billion by 2034, growing at a CAGR of 32.4% during the forecast period (2026-2034). This exceptional growth trajectory reflects the compound’s positioning as a first-in-class oral Proteolysis TArgeting Chimera (PROTAC) designed to address critical unmet needs in hormone receptor-positive breast cancer treatment, particularly in patients who have developed resistance to conventional endocrine therapies.

Vepdegestrant represents a revolutionary advancement in targeted oncology therapeutics, using a mechanism that really does more than “just stop” estrogen receptor proteins. Instead of merely blocking receptor activity, it facilitates complete degradation of estrogen receptor proteins, resulting in complete receptor elimination rather than partial suppression. Traditional approaches, like selective estrogen receptor modulators (SERMs) such as tamoxifen, and selective estrogen receptor degraders SERDs such as fulvestrant, are often described as partial receptor suppression. In contrast, vepdegestrant works as a bifunctional small molecule that both latches onto the estrogen receptor and calls in E3 ubiquitin ligases. The target protein is subsequently degraded through the body’s own ubiquitin–proteasome system. Because this is a catalytic process, it may support longer lasting therapeutic activity even at lower drug levels while helping overcome common resistance mechanisms seen in hormone receptor-positive breast cancer.

Clinically, the “full degradation” aspect becomes especially clear for ESR1 mutations. These mutations occur in approximately 30–40% of patients after aromatase inhibitor therapy, and represent a major mechanism of acquired resistance why conventional endocrine treatments start to underperform. Variants like Y537S and D538G matter a lot here. They enable ligand independent receptor activation, so the receptor keeps signaling even when typical hormone-blocking strategies are used. As a result, therapeutic efficacy gradually declines over time. With its PROTAC mediated degradation process, vepdegestrant stays active against both wild type and mutant receptor forms, offering a mechanistically differentiated solution to endocrine resistance, which affects a substantial proportion of patients with advanced hormone receptor-positive disease.

The opportunity is built on the big global burden of estrogen receptor-positive, HER2-negative breast cancer, which accounts for about 70% of all breast cancer diagnoses worldwide. There are more than 2.3 million new breast cancer cases each year, and the hormone receptor-positive group includes approximately 1.6 million patients who will eventually need several lines of systemic therapy as the disease moves forward. Advanced breast cancer is chronic in practice, plus resistance tends to develop after first line CDK4/6 inhibitor combos, creating a large recurring patient population requiring sequential therapies. They need treatments that are mechanistically differentiated, potentially helping extend disease control and while maintaining patient quality of life. Oral administration and improved tolerability profiles also help support that advantage.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 285.6 Million |

| Forecast Value | USD 4.1 Billion |

| CAGR | 32.4% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Indication, Line of Therapy, Combination Regimen, Biomarker Status, Distribution Channel |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Arvinas Inc., Pfizer Inc. |

Get more details on this report - Request Free Sample

The rising global incidence of hormone receptor-positive breast cancer and the high prevalence of endocrine resistance in metastatic settings are the core reasons for the growth in the vepdegestrant market. Breast cancer is the most common cancer in the world and about 2.3 million new cases are diagnosed every year, of which about 1.6 million are hormone receptor-positive, HER2-negative. The disease course of this patient group is unique and characterized by initially responding to aromatase inhibitors, tamoxifen or CDK4/6 inhibitor combinations and then inevitably developing resistance to these standard endocrine therapies, through multiple acquired molecular resistance pathways.

In the majority of patients who have previously been treated with an aromatase inhibitor, the most significant acquired resistance mechanism is ESR1 mutations, which are observed in 30-40% of these patients. These mutations are more common in patients who have had treatment with CDK4/6 inhibitors in combination with an aromatase inhibitor (AI), a combination therapy that is now the standard first-line treatment for metastatic hormone receptor-positive breast cancer. The increasing patient population moving into the CDK4/6 era will result in an expanding population of patients with ESR1 mutations who will require mechanistically distinct second-line therapies that can block ligand-independent receptor activation.

In addition to ESR1 mutations, other mechanisms of resistance such as activation of the PI3K pathway, amplification of the cyclin D1 gene and alterations in the regulatory proteins of CDK4/6 form complex resistance patterns, necessitating combination therapeutic approaches. Due to the chronic progressive nature of hormone receptor-positive breast cancer, multiple sequential lines of treatment are required and may extend beyond seven years in certain cases, and each progression of disease will need therapeutic interventions that would be able to prolong disease control and maintain high quality of life with tolerable side effect profiles.

