Share this link via:

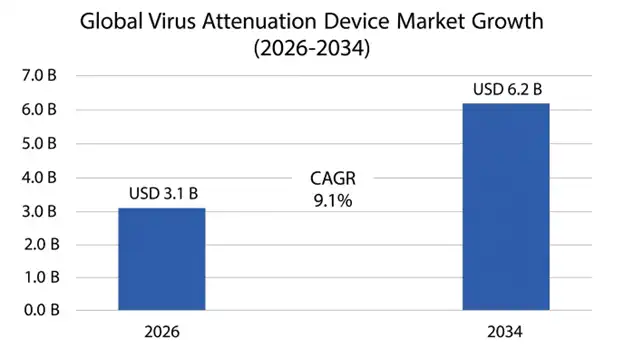

The global virus attenuation device market was valued at USD 2.8 billion in 2025 and is projected to reach USD 3.1 billion in 2026, expanding to USD 6.2 billion by 2034, growing at a CAGR of 9.1% during the forecast period (2026–2034).

Virus attenuation devices consist of an array of technologically advanced systems that attenuate or kill viruses for use in different applications such as pharmaceutical production, blood safety, environmental decontamination, and research purposes. The advanced systems utilize validated physical, chemical, and photochemical processes that inhibit the viruses’ ability to infect other cells without affecting the structural integrity required for applications such as antigen or vector production.

The market serves two main but interrelated categories: the pharmaceutical and biological virus attenuation devices which are used in controlled manufacturing facilities for the production of vaccines, ensuring the safety of blood components, viral vectors, and biopharmaceuticals; and environmental virus attenuation devices that can be installed in hospitals, office buildings, transport stations, and other public places for reducing the presence of airborne and surface viruses. Although both categories employ similar technologies based on ultraviolet irradiation, photolysis, and advanced filtration, they have distinct regulatory requirements, performance characteristics, and business models.

Pharmaceutical virus attenuation is the most technologically advanced and strictly regulated category, where the devices must produce specific viral log reduction levels, while preserving the product quality according to the strict standards of Good Manufacturing Practice. Such systems use sophisticated process analytical technologies, automated dose control, and extensive validation procedures to facilitate regulatory submissions for therapeutic products such as inactivated vaccines, pathogen-reduced blood products, and viral vector gene therapies. These technologies support the safe production of healthcare products through validated viral clearance processes.

Environmental virus attenuation systems address the growing public health challenge of airborne viral transmission, which cannot be managed solely through cleaning techniques and personal protective equipment. Such systems are integrated into building HVAC systems or operate as standalone air-cleaning or point-of-use devices that continuously reduce viral loads in occupied environments, helping with implementing infection prevention strategies in healthcare settings, education establishments, office buildings, and other places where there is a presence of people.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 2.8 Billion |

| Forecast Value | USD 6.2 Billion |

| CAGR | 9.1% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Technology, Application, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Switzerland, China, Japan, India, South Korea, Australia, Brazil, UAE, Saudi Arabia |

| Key Market Playes | Cerus Corporation, Sartorius AG, Terumo BCT, Philips (Signify), Steris Corporation, Honeywell International, Daikin Industries, UV Angel |

Get more details on this report - Request Free Sample

The major structural factor behind the development of the virus attenuation device market is the fast-growing global biopharmaceutical manufacturing capabilities, especially cell and gene therapy manufacturing, vaccines, and plasma-derived therapeutic drugs, which need to incorporate validated virus clearance and attenuation technology as an integral part of the manufacturing process under the strict regulations of FDA, European Medicines Agency, and International Council for Harmonization. Global biopharmaceutical market reached above USD 420 billion in 2025, wherein biologics constitutes 38% of total pharmaceutical revenue and has an annual growth rate of 12.4%.

Regulatory guidelines such as ICH Q5A mandate the implementation of viral clearance strategies using multiple orthogonal attenuation and removal steps to achieve log reductions greater than 4-6 logs for relevant viral species, thereby ensuring the safety of the process irrespective of any adventitious viral contamination. With the advancement of gene therapies utilizing viral vectors, there is a growing need to attenuate contaminating viruses without affecting the potency of therapeutic vectors. This necessitates advanced attenuation systems capable of distinguishing between contaminating and target viruses based on their physical and chemical attributes.

Cell and gene therapy constitutes the largest demand generation segment with more than 1,200 active clinical trials and 47 approved products demanding specialized viral safety solutions in hundreds of production facilities globally. The development of each new biopharmaceutical product demands viral clearance validation studies costing USD 300,000-900,000 per product. This generates repeatable revenues for device suppliers providing validated platforms with proven regulatory acceptability and technical expertise.

COVID-19 caused a major shift in institutional understanding of airborne viral transmission risks, thus leading to unprecedented investments in the infrastructure of environmental viral controls within healthcare centers, office buildings, education institutions, and even transport infrastructure, thereby creating an ongoing demand for air and surface disinfection technology that will ensure viral load reduction. The total spending on global pandemic preparedness stood at USD 24.8 billion from 2021-2025, with many investments going into improving building infrastructure and healthcare centers.

Medical facilities have increased efforts in procuring environmental viral attenuation technologies such as far-UVC, upper room UV, and enhanced air filtration systems to minimize the risks of nosocomial infections and enhance infection prevention strategies in patient treatment zones, surgical suites, and isolation rooms where traditional ventilation is inadequate in achieving desirable viral load levels. These technologies address limitations associated with episodic cleaning and disinfection by providing continuous automated viral reduction independent of human behavior.

Operators of commercial buildings and educational facilities are increasingly adopting environmental viral attenuation technologies as long-term infrastructure investments rather than temporary pandemic mitigation solutions, because of the demand for health and safety, reduced liability, and understanding that respiratory viral transmission is an operational risk that requires engineered control. Incorporating viral attenuation technology into building management systems will allow automatic functioning, energy efficiency, and performance measurement, ensuring sustainable operations.

The primary factor restricting broader adoption of virus attenuation devices is the high initial capital investment required for the equipment., between USD 125,000-350,000 for photochemical systems of pharmaceutical quality and USD 1.8-4.2 million for gamma or electron beam equipment, along with the need for validation, recurring costs of supplies, and special staff, which makes the cost of ownership prohibitively high for small-scale operations and emerging markets. The validation itself incurs costs of USD 180,000-500,000 based on tests for consistent performance under operational conditions.

The complexity of viral attenuation system design requires significant technical support, operator training, and maintenance capacity that might not be available in small setups and developing countries, restricting use to those organizations that are well-endowed with technical know-how in bioprocessing. The integration of the system with existing manufacturing or facility systems may necessitate major changes to the utility and process control systems.

Several technical limitations significantly hinder the universal application of currently available virus attenuation methods, especially when it comes to the attenuation of non-enveloped viruses such as parvovirus B19 and norovirus which exhibit greater resistance to photodynamic and UV treatments than enveloped viruses, thereby leaving certain safety concerns open for applications in which such resistant viruses pose health threats. Biological matrices such as whole blood, protein concentrates, and cell culture media that contain significant amounts of UV-absorbing substances can reduce treatment effectiveness through competitive absorption.

An opportunity exists to transform the market through the development of virus attenuation systems specifically designed to integrate into continuous manufacturing processes as opposed to conventional batch manufacturing processes, making it possible to monitor, treat and control the process in real-time thus reducing processing time, reducing product contact times and documenting the effectiveness of treatment. Biopharmaceutical industry move towards continuous manufacturing processes creates the need for virus attenuation systems that can be used with continuous processes.

Inline UV-C and photochemical inactivation systems engineered for continuous operation provide consistent viral log reductions under variable flow conditions using validated residence time distribution in precisely engineered flow cells, which makes it possible to install such technologies into perfusion bioreactors as well as continuous purification processes. Advanced integration of process analytical technology offers real-time monitoring of viral load, inactivation dose, and system performance with automated process control at validated process parameters.

The commercialization of far-UVC technology operating at a wavelength of 222 nanometers presents a substantial business opportunity for the application of this technology in the environmental attenuation of viruses since it is highly efficacious at killing airborne and surface viruses while being unable to penetrate deep into human skin and cornea, thereby allowing continuous safe operation in human-occupied environments without exposure constraints that confine the use of traditional UV-C with a wavelength of 254 nanometers to empty environments.

Clinical validation trials show that far-UVC provides over a 99.9% reduction in airborne viral concentrations within 10–15 minutes of continuous use at prescribed dose rates, whereas the human safety tests show that it is safe enough for exposure thresholds that can facilitate its approval for usage in occupied spaces. Technology resolves the basic shortcomings of the existing HVAC system-based approach.

Machine learning techniques have significantly improved the operation of virus attenuation devices by providing predictive models for the effectiveness of treatments under different operating conditions, automatic adjustments to process parameters to ensure uniform log reduction rates regardless of changes in feed stream composition, and prediction of system deterioration ahead of time to avoid any negative impact on the treatment efficiency. The AI-based PAT systems use spectroscopic analysis along with other process data for prediction and optimization.

Validation studies utilizing predictive models developed from large viral clearance databases are reducing the number of required validation experiments by determining the optimal process parameters via computer simulation before validation in the lab, which may save up to 25-40% of the work involved in such validations, without compromising on regulatory acceptance.

The attenuation technology for viruses is moving towards multi-mode systems using various forms of attenuation techniques like UV-C light, photo-chemical processing, and filtration in one single device. This results in better performance of such devices in terms of viral elimination than single mode devices. In addition, multi-mode systems have the advantage of redundancy in case of equipment failure and thus offer better operational performance and regulatory compliance. They give cumulative log reductions higher than any single method used individually.