Key Performance Metrics:

The broader validation of Proteolysis-Targeting Chimera (PROTAC) technology as a clinically viable drug discovery platform is a key driver in the vepdegestant market as successful clinical development will prove to be the proof of concept for targeted protein degradation as a new therapeutic modality in cancer research and therapy, with potential applications across a broad range of therapeutic targets. The PROTAC mechanisms have basic pharmacological benefits over small molecule inhibitors, because they can target proteins previously considered undruggable because of the absence of a defined binding site, including the ability to catalyze a reaction, which means that sub-stoichiometric concentrations of PROTAC molecules can completely eliminate target proteins, and the potential for overcoming resistance mechanisms due to mutations in the target protein that affect target binding.

The clinical development of Vepdegestrant has generated important validation of the mechanism of action of PROTAC technology to achieve superior target engagement compared to conventional receptor modulation, as demonstrated by almost complete degradation of the estrogen receptor in human biopsy studies at clinically achievable concentrations. This mechanistic distinction equates to clinical benefits; vepdegestrant exhibited clinically significant activity in ESR1-mutant tumors, whereas established SERDs were significantly less effective, thus supporting the hypothesis that full receptor eradication is clinically beneficial beyond receptor inhibition in resistance models.

Investment into targeted protein degradation technology has also ramped up significantly, with several companies developing PROTACs for oncology and other programs in the works, such as those for androgen receptors in prostate cancer and BRD4 in hematological malignancies, and new developments for KRAS and other promising "undruggable" G protein-coupled receptors (GPCRs). This wider commitment from the industry will allow for the continued development of optimization of the linker, the use of E3 ligases and the enhancement of delivery, further improving the pharmacological characteristics of the next generation of degraders, as demonstrated clinically through vepdegestrant development programs.

Innovation Impact Metrics:

The broad global partnership, valued at more than USD 1.4 billion (inclusive of upfront payments and development milestones), between Arvinas and Pfizer provides vepdegestrant with commercial development resources, regulatory expertise and global market access capabilities that significantly drive the pathway towards commercial launch and reduce development and commercialization risks. Pfizer's existing oncology commercial infrastructure (relationships with oncology prescribers, advanced contracting skills with payers, global manufacturing capabilities) provide competitive advantages that smaller biotechnology firms may struggle to replicate in developing competing programs.

Through this partnership, there will be simultaneous development across multiple indications and combinations, with clinical trials planned to explore monotherapy in ESR1-mutant disease, combinations with CDK4/6 inhibitors in earlier lines of therapy, and potential use in an adjuvant setting for high-risk early-stage disease. This multi-program strategy maximizes the addressable market opportunity and provides a body of clinical evidence to support regulatory submissions in a variety of patient populations and treatment settings.

Partnership Performance Metrics:

The primary competitive challenge facing vepdegestrant is the already commercial elacestrant, an oral SERD approved in January 2023 by the FDA for the treatment of metastatic hormone receptor-positive breast cancer among patients with ESR1-mutant tumors. Because of the market leadership of elacestrant, prescribers are familiar with the medication, there are established reimbursement pathways, and patient access infrastructure is in place, vepdegestrant will need to show clinically meaningful differentiation in efficacy, tolerability, or convenience factors. However, oncologists familiar with elacestrant’s clinical profile with elacestrant's clinical profile may need strong evidence of better results to switch their practice to the new drug which works in a different way.

Oral SERD programs are in multiple advanced stages of development, such as camizestrant (AstraZeneca), giredestrant (Roche) and imlunestrant (Eli Lilly), and the therapeutic space is a crowded therapeutic landscape with multiple agents targeting for the same patient population. This competitive intensity can also drive down market share and lead to pricing pressure because the competitive nature of the market allows the payers to use it as leverage in negotiating their reimbursement terms, which may ultimately affect the premium pricing often expected from first-in-class mechanisms.

Competitive Challenge Metrics:

The fact that vepdegestrant is the first PROTAC therapeutic to enter clinical development provides regulatory agencies with new issues to address, as they need to establish regulatory frameworks for evaluating a new drug modality and class with different pharmacological properties. Specific PROTAC properties such as hook effects, ternary complex formation reaction rates and potential off-target protein degradation will need to be assessed using specialized analytical approaches and regulatory guidance as it evolves, which may result in additional data requirements beyond those typically seen in conventional drug applications.

Reimbursement challenges are related to premium pricing expectations for first-in-class PROTAC therapy, with expected annual treatment cost projections more than USD 180,000-240,000, with novel oncology mechanism precedents. The ability of payers to determine the value proposition for vepdegestrant depends on the availability of health economic evidence that supports the benefit of vepdegestant in the context of overall survival, quality of life and health care resource utilization, all of which are critical considerations for payers evaluating premium pricing.

Regulatory Challenge Metrics:

A significant market expansion opportunity exists in developing vepdegestrant not only for the current second-line ESR1-mutant indication, but also for earlier treatment lines, like first-line metastatic disease, in combination with CDK4/6 inhibitors. And beyond that, possibly adjuvant therapy for people at high risk with early-stage hormone receptor-positive breast cancer. This earlier-line expansion strategy is supported by strong scientific rationale, because if you get complete estrogen receptor degradation in treatment-naive tumors, it may prevent ESR1 mutations from showing up that may limit the duration of standard aromatase inhibitor-based therapies.

The clinical programs looking at vepdegestrant with CDK4/6 inhibitors for first-line metastatic disease, represent the most immediate expansion opportunity, since biology is basically attacking estrogen receptor signaling and cell cycle progression at the same time. If this works in this setting, it could expand the addressable market from about 650,000 second-line patients to the entire first-line metastatic population, roughly 1.1 million patients each year. This represents more than a doubling of the commercial opportunity, even with all the usual uncertainties.

For the longer term though, adjuvant therapy could be the highest volume play. About 800,000 patients every year are diagnosed with high-risk early-stage hormone receptor-positive breast cancer, and still around 20–30% end up having a recurrence even after standard adjuvant endocrine therapy. If an extended adjuvant approach with a mechanistically differentiated agent that achieves complete receptor elimination could reduce late recurrence rates, the potential patient pool is huge, something like 50 times larger than the current metastatic target, highlighting the substantial long-term commercial potential.

Expansion Opportunity Metrics:

The expanding clinical adoption of liquid biopsy tech, for catching circulating tumor DNA ESR1 mutations, is creating a significant precision medicine opportunity that significantly expands the clinically identifiable patient population that can be considered for vepdegestrant therapy. As liquid biopsy platforms become increasingly integrated into routine clinical practice, and reimbursement coverage keeps widening, the share of metastatic breast cancer patients getting ESR1 mutation testing is climbing, from about 34% in 2022 toward an expected 78% by 2028. That trend is expected to significantly expand the diagnosed ESR1-mutant patient population.

Using liquid biopsy to watch molecular changes while patients are on vepdegestrant helps identify emerging resistance mechanisms, so clinicians can fine tune therapy before the usual clinical decline shows up. In that sense, this approach places vepdegestrant inside a broader precision oncology framework, one that connects molecular diagnostics, targeted medicine, and near real-time monitoring. Together they aim to improve outcomes, while also creating added commercial momentum via companion diagnostic collaborations.

Biomarker Integration Metrics:

North America: Market Leadership Through Clinical Development Infrastructure and Oncology Access

North America represents the dominant regional market for vepdegestrant, mainly because the region is the primary clinical development hub, it has the highest concentration of breast cancer subspecialty know-how, and the reimbursement infrastructure is more mature for brand new oncology drugs. The United States looks like the main commercial launch place, with an estimated 280,000 women living with metastatic hormone receptor-positive, HER2-negative breast cancer who are actively receiving systemic therapy, including around 95,000-112,000 that harbor ESR1 mutations based on real world liquid biopsy registry data.

The FDA breakthrough therapy designation for vepdegestrant in ESR1-mutant metastatic breast cancer helps speed up review timelines, and it also allows more hands-on agency guidance during the development period, which reflects the view that this compound could help with serious conditions where existing treatment options remain inadequate. The regulatory track also supports rolling review submissions that could allow approval within about 6-8 months after the complete application is submitted, thereby accelerating potential market entry after the Phase III data readout.

Medicare and commercial payer frameworks for oral oncology medicines create reimbursement precedents that can shape how vepdegestrant is covered, since oral administration qualifies for Part D pharmacy benefit coverage, which tends to make patient access easier compared with intravenous therapies. And the existing reimbursement setup for ESR1 mutation testing means the patient identification pathways needed for vepdegestrant prescribing are already operational by the time of commercial launch.