North America accounted for the highest market share of USD 1.15 billion in 2025 and is expected to have a CAGR of 8.7% during the forecast period from 2024 to 2034, owing to the presence of global biopharmaceutical manufacturing facilities where more than 42% of the global capacity of biologicals manufacturing lies in the United States along with stringent regulatory frameworks that mandate validated viral clearance methods for blood products and biologics. The stringent approach adopted by FDA in enforcing viral safety guidelines results in continuous demand for validated attenuation technologies.

The region houses the largest number of cell and gene therapy manufacturing facilities globally, where there are more than 320 such facilities producing advanced therapies for clinical as well as commercial purposes. Investments made by governments in pandemic preparedness activities via BARDA and CDC ensure continued demand for environmental viral control technologies.

The Asia Pacific region is the fastest-growing segment with a CAGR of 10.8% till 2034 and revenues of USD 580 million in 2025 owing to the fast growth in biopharmaceutical production capacities in China, South Korea, and India, increasing regulations aligned with global viral safety norms, and significant government investments in pandemic preparedness facilities. The Chinese biopharmaceutical manufacturing industry registered a 32% annual growth from 2020-2025 with regulatory authorities enforcing viral safety norms aligned with ICH regulations.

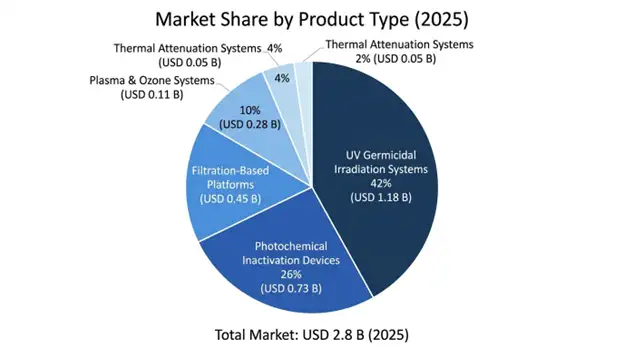

The Ultraviolet Germicidal Irradiation Systems hold the largest market share of 42%, accounting for USD 1.18 billion in 2025, and is expected to witness a CAGR of 9.3% during 2025-2034. The category includes flow through UV-C systems used for treating liquids, chamber systems for surface disinfection, and far-UVC technology systems used in occupied spaces. The segment gains an edge over its peers owing to its wide acceptance and well-defined validation protocols.

The Photochemical Inactivation Devices segment has a 26% market share with a value of USD 728 million in 2025 and includes psoralen-UVA and riboflavin-UV technologies used for pathogen reduction of blood components as well as in pharmaceutical applications. The segment enjoys high pricing due to its exclusive reagents and validation datasets.

Pharmaceutical & Biopharmaceutical Manufacturing is the leading end-user segment accounting for 38% market share with USD 1.06 billion valuation in 2025, covering areas such as virus removal in biologics production, vaccine manufacture, and cell therapy processing. The segment gains from regulations, need for validation, and high prices of advanced pharmaceutical equipment.

Environmental Air & Surface Disinfection stands at 31% with revenue at USD 868 million in 2025 with 10.2% CAGR to 2034, being the fastest-growing segment due to spending on pandemic preparedness, health care infection prevention measures, and commercial building safety.

Pharmaceuticals form the biggest end user segment accounting for 35% market share worth USD 980 million by 2025, including biological drugs, plasma fractionation, and advanced therapies producers that need a validated system for viral clearance as a critical part of the manufacturing process. This segment displays steady buying behavior driven by regulation and supply chain considerations.

Healthcare & Hospitals contribute to 28% market share valued at USD 784 million in 2025 with a CAGR of 9.8% during 2034, fueled by environmental infection control needs, blood bank pathogen reduction technologies, and pandemic preparation facilities.

The global market for virus attenuation devices has a moderate level of concentration in that the major firms control roughly 58 to 65 percent of market value by having a full range of technologies across both pharmaceutical and environmental markets, regulatory expertise, validated platforms, and worldwide distribution channels. The key competitive factors include proven log reductions, wide acceptance among regulators, cost optimization, and implementation capabilities.

Technology leadership demands consistent innovation in the efficacy of treatments, the integration capacity of processes, and the sophistication of control systems that distinguish high-end products from commoditized UV lamp systems, while total service offerings, such as validation and regulatory guidance, generate switching costs for customers.

March 2026: The Cerus Corporation reported the FDA approval of INTERCEPT Blood System for red blood cells pathogen reduction after completing Phase III clinical trials, increasing the addressable market by USD 1.4 billion due to the inclusion of the most used blood component in pathogen reduction systems.

February 2026: The Sartorius AG introduced its next generation of the continuous flow UV-C attenuation system, capable of reducing the level of parvovirus by 6.5 long per hour at a throughput of 150 L/hr. It is designed specifically for continuous biopharmaceutical manufacturing with process analytical technology and automated dose control.

January 2026: Philips (Signify) was granted the FDA 510(k) clearance for its far-UVC disinfection system for use in occupied healthcare settings.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.