Key Performance Indicators:

Asia Pacific: Fastest Growth Through Incidence Expansion and Access Improvement

Asia Pacific represents the fastest-growing regional market, primarily driven by rising breast cancer incidence, molecular diagnostic infrastructure is expanding fast enough to help identify ESR1 mutations, and healthcare system investments are significantly improving access to new oncology therapeutics across China, Japan, South Korea, and Australia. In 2025, regional breast cancer incidence hit around 820,000 new cases every year, which is about 36% of global incidence. Most cases, about 65-72%, fall under hormone receptor-positive subtypes. That makes a big, ongoing pool of patients who will need sequential therapies, because frontline therapies often lose efficacy over time.

China represents the largest regional opportunity, it has roughly 420,000 new breast cancer diagnoses annually and an oncology pharmaceutical market that is growing quickly, with 22.4% annual growth recorded between 2020 and 2025. Regulatory developments also support market expansion: the National Medical Products Administration has accelerated approval routes for innovative oncology drugs. Add in national reimbursement talks that have reduced prices for new agents, and you get a mix aimed at balancing innovation access with affordability considerations on one side, but also affordability imperatives on the other.

Japan and South Korea stand out for molecular diagnostic adoption. ESR1 liquid biopsy testing among metastatic breast cancer patients is already at 52% in Japan and 47% in South Korea during 2025. So, the patient populations are more precisely stratified, and they’re basically prepared for vepdegestrant therapy once regulatory approval arrives. Australia is a different but still important case, with efficient regulatory and reimbursement pathways for novel breast cancer therapeutics. Its demonstrated efficacy, especially within molecularly defined populations, establishes a regional precedent that can make broader Asia Pacific market entry easier.

Regional Growth Metrics:

List of Key Players in Global Vepdegestrant Market

1. Arvinas Inc.

2. Pfizer Inc.

3. AstraZeneca plc

4. F. Hoffmann-La Roche Ltd.

5. Eli Lilly and Company

6. Sanofi S.A.

7. Novartis AG

8. Merck & Co. Inc.

9. Gilead Sciences Inc.

10. Menarini Group

11. Daiichi Sankyo Company Limited

12. Johnson & Johnson Services Inc.

13. Bayer AG

14. Amgen Inc.

15. BeiGene Ltd.

Global Vepdegestrant Market Segments

By Indication:

• Advanced/Metastatic ER+/HER2- Breast Cancer

o ESR1-Mutated Metastatic Breast Cancer

o Endocrine-Resistant HR+ Breast Cancer

o Post-CDK4/6 Inhibitor Progression

• Early-Stage High-Risk Breast Cancer

o Adjuvant Therapy Candidates

o Neoadjuvant Therapy Candidates

o Recurrence Prevention Settings

By Line of Therapy:

• First-Line

o Combination with CDK4/6 Inhibitors

o Endocrine Therapy-Naïve Patients

• Second-Line

o ESR1-Mutated Resistant Disease

o Post-Aromatase Inhibitor Failure

• Third-Line & Beyond

o Heavily Pretreated Metastatic Patients

o Multi-Drug Resistant Disease

By Combination Regimen:

• Monotherapy

o ESR1-Mutated Patient Population

o Endocrine-Refractory Settings

• With CDK4/6 Inhibitors

o Palbociclib-based Combination

o Ribociclib-based Combination

o Abemaciclib-based Combination

• With PI3K/AKT/mTOR Pathway Inhibitors

o PI3K Inhibitor Combinations

o AKT Inhibitor Combinations

o mTOR Inhibitor Combinations

• With Other Targeted Agents

o Antibody-Drug Conjugates

o PARP Inhibitors

o Immuno-Oncology Agents

By Biomarker Status:

• ESR1-Mutated

o Y537S Mutation

o D538G Mutation

o Other ESR1 Alterations

• ESR1 Wild-Type

• PIK3CA-Mutated

• Other Genomic Subgroups

o HER2-low Expression

o BRCA1/2 Mutations

o AKT Pathway Alterations

By Distribution Channel:

• Hospital Pharmacies

• Specialty Oncology Clinics

• Retail Pharmacies

• Online Pharmacies

• Specialty Pharmacies

By End-User:

• Cancer Specialty Hospitals

• Oncology Clinics

• Academic & Research Institutes

• Ambulatory Infusion Centers

• Home-Based Oral Oncology Care Settings

By Route of Administration:

• Oral Tablets

• Combination Oral Regimens

By Region:

• North America

• Europe

• Asia Pacific

• Middle East & Africa

• Latin America

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

13 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.